What you’ll learn in this article…

- Keep total MBA debt below your realistic first-year post-MBA salary to maintain manageable repayment timelines.

- Opportunity cost often exceeds tuition: a professional earning $90,000 forfeits over $180,000 by attending a two-year full-time program.

- Target industry matters most because consulting and finance starting salaries can be double what nonprofit or government roles offer.

- Part-time and online formats cut total costs dramatically by letting you keep your income while earning the degree.

Most prospective MBA students wrestle with the same uncomfortable question: is borrowing six figures for a business degree reckless or rational? A recent Reddit post on r/MBA, titled "Is it worth taking a hefty loan for an MBA?", captures the anxiety underlying this calculus. The original poster is hardly alone. Coffee chats with current students and online forums overflow with similar hand-wringing, yet most of the advice boils down to useless absolutes: "always worth it if you go to a top program" or "never borrow for grad school."

The truth is messier. Whether MBA debt makes sense depends on your salary trajectory, target industry, opportunity cost, program tier, existing savings, and risk tolerance. A $120,000 loan for a consulting track at a top-15 program can pay itself back in under five years. The same debt load for a nonprofit career at a regional program can compound into a decade-long drag on discretionary income. The difference is not motivation or work ethic. It is arithmetic.

This analysis provides the benchmarks, industry-specific salary models, and decision framework to help you quantify when MBA debt is a calculated investment and when it crosses into financial overextension. Whether you are weighing financing your MBA through federal loans, scholarships, or employer sponsorship, the goal is the same: replace gut feelings with numbers you can defend.

The Real Cost of an MBA: Beyond Tuition

Most prospective MBA students underestimate what the degree will actually cost them, sometimes by a factor of two or more.

The Four Cost Buckets

Think of MBA expenses in four distinct categories:

- Tuition and program fees: The sticker price schools advertise, which ranges from roughly $27,000 for affordable online programs to well over $200,000 for two years at a top-tier full-time program.

- Books, materials, and technology: A secondary but real expense, typically running $3,000 to $8,000 over the course of a full-time program.

- Living expenses: Rent, food, transportation, and health insurance during enrollment. In high-cost cities where many elite programs are located, this can add $30,000 to $60,000 per year.

- Opportunity cost: The salary you stop earning when you leave the workforce. For full-time students, this is almost always the largest single number in the calculation, and the one most borrowers ignore.

What Borrowers Actually Owe by Tier

Debt levels vary sharply depending on where and how you study. According to data from the Education Data Initiative and Edvisors, average MBA loan balances at graduation currently look like this:12

- M7 programs: Graduates typically carry $120,000 to $170,000 in student debt, on top of annual total costs of attendance that run $115,000 to $150,000.

- Top-15 programs (non-M7): Average debt at graduation falls between $90,000 and $150,000.

- Top-25 programs (non-T15): Borrowers typically finish with $70,000 to $120,000 in loans.

- Unranked programs: Debt ranges from roughly $40,000 to $90,000, though program quality and career outcomes vary widely at this tier.

- Part-time programs: Because students keep their jobs and spread costs over three or more years, average debt is considerably lower, generally $20,000 to $80,000.

- Online MBAs: Affordable online options can be completed for $30,000 or less in total cost, while elite online programs from flagship universities often land between $30,000 and $80,000 in debt.

For context, the national average debt for all master's degree holders sits around $81,870, meaning full-time MBA borrowers at selective programs frequently owe double that figure or more.1

The Opportunity Cost Calculation Most Students Skip

Consider a working professional earning $85,000 a year who leaves the workforce to pursue a full-time MBA at a T25 school. Tuition and fees might total $90,000 to $100,000. Add two years of living expenses, books, and miscellaneous costs, and direct out-of-pocket spending reaches roughly $150,000 to $160,000. Now layer in two years of forgone salary: another $170,000 in pre-tax income that never arrives, plus lost retirement contributions and any employer benefits.

The total economic exposure can approach $350,000 or more, even for a mid-tier program. Yet when candidates talk about "MBA debt," they almost exclusively mean the loan balance, which might be $90,000. That fixation on the tuition number causes borrowers to undercount their true financial exposure by 40 to 60 percent. Any honest return-on-investment analysis has to include opportunity cost, and understanding what the average cost of an MBA actually entails is a critical first step.

Opportunity cost is not a debt you owe to a lender, but it is absolutely a cost you owe to your future self. A thorough analysis of whether an MBA is worth it in 2026 must account for every dollar, earned and unearned, not just the loan balance on your statement.

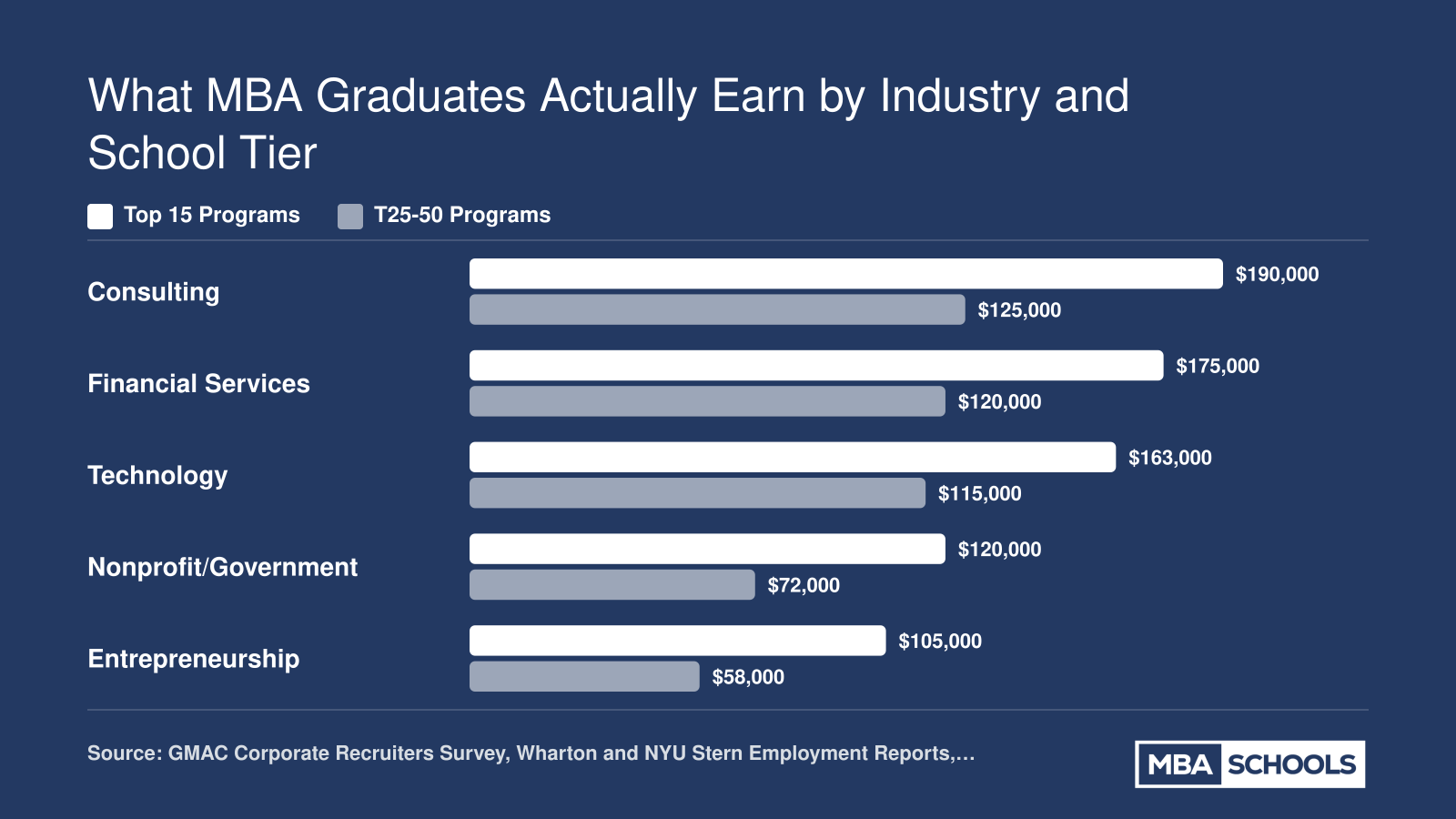

What MBA Graduates Actually Earn by Industry and School Tier

Post-MBA salaries vary dramatically depending on which industry you enter and which program you attend. Before committing to six figures in loans, ground your expectations in real compensation data. The gap between a top-15 program graduate in consulting and a lower-ranked program graduate in the social sector can exceed $130,000 per year, a difference that fundamentally changes the debt calculus.

When MBA Debt Makes Financial Sense

Borrowing six figures to sit in a classroom for two years sounds reckless. Walking away from MBA-level opportunities because you fear debt can be equally costly. The difference lies in knowing which scenarios tip the scale from gamble to calculated investment.

Green-Light Scenarios: When the Math Works in Your Favor

Three archetypes consistently recoup MBA debt ahead of schedule. First, career switchers targeting high-compensation fields. If you are moving from a $70,000 nonprofit role into management consulting, investment banking, or tech product management, the salary compression makes borrowing defensible. Second-year consultants at MBB firms earned base salaries near $175,000 in 2026, with total comp frequently exceeding $225,000 when bonuses land. Exploring MBA career paths and salaries confirms that these trajectories justify substantial borrowing.

Second, professionals with employer sponsorship covering partial tuition. If your firm is funding 40 to 60 percent of the program, your personal loan burden drops by half. The risk profile shifts dramatically when you borrow $60,000 instead of $120,000, even if post-MBA salary gains remain identical.

Third, candidates admitted to programs with verifiable placement rates above 90 percent and median starting salaries at least double their current pay. When a program consistently places graduates into $140,000-plus roles and you are earning $65,000 today, the salary-jump test passes with margin to spare.

The Salary-Jump Test: A Simple Threshold

If the MBA is projected to increase your compensation by at least 50 to 70 percent within three years of graduation, borrowing up to one times your expected post-MBA salary is defensible. A $150,000 loan becomes manageable when you land a $155,000 offer with predictable raises. The ten-year payback horizon remains tolerable, and refinancing options after two years of employment can cut interest costs significantly.

This test fails when salary gains are modest. Moving from $90,000 to $110,000 does not justify $130,000 in debt, no matter how prestigious the program name.

The Elite Program Premium and Its Limits

Data consistently shows M7 and top-15 graduates recoup debt faster. Median time to breakeven at these schools runs 3.5 to 5 years, compared to 7 to 10 years at lower-ranked programs. Recruiting pipelines, alumni networks, and brand recognition compress job search timelines and elevate starting offers.

Yet the gap narrows sharply for part-time students who maintain full-time employment. When you avoid two years of forgone income, even a mid-tier program becomes ROI-positive if tuition remains under $80,000 and you secure a 30 percent raise within 18 months of graduating. For candidates weighing format trade-offs, understanding online MBA vs. in-person cost differences can sharpen the calculation further.

Reframing the Reddit Question

The original post asked whether a hefty loan for an MBA is worth it. The honest answer depends on three variables: program tier, target industry, and your pre-MBA baseline salary. A $150,000 loan makes sense for a consultant-bound candidate at a top-ten school earning $75,000 today. That same loan becomes a trap for someone targeting corporate finance roles at $95,000 post-graduation from a regional program. Run your own numbers before you sign.

Questions to Ask Yourself

When MBA Debt Is Too Risky

Borrowing for an MBA is not inherently bad, but borrowing without the right conditions in place can set your finances back by a decade or more. Before you sign for six figures in loans, it is worth being honest about whether your specific situation belongs on the safe side of that line.

Four Scenarios Where the Math Breaks Down

Certain combinations of program choice, career target, and personal circumstances make MBA debt genuinely dangerous rather than merely uncomfortable.

- Unranked programs with high sticker prices: A $120,000 debt load is hard to justify at a program with weak employer relationships and modest placement rates. If the school cannot consistently move graduates into roles paying $90,000 or more, the repayment window stretches painfully long.

- No clear post-graduation target: Taking on debt to "figure it out" in business school is an expensive strategy. Lenders do not adjust repayment schedules because your career pivot took longer than planned.

- Existing undergraduate debt above $50,000: Layering a large MBA loan on top of a substantial prior balance means your total debt service can easily consume 20 to 25 percent of a mid-range post-MBA salary before you account for rent, taxes, or retirement contributions.

- Target industries with compressed salaries: Nonprofit management, K-12 education administration, government, and early-stage startup roles frequently pay in the $60,000 to $85,000 range even for MBA holders. At those income levels, a $100,000-plus loan balance is not a manageable burden; it is a years-long constraint on every financial decision you make.

The Prestige Trap

One of the subtler risks is borrowing heavily for a brand-name program while planning to enter a field where that brand does not translate into premium compensation. A top-ten MBA opens doors in consulting and finance at salaries that can support the debt. The same degree held by someone entering arts administration or community development does not. The school's ranking is irrelevant to your repayment schedule. What matters is the salary your specific career path is likely to produce, and whether that salary can carry the loan. For a deeper look at compensation by role, review our guide to average MBA salary by job title.

Household-Level Risk Factors

Personal circumstances compound the math in ways that median salary figures do not capture. Single-income households have no financial cushion if a job search runs long or a first post-MBA role does not pan out. Dependents, whether children or aging parents, add fixed costs that shrink the income available for debt service. Homeownership aspirations compete directly with loan payments: mortgage lenders count student debt in your debt-to-income ratio, and a large MBA balance can delay or reduce your buying power for years. Understanding how to choose the right MBA program with these constraints in mind can prevent costly mismatches.

The International Student Premium

International students face a structurally different risk profile. Federal loans are not available to non-U.S. citizens, which pushes many candidates toward private international lenders. MPOWER Financing, for example, charges fixed rates between 10.89 and 12.99 percent plus a 5 percent origination fee, with no cosigner required.12 Prodigy Finance, another common option for students at top global programs, carries variable rates ranging from 11.00 to 14.50 percent and can lend up to $220,000.3 Those rates are materially higher than the federal graduate loan rate, meaning the same $100,000 borrowed costs significantly more over a standard repayment period.

Beyond interest rates, visa uncertainty adds a layer of risk that domestic borrowers do not face. An H-1B denial, a change in employer sponsorship policy, or a forced return to a home country market can sharply reduce the post-MBA earnings that were supposed to service the loan. If your repayment plan depends on earning a U.S. salary for the next ten years, that plan needs a realistic contingency for what happens if that path closes.

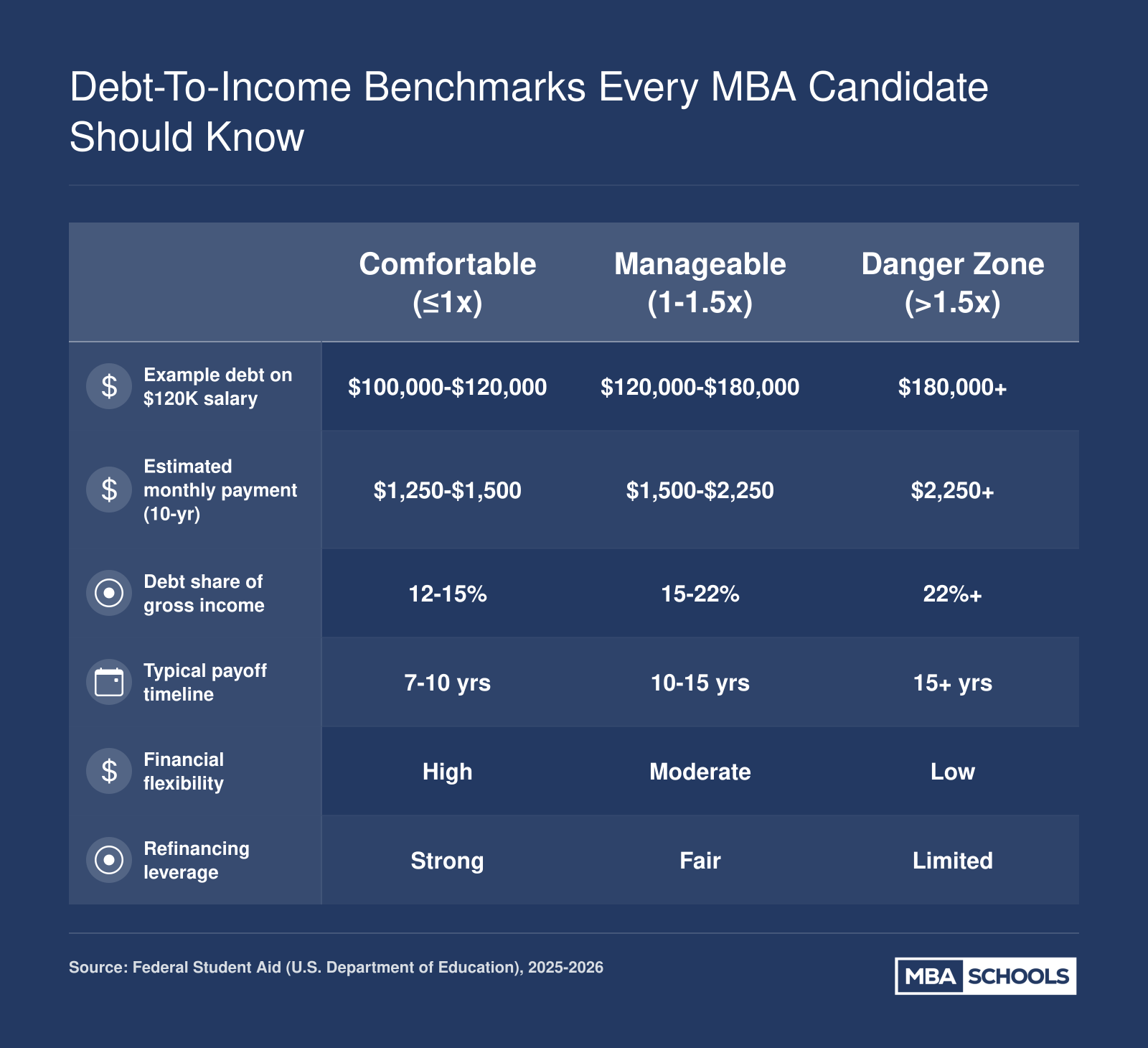

Debt-To-Income Benchmarks Every MBA Candidate Should Know

A useful rule of thumb for evaluating MBA debt is to compare your total borrowed amount against your realistic first-year post-MBA salary. The tiers below map that ratio to approximate repayment timelines and monthly burdens using a blended rate near current federal Grad PLUS levels (8.94% for the 2025-2026 year). Private loan rates vary widely, from roughly 3% to 16%, so your individual numbers may shift, but the framework holds.

Full-Time Vs. Part-Time Vs. Online: How Program Format Changes the Debt Equation

Program format refers to how you structure your MBA experience: enrolling full-time over roughly two years, attending part-time while continuing to work (typically three to four years), or completing a degree online with maximum scheduling flexibility. Each path carries a distinct financial profile, and choosing the wrong format for your situation can add tens of thousands of dollars in unnecessary cost or lost income.

Full-Time Programs: Higher Sticker Price, Higher Opportunity Cost

Full-time MBA programs tend to carry the largest upfront price tag because tuition is typically set at the school's flagship rate, and you forgo a salary for the duration. That combination of tuition plus lost wages creates the steepest total cost of any format. The tradeoff is access to deeper recruiting networks, on-campus experiences, and the strongest post-graduation salary bumps in industries like consulting and investment banking. Before committing, use each school's net price calculator and financial aid pages to estimate realistic out-of-pocket costs after scholarships and grants. The Bureau of Labor Statistics (BLS.gov) publishes occupation-specific salary projections that can help you model whether post-MBA earnings justify the gap in income. If you are still weighing whether the degree itself pencils out, our analysis of is an MBA worth it walks through the ROI calculation in detail.

Part-Time Programs: Lower Headline Cost, Longer Horizon

Part-time students maintain a paycheck, which eliminates the opportunity-cost problem. However, the longer time to degree means more semesters of tuition, fees, and interest accrual on any borrowed funds. Lifetime borrowing costs can rival or even exceed those of a full-time program once you factor in the extended repayment timeline. Check the National Center for Education Statistics (NCES) or the College Scorecard for completion rates filtered by institution type and program format; lower completion rates in part-time cohorts can signal structural challenges worth weighing before you enroll.

Online Programs: Flexibility With Perception Trade-Offs

Online MBAs generally offer the lowest tuition and the greatest flexibility, making them attractive for professionals who cannot relocate or step away from work. The debt equation looks favorable on paper, but employer perception varies by industry. Our guide on what employers think about online MBA degrees explores this dynamic further. Professional associations such as the AICPA, AMA, and IEEE periodically publish hiring-trend reports and salary surveys that break down how employers view different program formats. Reviewing these resources can reveal whether your target industry values the credential itself or the specific format behind it.

How to Compare Formats Systematically

Rather than defaulting to prestige or convenience, run a side-by-side analysis. You can use our compare MBA programs tool to benchmark schools head to head, then layer in the following cost dimensions:

- Total cost of attendance: Include tuition, fees, books, and living expenses for the full duration of the program.

- Forgone income: Estimate the salary and benefits you will lose if you leave work, using BLS data for your current occupation.

- Interest accumulation: Model loan interest over the actual repayment period, not just the in-school period.

- Completion likelihood: Programs with lower completion rates carry a risk of sunk cost without a degree.

- Employer perception in your field: Consult industry association surveys and recruiter feedback to gauge whether online or part-time credentials face a discount in your target roles.

The format that minimizes total debt is not always the format that maximizes career return. A part-time program that costs less per semester could end up more expensive overall, and an online degree that saves money upfront might limit access to certain employers. Match the format to your career goal, then stress-test the numbers before you borrow.

Career-Path Sensitivity: How Your Target Industry Changes the Math

Your target career after business school is arguably the single most important variable in determining whether MBA debt is manageable or crushing. The table below models loan affordability across five common post-MBA career paths, using median starting compensation at top-15 programs and a standard 10-year repayment on a 7% fixed-rate loan. Note that total compensation in consulting and banking often includes significant bonuses, which can accelerate repayment well beyond what base salary alone suggests.

| Career Path | Median Starting Salary (T15) | Monthly Payment on $120K Debt (7%, 10-Year) | Estimated Years to Repay $100K | Estimated Years to Repay $150K | Risk Level |

|---|---|---|---|---|---|

| Management Consulting | $190,000 (base + signing bonus) | $1,393 | 4 to 5 | 6 to 7 | Low to Moderate: High offer rates at target schools, but up-or-out culture creates income uncertainty after 2 to 3 years |

| Investment Banking | $200,000 (base + signing bonus) | $1,393 | 3 to 5 | 5 to 7 | Moderate: Strong starting pay and large performance bonuses, though cyclical hiring and volatile deal flow can affect job security |

| Tech Product Management | $175,000 (base + equity) | $1,393 | 5 to 6 | 7 to 8 | Low: Broad demand across companies, relatively stable hiring, and equity upside can supplement cash compensation significantly |

| Nonprofit and Social Impact | $90,000 to $110,000 | $1,393 | 8 to 10 | 10 to 13 | High: Lower and narrower salary bands with fewer signing bonuses; loan forgiveness programs may help but require specific employer eligibility |

| Entrepreneurship | Highly variable ($0 to $150,000+) | $1,393 | Unpredictable | Unpredictable | Very High: No guaranteed salary post-graduation; founders often forgo income in early years, making fixed debt payments a significant burden |

Strategies to Reduce or Eliminate MBA Debt

Every dollar you avoid borrowing is worth roughly two dollars of post-MBA salary once you account for interest and taxes, which is why aggressive debt reduction before you sign a loan document is the highest-leverage move you can make. The five levers below, used in combination, routinely cut effective MBA cost by a third or more.

Scholarships and Need-Based Aid

Merit scholarships are more common than most applicants assume. Industry survey data suggests roughly 35% of business school students receive merit awards, with another 15% receiving other forms of institutional aid.1 At Harvard Business School, about half of students qualify for need-based scholarships averaging $42,000 per year, or roughly $84,000 across the two-year program.2 Some programs are even more generous: published figures show scholarship receipt rates near 89% at Rice's Jones Graduate School of Business and around 90% at Indiana's Kelley School of Business.2 Across M7 and top-15 programs, partial scholarships typically cover between 25% and 75% of tuition, and average award sizes have been growing roughly 10% annually in recent cycles.4 For a comprehensive look at available awards, our guide to MBA scholarships is a good starting point.

Negotiation is the most underused lever. Many T25 to T50 programs will match or raise an offer when a candidate presents a competing admit with a higher scholarship, particularly during yield season. A polite, specific email comparing total cost of attendance has produced five-figure increases for well-qualified applicants.

Employer Sponsorship, Veterans Benefits, and ISAs

If your current employer will sponsor part or all of tuition in exchange for a return-of-service commitment, the math almost always favors accepting, even with the lock-in. Veterans should fully exhaust Post-9/11 GI Bill benefits and the Yellow Ribbon Program, which together can eliminate tuition at many top schools. Income share agreements still exist at a handful of programs and can hedge downside risk, though terms vary widely and deserve careful legal review.

In-School Earnings and Post-MBA Refinancing

Part-time and online students can apply current salary directly to principal. Full-time students should treat summer internship earnings, often $30,000 to $50,000 at top consulting and banking firms, as a debt-reduction fund rather than discretionary income. Our MBA internship guide covers how to land and convert those offers.

After graduation, refinancing federal and private loans into a single private loan can lower rates meaningfully once you have a high-income job and strong credit. The trade-off is real: refinancing federal loans forfeits income-driven repayment, deferment options, and eligibility for Public Service Loan Forgiveness. PSLF remains a legitimate path for MBA graduates entering qualifying government or nonprofit roles, but only federal loans count, and only after 120 qualifying payments under an eligible employer.

According to the GMAC Prospective Students Survey, 42 percent of prospective business school students now rank return on investment as their top factor when evaluating MBA programs. This shift toward ROI-focused decision making reflects growing awareness that the financial calculus of business school, not just prestige or rankings, should drive enrollment choices.

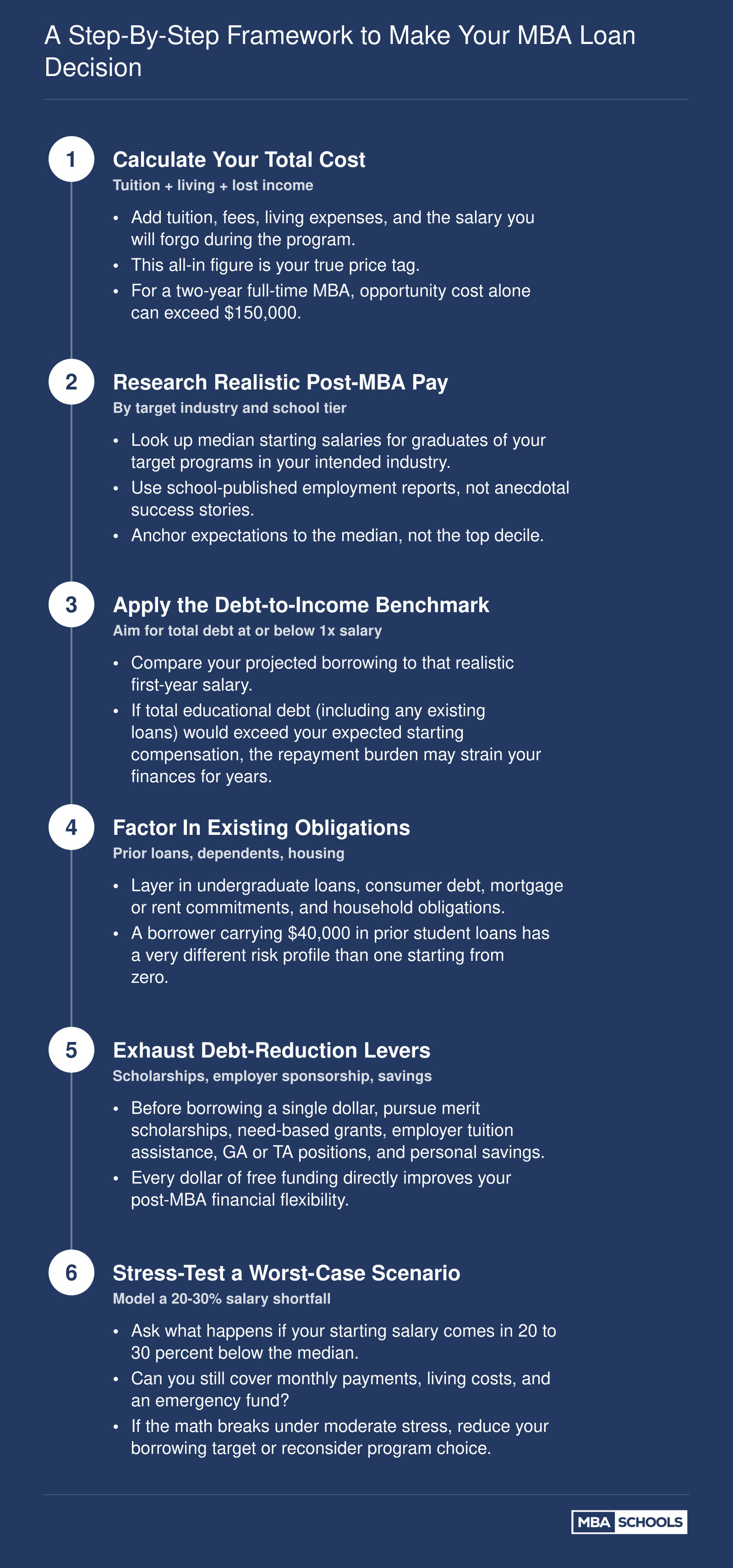

A Step-By-Step Framework to Make Your MBA Loan Decision

Before you sign a promissory note, run your personal numbers through this six-step decision framework. Each step builds on the last, so work through them in order. The goal is to arrive at a borrowing ceiling you can defend with data, not a number you hope will work out.

Frequently Asked Questions About MBA Debt

The financial calculus of borrowing for an MBA generates more questions than most admissions offices are willing to answer directly. Below, we address the most common concerns using the benchmarks and frameworks outlined earlier in this guide.

Related Articles

Taking on MBA debt works when you borrow against a realistic earnings projection, not when you borrow against hope. The six-figure price tag can pay for itself if your target industry and school tier produce the salary multiples the debt-to-income benchmarks demand. If your numbers land in the caution zone, a part-time or employer-funded path preserves upside without the full leverage risk.

Before you sign a promissory note, use the step-by-step framework earlier in this guide. Run your own scenario, isolate your borrowing ceiling, and only proceed if the math holds up under conservative assumptions. For candidates still sorting through program options and financing an MBA, mapping out your funding strategy alongside your school list ensures the decision stays grounded in data from the start.