What you’ll learn in this article…

- Scholarships, employer sponsorship, and military benefits should be exhausted before borrowing any MBA loans.

- IRS Section 127 lets employers provide up to $5,250 in tax-free tuition assistance per year for MBA courses.

- Roughly 61% of MBA students receive scholarship or grant funding, according to GMAC's 2026 survey.

- Modeling your debt to income ratio and monthly repayment before enrolling prevents overborrowing and protects long-term ROI.

MBA tuition ranges from under $20,000 for some online and in-state public programs to more than $200,000 in total cost of attendance at elite full-time programs. That spread makes program selection and financing strategy inseparable decisions. For a detailed breakdown of costs by format and school type, see our best MBA programs cost guide.

Paying for an MBA efficiently follows a logical sequence: reduce the sticker price first, compare every funding source before borrowing, understand federal and private loan structures, evaluate the return on investment for your specific career target, match your financing approach to the format you choose, then build a concrete payment plan with real numbers.

This guide is educational in nature and does not constitute financial, legal, or tax advice. Individual circumstances vary, and you should consult qualified professionals before making enrollment or borrowing decisions. What the data consistently shows is that candidates who model their full repayment cost before enrolling make materially better financing choices than those who focus only on tuition.

Step 1: Reduce the Price Before Borrowing

Under IRS Section 127, employers can provide up to $5,250 in tax-free education assistance annually for graduate courses, including MBA tuition.1 This exclusion is a powerful starting point, but free money in any form should be your first priority before considering loans. Every dollar you receive without repayment eliminates future interest and shortens your payback period. The most accessible sources are scholarships, fellowships, and graduate assistantships, which require no repayment and are awarded based on merit, background, or need.

Maximize Free Money First: Scholarships, Fellowships, and Assistantships

Scholarships are the gold standard of MBA funding because they directly reduce what you owe. Private and school-based awards can range from partial tuition to full rides, often targeting diversity, industry experience, or leadership potential. Visit our MBA scholarships guide for a detailed breakdown of top programs and application strategies. Fellowships typically include a stipend and tuition waiver in exchange for research or teaching assistance, providing both funding and resume-building experience. Graduate assistantships operate similarly, covering a portion of tuition in return for part-time work. Unlike loans, these awards never accrue interest, making them your highest-leverage option.

Employer Sponsorship: Tax Benefits and Clawback Risks

Many companies that pay for MBA degrees offer tuition reimbursement as a standard benefit, and the IRS makes up to $5,250 per year tax-free for the employee under Section 127.1 Eligible expenses include tuition, fees, books, supplies, and equipment, as well as some loan repayments, while meals, transportation, and lodging do not qualify.2 Any amount above the cap is treated as taxable compensation, but the tax-free portion alone can significantly offset MBA costs. Be aware, however, that most employer plans come with strings attached. It is common for employers to require a post-completion service commitment of one to three years. If you leave voluntarily or are terminated before that period ends, you may trigger a clawback clause and owe some or all of the reimbursed amount. Always request the written policy and model worst-case scenarios before accepting.

Military Benefits: GI Bill and Yellow Ribbon

Veterans and eligible dependents can tap substantial education benefits. The Post-9/11 GI Bill pays up to an annual national maximum for private school tuition, and the Yellow Ribbon Program can cover remaining out-of-pocket charges when the school participates. Yellow Ribbon splits the excess cost between the VA and the institution, but availability and the amount of the institution's contribution vary by school. Graduate programs are eligible, but you must be at the 100% benefit level to qualify for Yellow Ribbon. For a deeper look at veteran-specific funding options, see our guide to military MBA financial aid. In the meantime, verify your benefit eligibility and the school's participation status through the VA website or the admissions office.

Structural Savings: Lower-Cost Formats and In-State Options

Before applying for any aid, you can cut the base price by choosing a lower-cost degree pathway. In-state public university MBA programs charge substantially less than private or out-of-state alternatives, sometimes half the tuition or less. Part-time and online formats allow you to continue earning an income while studying, reducing the need to borrow for living expenses and leveraging cash flow to pay as you go. Online MBAs offered by public universities often match in-state rates for all students regardless of residency and eliminate relocation and commuting costs. For a full breakdown of tuition benchmarks across delivery formats, see our online MBA cost analysis. While these formats may extend your timeline, the total cost of attendance can drop by tens of thousands of dollars, shifting the ROI equation in your favor before you ever submit a loan application.

Negotiating and Appealing Scholarship Offers

Few applicants realize that MBA scholarship awards are often negotiable. Many programs have a formal reconsideration process, especially if you hold a competing offer from a similarly ranked school. After receiving your initial aid package, politely contact the admissions office to share relevant competing offers and ask whether additional funding is available. Frame the discussion around your enthusiasm for the program and your need to make the financial decision work. Even a modest increase of a few thousand dollars per year can compound into significant savings over the life of your MBA and reduce your total debt load at graduation.

Step 2: Compare Funding Sources

Not all MBA funding carries the same cost, conditions, or risk. Before committing to any single source, compare the options side by side. The strongest payment plans typically combine two or more of the sources below, starting with those that do not require repayment and filling any remaining gap with the most borrower-friendly loans available.

| Funding Source | Best For | Repayment Required? | Key Risk |

|---|---|---|---|

| Scholarships | High-achieving or targeted applicants (merit, diversity, need-based) | No | Highly competitive; may require maintaining a minimum GPA |

| Employer sponsorship | Working professionals whose companies offer tuition reimbursement | Usually no, but may require a service commitment | Clawback provisions if you leave the employer before the agreed period |

| Federal loans | U.S. citizens and eligible noncitizens who need to borrow | Yes | Borrowing limits and accruing interest; repayment begins after graduation or grace period |

| Private loans | Borrowers with strong credit or those who need to cover funding gaps beyond federal limits | Yes | Fewer borrower protections, variable interest rates, and limited deferment options |

| GI Bill and Yellow Ribbon | Eligible veterans and qualifying dependents | No or significantly reduced | Not all schools participate in Yellow Ribbon; benefit amounts vary by service history |

| Personal savings | Students focused on minimizing or eliminating debt | No | Liquidity risk; depleting savings may leave little financial cushion during the program |

Step 3: Understand MBA Loans

What are the differences between federal and private MBA loans, and which should you borrow first?

Once you have exhausted scholarships, employer contributions, and personal savings, student loans become the next layer of MBA financing. Understanding the structure, protections, and trade-offs between federal and private loans is critical to managing your debt responsibly and preserving financial flexibility after graduation.

Federal Direct Unsubsidized Loans

Graduate and professional students are eligible to borrow through the federal Direct Unsubsidized Loan program. For the 2025, 2026 academic year, these loans carry a fixed interest rate of 7.94 percent.1 You may borrow up to $20,500 per year, with an aggregate lifetime limit of $138,500 (including any undergraduate federal loans).1 Interest accrues while you are enrolled, but you are not required to make payments until after graduation or dropping below half-time enrollment.

These loans require no credit check and no cosigner. MBA students qualify as independent graduate students and must file the Free Application for Federal Student Aid (FAFSA) each year to access federal loan eligibility. Our FAFSA for MBA guide walks through the application process, deadlines, and maximum loan amounts. The FAFSA opens every October for the following academic year.

Grad PLUS Loans

If your cost of attendance exceeds the Direct Unsubsidized Loan limit, you may apply for a Grad PLUS Loan. For 2025, 2026, the interest rate is 8.94 percent, and an origination fee of 4.228 percent is deducted from each disbursement.2 Grad PLUS allows you to borrow up to the full cost of attendance minus any other aid received.

Unlike Direct Unsubsidized Loans, Grad PLUS requires a credit check. Borrowers with adverse credit history may be denied or required to obtain an endorser (similar to a cosigner). Borrowers with no credit history or minor issues typically qualify.2

Federal Protections vs. Private Loan Trade-Offs

Federal loans come with borrower protections that private loans rarely match:

- Income-Driven Repayment (IDR) plans that cap monthly payments at a percentage of discretionary income

- Public Service Loan Forgiveness (PSLF) eligibility after 120 qualifying payments while working for a government or nonprofit employer

- Deferment and forbearance options during economic hardship

For borrowers who took out federal loans before July 2026, available IDR plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR).3 Beginning with the 2026, 2027 academic year, new borrowers will enroll in the Tiered Standard or the Repayment Assistance Plan, which offers forgiveness after 30 years and remains PSLF-eligible.3

Private lenders may advertise lower starting rates, especially for borrowers with strong credit scores and stable income. However, many private loans carry variable interest rates that can rise over time, and they typically do not offer IDR, PSLF eligibility, or robust deferment protections. For a deeper look at when borrowing makes sense, see our MBA loan decision guide.

Borrowing Strategy

Exhaust your federal Direct Unsubsidized and Grad PLUS borrowing before considering private loans. Federal loans lock in fixed rates, preserve repayment flexibility, and offer forgiveness pathways unavailable through private lenders. Only after you have maximized federal eligibility should you evaluate private loans to close any remaining funding gap.

Upcoming dedicated pages on federal MBA loans and private MBA loans will explore eligibility, application procedures, repayment simulations, and lender comparisons in depth.

*This guide is for educational purposes only and does not constitute financial, legal, or tax advice. Consult a qualified professional before making borrowing decisions.*

Questions to Ask Yourself

Step 4: Evaluate the ROI of an MBA Before Enrolling

Return on investment is the ratio of financial gain to cost, and for an MBA, that means comparing your total program expense against the salary increase and career opportunities you unlock. Before you borrow a dollar, you need to model whether the economics work in your favor.

Average Post-MBA Salary by Function

According to recent survey data, the median starting salary for MBA graduates in the United States stands at approximately $125,000, with an average salary uplift of $41,000 (roughly 46 percent) over pre-MBA earnings.1 However, outcomes vary significantly by career function. Graduates entering management consulting earn a mean annual wage near $147,000, while those in finance roles average around $139,000.1 Technology product management positions typically start near $165,000 at the median, and marketing and general management roles often fall closer to $120,000.2 At top-tier programs, median total compensation can reach $190,000 or more when bonuses and equity are included.2 Investment banking offers the highest total compensation, often between $275,000 and $350,000 when performance bonuses are factored in. For a deeper breakdown by job title and industry, see our guide to MBA career paths and salaries.

These figures represent starting points. The value of an MBA extends across decades, but your first-year salary determines how quickly you can repay debt and how much financial flexibility you retain.

Debt-to-Income Guideline and Payback Period

A widely cited rule of thumb is to keep your total MBA debt below your expected first-year post-MBA salary. If you anticipate earning $130,000 after graduation, aim to borrow no more than $130,000 in total. This ratio helps ensure that monthly loan payments remain manageable relative to your take-home pay.

To estimate your payback period, divide your total debt by your annual salary increase. For example, if you borrow $100,000 and expect your salary to rise by $50,000, your simple payback period is two years. This calculation ignores interest and taxes, so real payback will take longer, but it provides a quick litmus test. If your payback period exceeds three or four years, scrutinize whether the program's outcomes justify the cost.

Career-Switch Probability and Placement Infrastructure

Recent data shows that approximately 24 percent of MBA graduates change careers, a figure lower than the 70 to 80 percent switching rates often cited by full-time programs in their employment reports.1 The difference may reflect methodology, with some schools counting any function or industry change as a switch, while others count only major pivots. Regardless, the MBA remains one of the few credentials that actively facilitates career transitions.

What drives successful switches is not the degree alone but the infrastructure around it: structured internships, dedicated recruiting relationships, and coaching from career services. Before enrolling, ask programs what percentage of students land internships in your target function, which companies recruit on campus, and how many alumni work in your desired industry. Generic placement rates matter less than targeted outcomes in your specific field. Understanding how to choose the right MBA program for your goals can help you ask the right questions during the evaluation process.

Geographic Salary Differences and Real ROI

Salary figures are national averages, but geography matters. A $140,000 salary in San Francisco or New York City buys far less than the same figure in Austin, Charlotte, or Chicago. When evaluating ROI, adjust for cost of living in your likely post-MBA market. A program with strong regional employer ties and lower tuition may deliver better real purchasing power than a higher-ranked school with higher debt and a more expensive job market.

Some programs publish median salary by geography in their employment reports. Review these carefully, and model your net income after rent, taxes, and loan payments in your target city.

Alumni Network and Long-Term Optionality

The hardest ROI components to quantify are alumni network strength and long-term career optionality. A strong network can accelerate promotions, open doors to venture funding, or provide board seats decades after graduation. These benefits do not appear in first-year salary data, but they compound over time.

Before committing, speak with alumni who graduated five or ten years ago. Ask whether the network remains active, whether the school's brand opens doors in your industry, and whether they would make the same investment again. Research on why alumni networks matter can help you evaluate this often-overlooked dimension of program value. Their candor will help you assess whether the intangible returns justify the tangible cost.

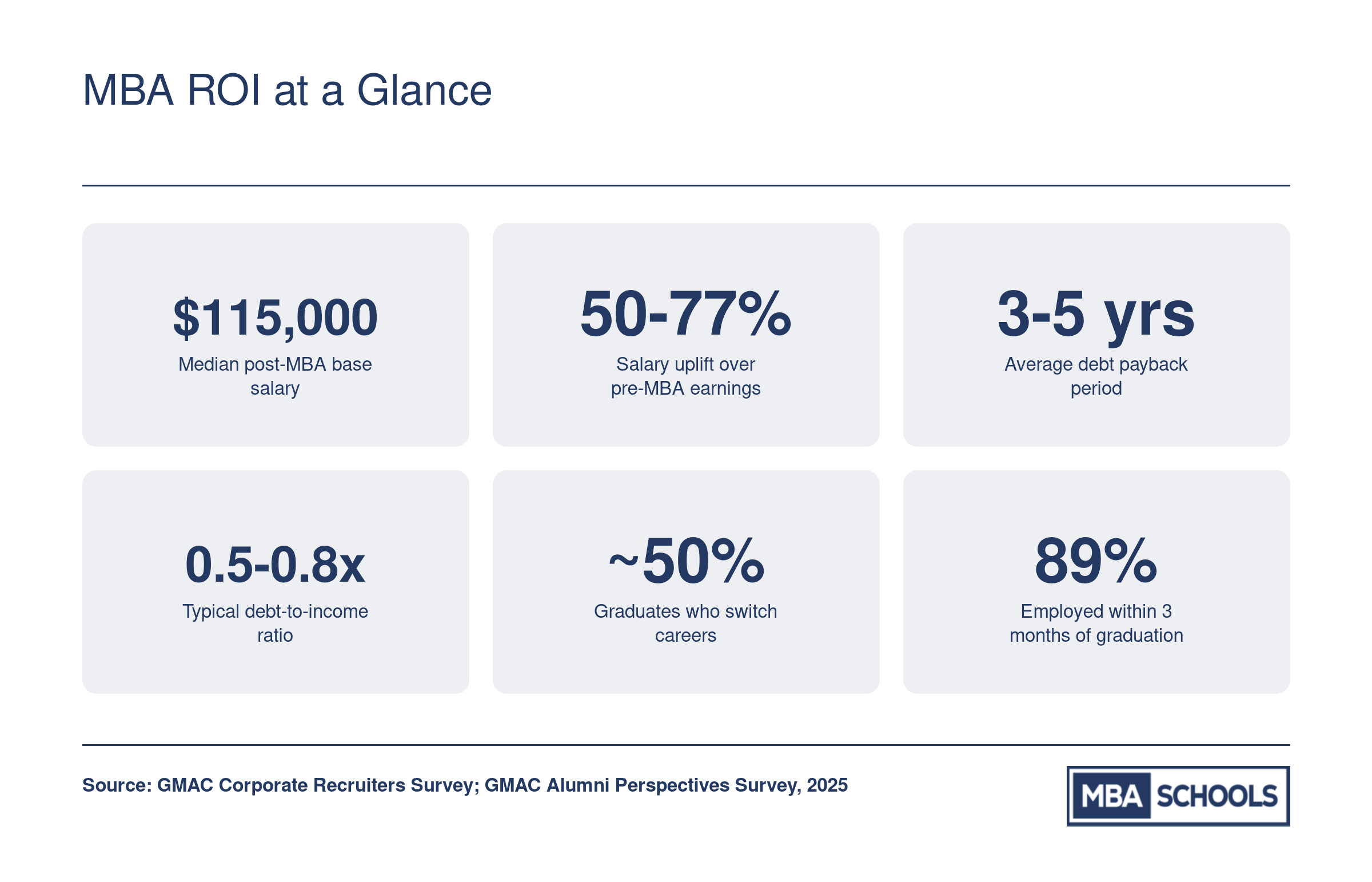

MBA ROI at a Glance

Before committing to a financing strategy, ground your decision in the numbers. These figures reflect broad outcomes reported by recent MBA graduates and illustrate why careful ROI analysis matters before you enroll.

Step 5: Choose a Funding Strategy by MBA Format

The format you choose determines not only how you will study but also how you will pay. A full-time program that removes you from the workforce for two years creates a fundamentally different financial equation than an executive MBA where your employer picks up the tab. Matching your funding strategy to your program format is one of the most consequential decisions in the entire MBA financing process.

Full-Time Two-Year MBA

Total tuition for a full-time two-year MBA typically ranges from $60,000 to $200,000, with elite programs clustering at the higher end.1 Because you are leaving employment, employer tuition reimbursement is uncommon. The primary funding sources are merit scholarships, federal and private loans, and personal savings. Full-time programs tend to offer the most generous scholarship pools, so aggressive mba scholarship applications are essential. Expect to rely heavily on borrowing unless you secure substantial grant aid.

Part-Time MBA

Part-time programs generally cost between $35,000 and $120,000.3 The key advantage here is continued income: you can fund tuition through salary cash flow and employer tuition assistance programs. Employer support is far more common in part-time formats than in full-time programs because companies retain you as an employee throughout your studies. Loans remain an option, but many part-time students minimize borrowing by paying as they go.

Online MBA

Online MBA tuition spans roughly $20,000 to $90,000, making it one of the more affordable formats.3 Employer tuition assistance and salary-based payments are the dominant funding sources. However, scholarships tend to be less generous for online programs compared to their residential counterparts. If cost minimization is a priority and you have employer support, an online format can significantly reduce your debt load.

Executive MBA

Executive MBA programs carry tuition ranging from $80,000 to $200,000, yet they also have the highest rate of employer sponsorship among all formats.4 Many organizations cover full or partial EMBA costs for senior employees they want to retain and develop. Personal savings and loans fill any gaps. If your company offers sponsorship, an EMBA can be one of the most accessible high-end programs financially, despite its sticker price.

One-Year MBA

Accelerated one-year programs cost between $50,000 and $130,000.5 Scholarships and loans are the most common funding sources, supplemented by personal savings. While the compressed timeline reduces opportunity cost, employer reimbursement is less common than in executive programs. Merit scholarships can make a significant difference, so apply broadly.

Dual-Degree MBA

Dual-degree programs combining an MBA with a law, medical, or public policy degree represent the highest total investment, typically $150,000 to $250,000.5 Funding often comes from loans and scholarships awarded by both schools involved. Employer reimbursement is rare outside of sponsored corporate tracks. Plan for substantial borrowing, and investigate whether each school offers dedicated dual-degree financial aid packages.

Step 6: Build Your MBA Payment Plan

As MBA sticker prices continue to outpace inflation, building a deliberate funding plan before you enroll has shifted from a good idea to a financial necessity. A transparent formula lets you isolate exactly how much you need to borrow and whether that debt load aligns with your career goals.

The Funding Formula

A straightforward equation anchors every sound MBA payment plan:

- Total Cost of Attendance (COA): includes tuition, mandatory fees, books, supplies, living expenses, and health insurance

- Minus Scholarships and Grants: merit- or need-based awards that do not require repayment

- Minus Employer or Military Benefits: tuition reimbursement, GI Bill, Yellow Ribbon, or similar

- Minus Savings and Cash Flow: personal assets you can deploy without taking on debt

- Equals Amount to Finance: the gap you must cover through loans or other debt

This exercise forces you to confront the true borrowing need. Many students overlook employer contributions or underestimate living costs, leading to unnecessary borrowing. Run the formula three times: once with conservative assumptions, once with optimistic ones, and once with the most realistic set.

Case Study: Part-Time Public MBA

Consider a working professional pursuing a part-time MBA at a public university while keeping their day job.

- Total COA over three years: $60,000 (tuition $36,000; living expenses not included because salary covers them)

- Merit scholarship: $15,000 total

- Employer reimbursement: $5,250 per calendar year, totaling $15,750 over three years

- Personal savings: $10,000

Amount to finance: $60,000 , $15,000 , $15,750 , $10,000 = $19,250.

On a 10-year federal Direct Unsubsidized Loan at 6.5% interest, the monthly payment would be roughly $218. That is less than six dollars a day. Because the student is still earning a full-time salary throughout, this debt is easily serviceable and leaves plenty of room for other financial goals.

Case Study: Top-20 Full-Time Private MBA

Now imagine a candidate leaving a $95,000 job to enroll full-time in a highly selective two-year program.

- Total COA over two years: $155,000 (tuition $110,000; room and board, books, and insurance add $45,000)

- Scholarships and fellowships: $30,000

- Employer sponsorship: $0

- Personal savings: $20,000

Amount to finance: $155,000 , $30,000 , $20,000 = $105,000.

Financing an MBA with a combination of federal and private loans at a blended interest rate of 7.0% over 10 years produces a monthly payment around $1,219. If the expected post-MBA base salary is $140,000, monthly take-home pay after taxes and deductions might be roughly $7,800. The student-loan payment would consume 15.6% of that income. Crossing the 10 to 15% threshold means the borrower must scrutinize job-offer certainty and lifestyle trade-offs before signing a promissory note.

Model Monthly Payments Before You Commit

The U.S. Department of Education's Loan Simulator and many private calculators let you test different repayment scenarios using your expected income and debt level. A healthy guideline: keep total student-loan payments below 10 to 15% of your projected after-tax monthly income. If your expected payment exceeds that band, you have three levers: reduce the amount borrowed (more scholarships, a lower-cost program, or a longer timeline), increase income (negotiate a higher salary or pursue a field with stronger compensation), or extend the repayment term with the understanding that interest costs will grow.

Know Your Numbers: Tuition vs. Total Cost vs. Repayment Cost

Misunderstanding these terms is the most common budgeting mistake. If you are still weighing program options, our guide on factors to consider when choosing an MBA program can help you compare costs side by side.

- Tuition: the base price of instruction only.

- Total Cost of Attendance: the full sticker price your school reports, including living expenses, books, supplies, and fees.

- Total Repayment Cost: the principal you borrow plus all interest that accrues over the life of the loan. Borrowing $105,000 at 7.0% for 10 years means you will pay back approximately $146,000. At 8.5% on a 15-year term, the same principal balloons to over $186,000.

Always plan from total repayment cost, not the amount you receive. A manageable monthly payment today can mask a doubling of true expense across decades. Regularly revisit your plan as your career progresses; refinancing opportunities, bonus windfalls, or accelerated repayment can meaningfully shrink total cost.

*This guide is for educational purposes only and does not constitute financial, legal, or tax advice. Consult a qualified professional before making borrowing decisions.*

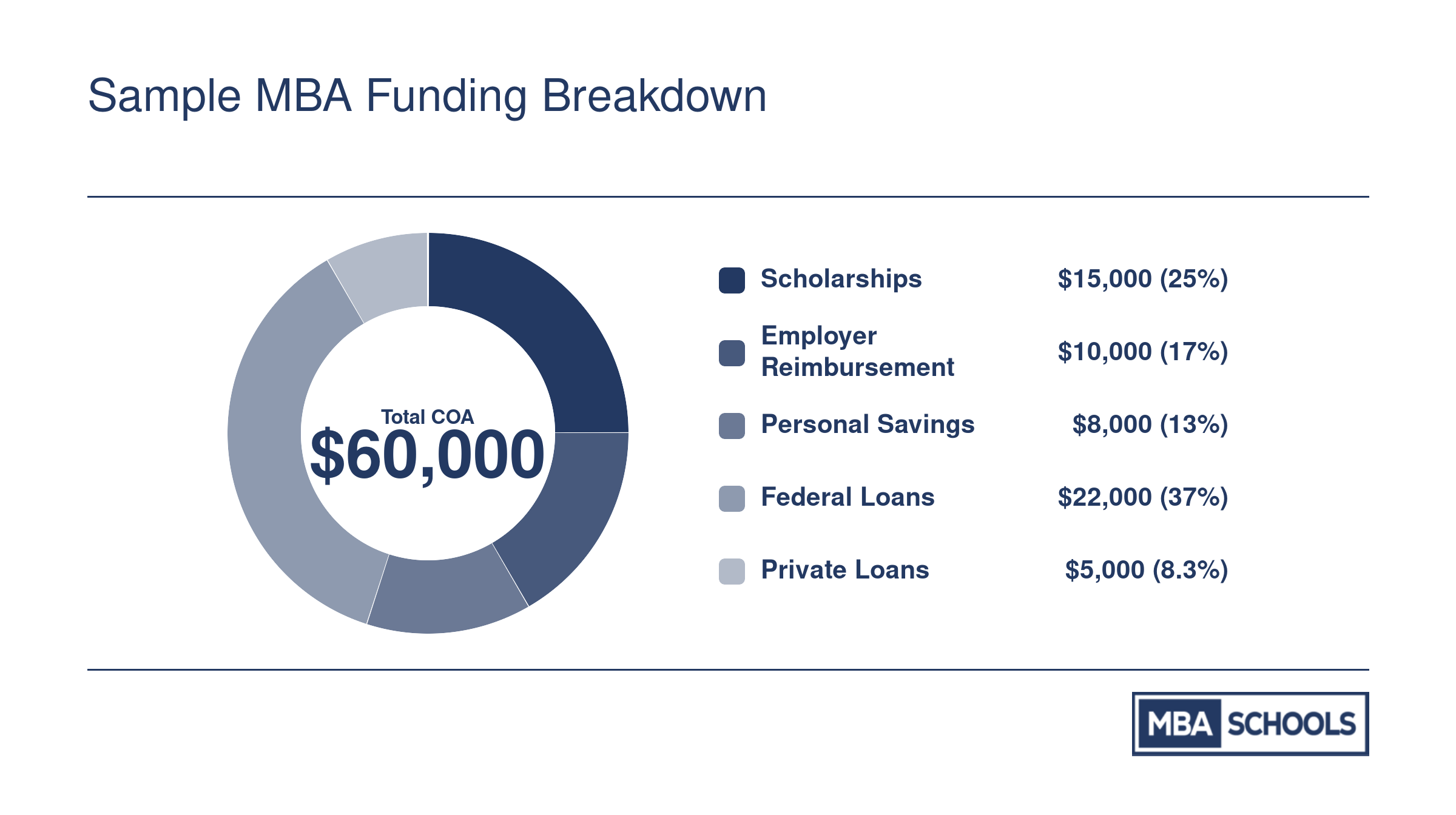

Sample MBA Funding Breakdown

Here is how a hypothetical $60,000 total cost of attendance might break down across multiple funding sources. Before committing to any program, model your own version of this breakdown and calculate the monthly repayment on the financed portion to confirm it fits your post-MBA budget.

According to the GMAC Prospective Students Survey 2026, roughly 61% of MBA students receive some form of scholarship or grant funding. That means the majority of candidates pay less than the published sticker price, making it well worth applying broadly before assuming you will need to borrow the full cost.

Frequently Asked Questions

Financing an MBA involves many moving parts, from federal aid eligibility to scholarship negotiation. Below are answers to the questions prospective MBA students ask most often. For deeper coverage of any topic, follow the links to our dedicated guides.

Related Articles

Explore Resources How to Pay for An MBA

Explore More

- AACSB-Accredited MBA

- Best GRE Prep Courses for MBA Applicants

- Best Military-Friendly MBA

- DISC Assessment for MBA Students & Graduates

- Executive MBA Courses

- Executive MBA vs. MBA

- FAFSA for MBA Students

- Financial Aid for Minority MBA Students

- Financing Your MBA

- GMAT Study Guide

- GRE Guide for MBA Applicants

- How Much Does an Online MBA Cost? Full Breakdown

- How to Choose the Right MBA

- LGBTQ+ MBA

- MBA Accreditation Types

- MBA Admissions Consulting Guide

- MBA Admissions Rounds vs. Rolling Admissions

- MBA Capstone Projects

- MBA Careers Guide

- MBA Entrance Exams

- MBA FAQ

- MBA Glossary

- MBA Preparation Courses

- MBA Requirements

- MBA Resume Guide

- MBA Salary

- MBA Scholarships

- MBA Scholarships for AAPI Students

- MBA Scholarships for Black Students

- MBA Scholarships for Hispanic & Latino Students

- MBA Scholarships for International Students

- MBA Scholarships for Women

- MBA vs. Master's Degree

- Military MBA Financial Aid

- Mini-MBA

- Native American MBA Scholarships

- Undergraduate Prerequisites for MBA

- What Is a STEM MBA Program? Benefits, Schools & OPT Guide

- What Is an MBA? Your Complete Guide to MBA Degrees