What you’ll learn in this article…

- A mid-tier full-time MBA can cost roughly $200,000 when tuition, living expenses, lost salary, and loan interest are combined.

- The single biggest ROI driver is the gap between your pre-MBA and post-MBA salary, not school prestige alone.

- Part-time and online formats often improve ROI by eliminating opportunity cost, even if salary gains are smaller.

- Career switchers moving from $55,000 to $165,000 can outperform advancers at pricier programs with narrower salary jumps.

What does an MBA actually cost, and what does it actually return? At top-tier programs, two-year total cost of attendance now exceeds $275,000 before a dollar of forgone salary is counted. Post-MBA median compensation at those same schools clears $175,000, but median is not destiny.

The useful question is not whether you can finance the degree. It is whether the financial return justifies the capital outlay, the borrowing, and roughly two years away from a paying job. The answer shifts substantially based on program cost, scholarship aid, target industry, and whether you are switching careers or advancing within one. Understanding how to pay for an MBA is important, but knowing whether the investment pencils out matters more.

ROI is not a single number. It is a model built from your numbers, stress-tested against a realistic range of post-graduation outcomes.

What MBA ROI Really Means, and Why Most People Calculate It Wrong

The question most prospective MBA students ask is whether a higher salary after graduation justifies the cost of the degree. That framing, while understandable, leads to a flawed analysis. A true MBA ROI calculation is not a simple before-and-after salary comparison. It is a net financial gain measured against the full investment you make to earn the degree, including money you never see on a tuition bill.

The Core Formula in Plain English

MBA ROI can be expressed as:

ROI = (Cumulative Post-MBA Earnings minus Cumulative No-MBA Earnings minus Total Cost of MBA) divided by Total Cost of MBA

Each variable deserves a clear definition:

- Cumulative Post-MBA Earnings: The total compensation you expect to earn over a defined period (often 10 or 20 years) after completing your MBA, including base salary, bonuses, and equity.

- Cumulative No-MBA Earnings: What you would have earned over that same period if you had never enrolled, factoring in normal raises and promotions in your current career trajectory.

- Total Cost of MBA: Tuition, fees, living expenses, loan interest, and opportunity cost (the income you forgo while enrolled full time).

The result is typically expressed as a percentage. A positive number means the degree created net financial value over your chosen time horizon. A negative number means it did not, at least within that window.

Why Payback Period Matters More Than the Percentage

A raw ROI figure can be misleading without context. Imagine two graduates who both calculate a 200% ROI. One reaches that mark in five years; the other needs fifteen. The first scenario means rapid wealth acceleration. The second means more than a decade of waiting before the investment fully compounds, during which time career disruptions, industry shifts, or personal priorities could intervene.

For most working professionals, the payback period (how many years it takes for your cumulative salary premium to exceed your total cost) is the more actionable metric. A shorter payback period reduces risk and frees you to make career decisions without the weight of unrecovered costs.

The Mistakes That Skew Almost Every DIY Calculation

Three errors appear repeatedly when candidates run their own numbers:

- Ignoring opportunity cost: If you leave a $90,000 salary to attend a two-year full-time program, $180,000 in lost wages belongs on the cost side of the ledger. Omitting it can cut your perceived total investment nearly in half.

- Using median salary data as your personal projection: Published median salaries for a school's graduating class include career paths, geographies, and industries that may not match yours. A median consulting salary in New York is not a realistic projection for someone planning to work in nonprofit management in the Midwest.

- Forgetting loan interest: Federal Graduate PLUS loans and private MBA loans carry interest rates that add tens of thousands of dollars to your total repayment over a standard 10-year term. The sticker price of tuition and the amount you actually repay are meaningfully different numbers.

Getting these inputs right is the foundation of every calculation that follows. Before diving into the numbers, it helps to understand the full landscape of how to pay for an MBA, since your funding mix directly shapes total cost. Likewise, candidates weighing whether going into debt for an MBA is worth it should model realistic loan interest scenarios rather than relying on tuition alone. The sections ahead walk through each component in detail so you can build a projection that reflects your situation, not an idealized average.

Total Cost of an MBA: Beyond Tuition

At MIT Sloan, the total cost of attendance for the 2024, 2025 academic year reached $276,620, even though tuition alone was $178,000.1 That gap, nearly $100,000, is not a rounding error. It reflects the living expenses, health insurance, books, technology fees, and other costs that schools are required to disclose but that applicants routinely underweight when building their financial case for enrolling.

What Tuition Does Not Cover

Tuition typically accounts for 50 to 70 percent of your actual cost of attendance at a full-time program. The remainder falls into a predictable set of categories:

- Living expenses: Rent, food, and transportation for two years in a major metropolitan area can easily reach $40,000 to $60,000 in total, depending on location.

- Health insurance: Most full-time programs require students to carry coverage. School-sponsored plans commonly run $3,000 to $5,000 per year.

- Books and course materials: Case-method programs in particular require substantial reading packets. Budget $2,000 to $4,000 over the program.

- Technology and activity fees: Mandatory fees for software, career services, and student organizations add another $2,000 to $5,000 annually at many schools.

When you add these together, the sticker price you see on a school's admissions page understates what you will actually spend.

Tuition Ranges by School Tier

To give you a working framework, here is where program costs tend to cluster as of 2024 to 2026:

- M7 programs (Harvard, Wharton, Stanford, Booth, and peers): Tuition runs $170,000 to $180,000 for the full program, with total cost of attendance between $260,000 and $270,000. Stanford GSB, for instance, reported a total cost of $271,542 for 2024-2025.1

- Top-25 non-M7 programs: Tuition of $150,000 to $175,000, with total attendance costs between $230,000 and $260,000.1

- Top-50 programs: Tuition of $120,000 to $160,000, and total costs ranging from $200,000 to $240,000.1

- Unranked and regional programs: Tuition can drop to $40,000 to $90,000, with total costs between $80,000 and $150,000, making these programs structurally different ROI propositions.2

Part-time M7 programs are a notable exception: their tuition often reaches $180,000 to $200,000, and because students remain employed, living costs are not the same kind of two-year burden, though the timeline stretches considerably.1 For a deeper look at funding strategies across these tiers, see our guide on how to pay for an MBA.

The Opportunity Cost No One Advertises

None of the figures above include what may be the single largest cost of a full-time MBA: the salary you stop earning while you are in school. For a professional earning $80,000 per year, a two-year program represents $160,000 in foregone income before a dollar of tuition is paid. At $120,000 per year, the figure becomes $240,000. This income does not disappear from your bank account in a single transaction, which is why it feels abstract, but it is as real as any tuition bill.

When you borrow to cover program costs, interest compounds that reality further. A $150,000 loan at 7 percent repaid over ten years generates more than $60,000 in interest, pushing your true cash outlay well past the sticker price. A complete ROI calculation has to start here, with total cost including foregone earnings and financing costs, not just the number on the admissions website. Before taking on that level of debt, it is worth evaluating whether an MBA is worth it in 2026 given your specific career trajectory.

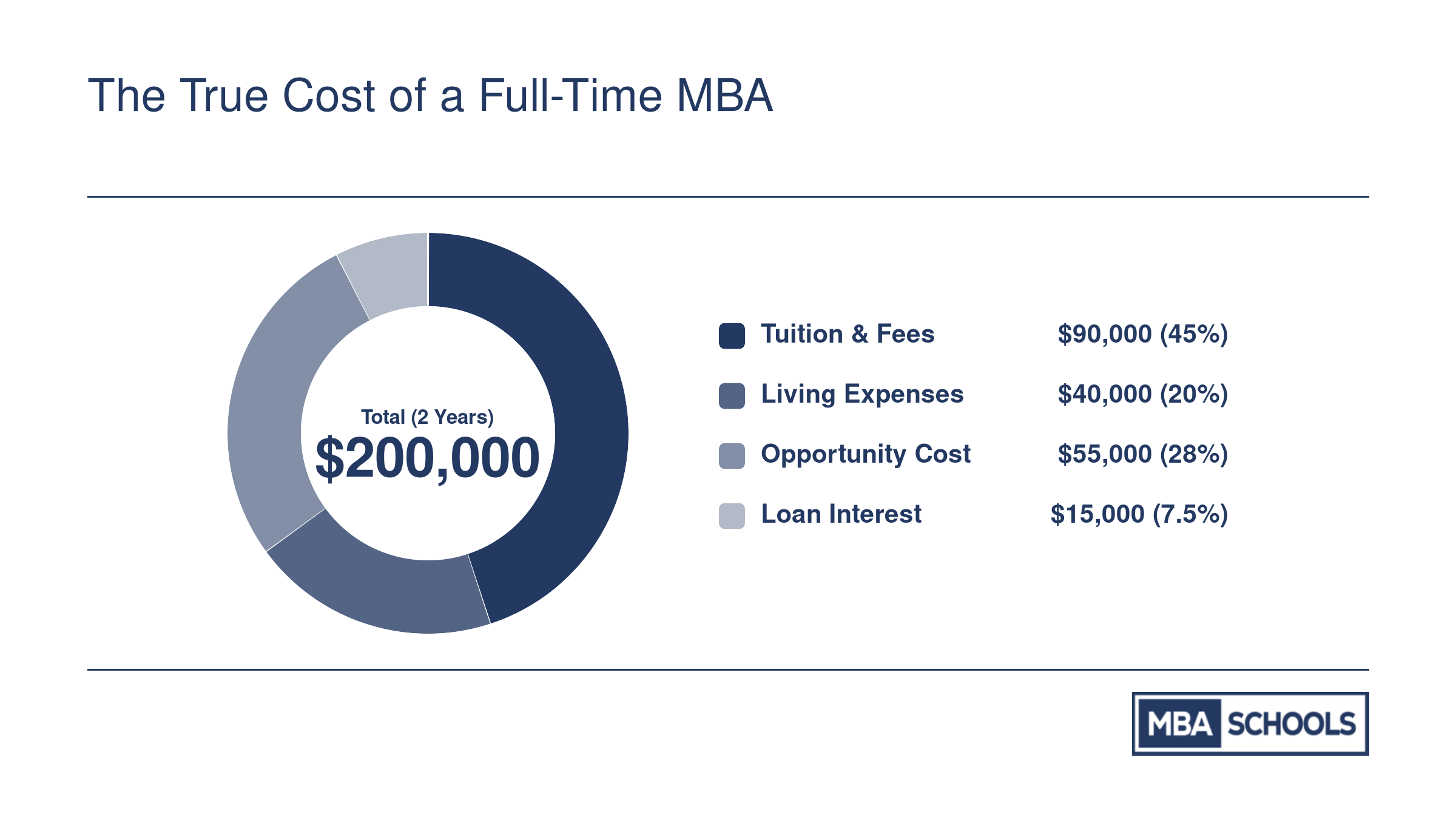

The True Cost of a Full-Time MBA

Tuition is only part of the picture. When you add living expenses, the salary you forgo for two years, and loan interest, a mid-tier full-time MBA can run roughly $200,000. The breakdown below shows how each component contributes to that total, giving you a realistic starting point for your own ROI calculation.

Estimating Your Post-MBA Salary and Earnings Curve

Where you land financially after an MBA depends less on the degree itself and more on the program you attend, the industry you enter, and how far your total compensation stretches beyond base pay.

Find Realistic Numbers, Not Averages

The worst thing you can do is Google "average MBA salary" and build a business case around the result. Aggregated numbers blend M7 consulting hires with part-time graduates who stayed in the same job, producing a figure that describes almost no one's actual experience.

Instead, triangulate from three sources:

- School employment reports: Every accredited program publishes post-graduation employment data. Look for median base salary, median signing bonus, and the percentage of graduates who accepted offers within three months of graduation. These are real numbers for real graduates.

- GMAC Corporate Recruiters Survey: This annual report shows what employers across industries actually plan to pay MBA hires, broken out by function and sector.4

- Glassdoor and Levels.fyi: For finance and technology roles especially, these platforms provide granular compensation data by firm, level, and location that school reports sometimes obscure.

Total Compensation Is the Real Metric

Base salary is a starting point, not the full picture. At top consulting and finance firms, signing bonuses commonly run $25,000 to $50,000 in the first year alone. Annual performance bonuses in finance and consulting typically add 20 to 40 percent on top of base. In technology, equity grants can dwarf both, particularly at growth-stage companies where an MBA hire might receive four-year vesting packages worth several times their annual salary. For a deeper look at how compensation varies across functions, see our guide to MBA career paths and salaries.

When you model your post-MBA earnings, use total first-year compensation as your baseline, not base salary in isolation.

Salary Benchmarks by School Tier

Here is where the market currently stands for 2026 graduates, based on recent school employment reports and GMAC data:

- M7 programs (Harvard, Stanford, Wharton, Booth, Sloan, Kellogg, Columbia): median base salaries ranged from $185,000 to $210,000 for the Class of 2024, with total first-year compensation for M7 graduates running $200,000 to $230,000 once bonuses are included.1

- Top-25 programs (non-M7): Median total compensation falls in the $150,000 to $190,000 range.1

- Top-50 programs: Typically $120,000 to $150,000 in total first-year compensation.1

- Unranked programs: Starting compensation generally ranges from $80,000 to $120,000, with significant variation by geography and industry.2

These ranges are medians. The distribution within each tier is wide. A Kellogg graduate entering nonprofit management will earn far less than a classmate joining a bulge-bracket bank.

The Earnings Curve Matters More Than Year One

A single starting salary tells you almost nothing about an MBA's lifetime value. The more important question is how the earnings curve unfolds over 10 to 20 years.

In consulting and finance, MBA hires move through structured promotion tracks where the degree is often a prerequisite for advancement to manager and partner-level roles. The salary gap between an MBA holder and a non-MBA widens substantially at the senior level. In technology, the curve is less linear but equally steep for those who move into product management or general management roles where MBA training is valued.

For career changers, the curve analysis is especially important. Year-one post-MBA compensation may not exceed what you earned before school once you account for the career reset. Year-five and year-ten numbers, by contrast, often justify the initial dip. That compounding dynamic is why payback period calculations, covered in the next section, matter so much. You can also explore average salary for MBA graduates across experience levels to ground your projections in current data.

Questions to Ask Yourself

Step-By-Step: How to Calculate MBA ROI and Payback Period

A credible MBA ROI calculation is not a single number. It is a year-by-year comparison of two financial futures: the one where you earn the degree and the one where you do not. Here is the framework we recommend working through before you sign a loan promissory note.

The 5-Step ROI Framework

- Step 1, total cost: Add tuition, fees, books, health insurance, living expenses for the program length, and projected loan interest. For a full-time program, include the opportunity cost of foregone salary and any employer benefits you walk away from.

- Step 2, no-MBA earnings trajectory: Project what you would realistically earn over the next 10 years without the degree. Use your current base salary, assume a 3 to 5 percent annual raise, and factor in any promotion you would likely receive on your existing track.

- Step 3, post-MBA earnings trajectory: Estimate your starting post-graduation salary (use your target school's employment report for your intended function and industry), then apply a 6 to 10 percent annual growth rate for the first decade.

- Step 4, net gain: Sum your cumulative post-MBA earnings over 10 years, subtract your cumulative no-MBA earnings over the same period, then subtract total cost from step 1. The result is your 10-year net financial benefit.

- Step 5, payback period: Track cumulative net gain year by year. The payback year is the first year that running total turns positive.

A Worked Example

Consider a candidate earning $75,000 pre-MBA who attends a top-25 full-time program with a $200,000 all-in cost (tuition, living, and roughly $160,000 in foregone salary across two years). She lands a $140,000 post-MBA role with a $20,000 signing bonus.

Without the MBA, at 4 percent annual growth, she would earn roughly $900,000 cumulatively over 10 years. With the MBA, starting at $140,000 and growing 7 percent annually, she earns roughly $1.93 million across years 3 through 12. Net earnings gain: about $1.03 million. Subtract $200,000 in cost, and the 10-year net benefit lands near $830,000. Her cumulative position turns positive around year 6, which is her payback point.

What Counts as a Good Payback Period

Under 5 years is strong and typical of top-tier graduates moving into consulting, banking, or tech product roles. Five to 7 years is reasonable and describes most solid mid-tier outcomes. Anything beyond 10 years is a warning sign: it usually means the cost was too high, the salary lift too modest, or both. When choosing the right MBA program for your career goals, payback period should rank alongside reputation and curriculum on your decision checklist.

You can build this in a basic spreadsheet with two columns (no-MBA and post-MBA earnings), one cost row, and a running cumulative total. Generic online MBA ROI calculators are useful as a sanity check, but they default to average inputs. If you are weighing a part-time or online format, understanding how much an online MBA costs can sharpen the cost side of your model. A spreadsheet you control, populated with your actual salary, target school cost, and realistic post-MBA offer range, will always beat a one-size-fits-all tool.

Related Articles

ROI by Program Format: Full-Time Vs. Part-Time Vs. Online MBA

The decision between full-time, part-time, and online MBA formats often shifts ROI by tens of thousands of dollars. Not because one format is inherently superior, but because each routes cost, time, and career impact through a different equation.

Weighing Time and Income Across Formats

A full-time MBA typically requires leaving the workforce for two years, sacrificing current salary and benefits. The payoff is accelerated career progression, intensive networking, and access to on-campus recruiting pipelines. Part-time and online programs allow you to keep earning, which dramatically reduces opportunity cost, but they extend the calendar commitment and may offer less immediate career-switching leverage. When calculating ROI, the pre-MBA salary you forgo is a cost that varies sharply by format, and the speed at which you re-enter a higher-paying role determines your payback period.

- Full-time: Highest opportunity cost, fastest credential timeline, strongest recruiting placement for career changers.

- Part-time: Lower opportunity cost, longer timeline, often used by advancers within their current industry.

- Online: Lowest opportunity cost, flexible schedule, but variable employer recognition and networking depth.

Salary and Career-Switching Potential by Format

Program format correlates with typical career outcomes. Full-time graduates frequently pivot into new industries or functions, leveraging internships and company presentations to land best jobs for MBA graduates. Part-time and online students more often accelerate within their current trajectory. The Bureau of Labor Statistics provides occupational salary data that can ground your post-MBA earnings estimate, but you must align your target role with the format you pick. A career changer looking at consulting or investment banking will find the full-time pipeline nearly essential; an operations manager aiming for a director role may see a part-time program deliver the needed credential without the income interruption.

Using Public Data to Build Your Calculation

Start with broad occupation-level earnings from BLS.gov for roles you would pursue after graduation, then layer on program-specific outcomes from individual school websites. Many MBA programs publish employment reports segmented by format: average starting salary, signing bonus, and employment rate at three months. Comparing these figures across full-time, part-time, and online cohorts at the same school can reveal gaps that matter for your estimate. If you are weighing the online route, understanding online MBA cost in detail is an essential step. Professional associations like GMAC and AACSB periodically survey employer perceptions and enrollment trends, often highlighting that while full-time programs dominate top-tier consulting and finance recruiting, employers increasingly view part-time and online degrees from accredited institutions as comparable for experienced hires.

Avoiding the One-Number Trap

The most common ROI mistake is assuming the same post-MBA salary regardless of format. A personalized estimate should weigh your current salary, the format's time commitment, the realistic career outcomes given your background, and any debt you take on. Combining BLS benchmarks with school-specific placement data and adjusting for geographic region and industry gives a grounded range, not a single payoff number, that reflects what each format can actually deliver.

How Career Goals Change ROI: Switchers Vs. Advancers

Your MBA ROI calculation hinges on a critical question: are you using the degree to advance in your current industry, or to switch into a new one? The financial outcomes differ dramatically between these two paths.

Career Advancers: Shorter Payback, Lower Risk

Career advancers enter an MBA with domain expertise and exit with enhanced credentials, broader networks, and faster promotion trajectories. Because they remain in familiar industries, they typically negotiate higher starting salaries, assume less re-entry risk, and reach breakeven faster. Pre-MBA compensation often sits in the moderate-to-high range already, and post-MBA gains reflect accelerated progression rather than a full career reset.

Advancers in fields like technology, finance, and healthcare management often see salary lifts of 30 to 50 percent, though the percentage gain may appear smaller than switchers' simply because the starting base is higher. The payback period is usually shorter because there is less income volatility and fewer months spent rebuilding industry credibility.

Career Switchers: Higher Ceiling, Longer Climb

Career switchers face a more complex ROI equation. Moving from software engineer to investment banking, nonprofit work to corporate strategy, or military service to management consulting can yield substantial long-term earnings, but the transition carries higher upfront risk and a longer path to profitability.

Post-MBA salaries for switchers entering high-paying fields like management consulting or investment banking can be substantial, but the pre-MBA baseline is often lower, making the percentage increase appear large while the absolute payback period extends. Switchers also absorb learning curves, may accept lower first-year bonuses, and sometimes require additional months to secure the right role, all of which delay ROI.

School employment reports break down outcomes by industry and career path. Harvard, Stanford, Wharton, and peer institutions publish detailed statistics showing median compensation by function and sector, often distinguishing switchers from advancers. The Bureau of Labor Statistics offers industry-specific benchmarks and ten-year growth projections, useful for stress-testing your assumptions about future earnings. GMAC's Alumni Perspectives Survey aggregates salary changes across career goals and industries.

The ROI Implication

If you are advancing within your field, calculate ROI assuming a shorter payback window and lower variance. Choosing the right MBA specialization can further sharpen your ROI by aligning coursework with high-demand skills in your sector. If you are switching, model conservatively: assume a longer breakeven period, potential for lower first-year bonuses, and the possibility that the target role takes an extra recruiting cycle to secure. Both paths can justify the investment, but only if your financial model reflects the realities of your specific trajectory.

Scholarships, School Tier, and Geographic Factors That Shift ROI

The sticker-price-versus-actual-cost gap at U.S. business schools has widened sharply in the past few years, and that gap is now the single biggest variable in any honest ROI calculation. Two candidates admitted to the same program in the same year can face cost structures that differ by $150,000 or more, enough to swing payback period by half a decade.

How Scholarships Reshape the Math

Merit aid is now the norm rather than the exception, even at elite programs. Roughly 45 to 55 percent of M7 students receive some form of scholarship, with average annual awards between $30,000 and $55,000.1 Harvard Business School reports that about half of its students receive need-based aid averaging roughly $100,000 over two years. Stanford GSB averages about $47,000 per year for fellowship recipients. Wharton funds about a third of its class at an average of $30,500 annually, while Chicago Booth awards merit aid to roughly 60 percent of students at an average of $30,000 per year. NYU Stern is notably tighter, funding only 20 to 25 percent of its class.2 For a deeper look at available awards, our guide to MBA scholarships breaks down program-specific opportunities and application strategies.

Outside the M7, the discounting gets aggressive. Top-25 non-M7 programs scholarship 40 to 65 percent of students, with awards typically totaling $40,000 to $70,000 across two years. Rice Jones funds 94 percent of its class at an average of $33,320 per year, which covers roughly 59 percent of tuition.1 Top-50 programs outside the top 25 routinely fund 60 to 80 percent of admits, and lower-ranked programs often discount tuition 40 to 60 percent for the majority of their students.

The Tier Tradeoff

This is where ROI rankings diverge from prestige rankings. A 50 percent scholarship at a top-25 program can compress payback period by two to three years compared to paying full freight at an M7. If the post-MBA salary delta between the two programs is $20,000 to $30,000 (often the realistic gap for finance and consulting roles), the discounted top-25 option frequently delivers a higher lifetime ROI. M7 programs still win on raw compensation and access to certain employers, but they do not automatically win on return.

Geography Eats Salary

Post-MBA base salaries cluster highest in New York, San Francisco, and Boston, but cost of living erodes much of the advantage. A $160,000 offer in Dallas or Atlanta typically delivers more take-home purchasing power than $190,000 in San Francisco once housing, state income tax, and daily expenses are netted out. Career changers targeting tech or finance hubs should model the after-tax, after-rent number, not the headline figure. Fellowships like Reaching Out MBA (up to $35,000) and Forté can further tilt the equation for eligible candidates, and financial aid for minority MBA students may open additional funding pathways that dramatically improve ROI.

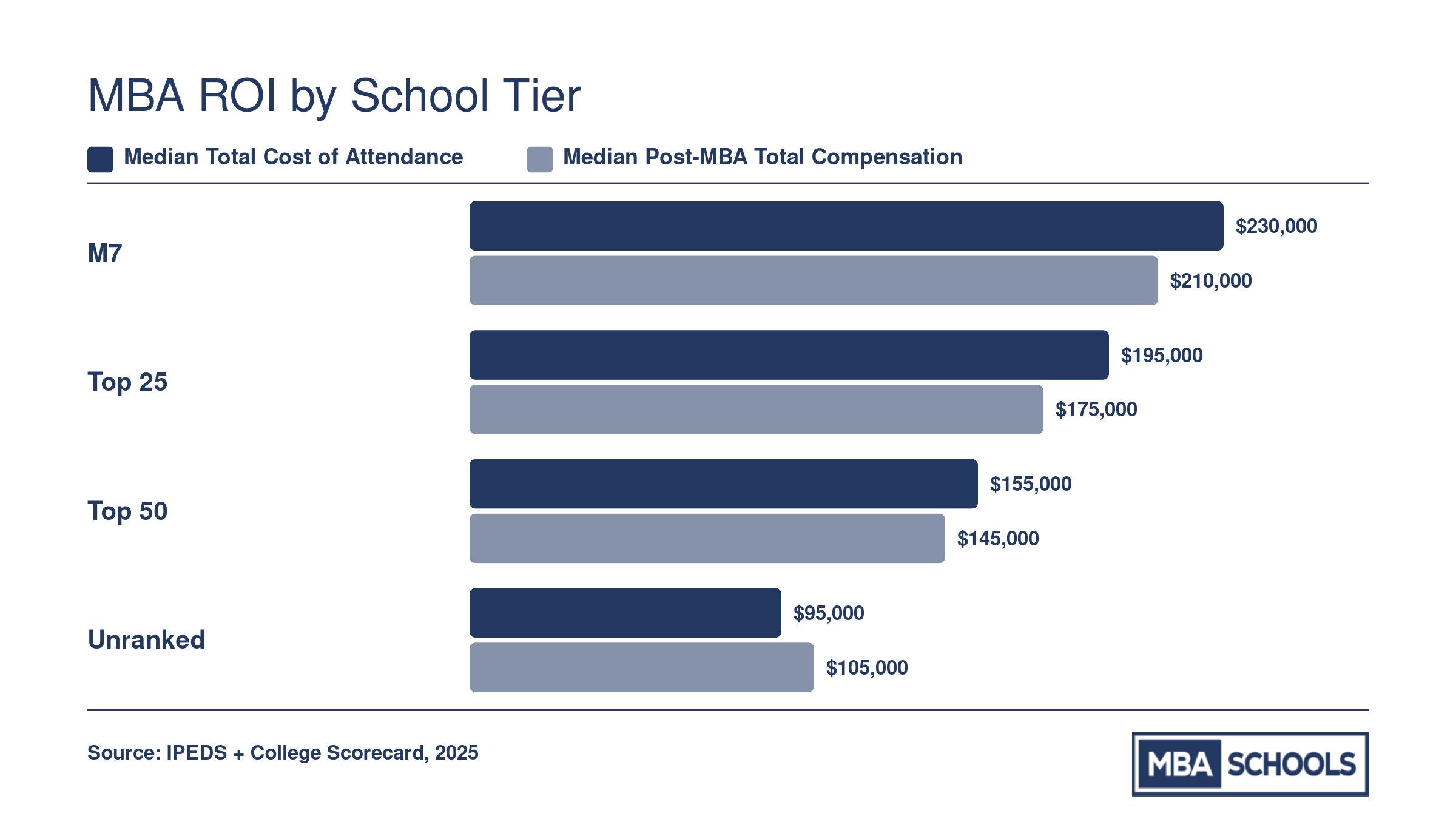

MBA ROI by School Tier

Program cost and post-MBA earnings vary dramatically depending on where a school falls in the rankings. The chart below compares median total cost of attendance (tuition, fees, and living expenses over two years) against median first-year post-MBA total compensation across four commonly referenced tiers. Both sides of the equation matter: a lower-cost program can deliver stronger ROI than a prestigious one if the salary gap is modest.

Conservative, Moderate, and Optimistic ROI Scenarios

No single number captures MBA ROI because outcomes vary widely based on the job market, scholarships, industry placement, and salary trajectory. The three scenarios below use the same starting assumptions from the step-by-step calculation (a pre-MBA salary of $75,000 and a two-year full-time program) but adjust cost inputs and post-graduation outcomes to reflect a realistic range. Factors that push results toward the conservative end include graduating into a recession or weak hiring cycle, failing to land a role in your target industry, an extended job search of three months or longer, and, in the worst case, leaving the program before completing the degree.

| Scenario | Total Cost (Tuition, Fees, Living, Opportunity Cost) | Year-1 Post-MBA Salary | Annual Salary Growth Rate | Payback Period | 10-Year Cumulative ROI |

|---|---|---|---|---|---|

| Conservative (no scholarship, weak job market, slower growth) | $310,000 | $105,000 | 3% | 7 to 8 years | Approximately $180,000 |

| Moderate (median outcomes, modest aid) | $260,000 | $130,000 | 5% | 4 to 5 years | Approximately $520,000 |

| Optimistic (significant scholarship, top-quartile salary, strong growth) | $200,000 | $165,000 | 7% | 2 to 3 years | Approximately $1,000,000 |

Common MBA ROI Questions, Answered

These are the questions working professionals ask most often when weighing the financial case for business school. Each answer draws on the frameworks and figures discussed throughout this guide.

Cost versus outcome: that is the tension every MBA candidate must resolve before committing to a program. The analysis throughout this guide shows that the degree is not automatically worth it, and the price tag alone does not settle the question.

MBA ROI is strongest when three conditions align: the salary gap between your current trajectory and your post-MBA path is substantial, the total cost is managed through scholarships or a lower-cost program, and the credential itself is required to reach your career goal. Career switchers moving into consulting or finance often clear these bars; advancers in industries where the MBA is optional frequently do not. Run your own numbers, use conservative salary assumptions, and factor in every cost component before deciding. The math, not the prestige, should drive the decision.