What you’ll learn in this article…

- Start researching program costs and funding sources 12 to 18 months before enrollment to maximize scholarship eligibility.

- Round 1 applicants (September to October) historically receive the largest share of merit scholarship dollars.

- Grad PLUS loans end July 1, 2026, so fall 2026 enrollees must model borrowing needs under new federal caps immediately.

- File the FAFSA as close to the October 1 opening as possible to secure the cleanest path to need-based aid.

When do you actually need to apply for MBA financial aid? For fall 2026 matriculants, the process starts up to 18 months before your first class and continues past graduation. July 2026 federal loan reforms eliminate Grad PLUS and cap graduate borrowing, so the timeline has immediate consequences: missed deadlines now mean losing access to programs that may not exist later. The funding sequence stretches from initial program research through acceptance, award comparison, deposit coordination, FAFSA filing, and employer reimbursement, with no single application date that covers everything. This guide walks you through each phase, from mba scholarships and fellowships to loan finalization, so you can treat the process as a multi-year project rather than a one-time form.

12–18 Months Before Enrollment: Research Programs, Costs, and Funding Sources

The earliest decision you face is not which school to attend, but how much financial uncertainty you are willing to carry into a two-year program. Starting the funding conversation 12 to 18 months ahead lets you trade guesswork for a structured plan, and it puts you in front of the deadlines that quietly close before most applicants even submit Round 1.

Why the Clock Starts So Early

Many of the most valuable external scholarship pipelines run on their own calendar, not the school's. The Forté Foundation MBA Launch program for women, The Consortium for Graduate Study in Management, and the Toigo Foundation fellowship for underrepresented candidates all have application cycles that open in the summer and close in the fall, often before Round 1 admission decisions are released. If you wait until you are admitted to start looking for outside money, you have already missed the largest pools. Our guide to MBA scholarships offers a comprehensive list of awards worth exploring at this stage.

Use this window to build a target list of 6 to 10 programs, register for early scholarship databases, and flag every fall and winter deadline on a single calendar.

Estimating the True Cost of Attendance

Published tuition is the headline number, not the full bill. A realistic two-year budget includes:

- Tuition and required fees: the figure quoted on the program's cost page

- Living expenses: rent, food, transportation, and health insurance, which vary sharply by city

- Program costs: books, technology, treks, club dues, and case competition travel

- Opportunity cost: the salary and bonuses you forgo while in school, often the single largest line item

Build a spreadsheet for each target school using its official cost of attendance, then layer in your own city-specific living estimates. The gap between two programs with similar sticker prices can exceed $40,000 once geography and lost income are factored in honestly. If budget is a primary concern, reviewing affordable MBA programs early can reshape your target list.

Open the Employer Conversation Now

If your company offers tuition reimbursement or full sponsorship, the approval process is rarely fast. Many corporate programs require 6 to 12 months of pre-approval paperwork, manager sign-off, and a service agreement spelling out post-MBA commitments. Request a meeting with your manager and HR early so you understand the cap, the eligible program types (full-time, part-time, executive, online), and any clawback terms before you commit.

Build a Personal Funding Map

Think of your total cost as something you will assemble from six buckets: school-based merit scholarships, need-based aid, federal loans, private loans, employer funding, and personal savings. Sketch a rough percentage for each bucket now. That map tells you where to spend your application effort, whether the FAFSA for MBA students matters for your situation, and how much gap you may need to close through borrowing or savings.

9–12 Months Before Enrollment: Prepare Applications and Scholarship Materials

Round 1 applicants, those submitting between September and October, historically receive the largest share of merit scholarship dollars at most MBA programs. That reality makes financial aid strategy and admissions strategy inseparable: if you want to maximize funding, you need your scholarship materials ready on the same timeline as your Round 1 application, not weeks later.

Align Scholarship Efforts With Admission Rounds

Most business schools allocate a fixed pool of merit aid across their MBA admissions rounds. By Round 2 (typically January), a significant portion of that pool has already been committed. By Round 3, scholarship funds may be nearly exhausted. If finances are a deciding factor in whether you pursue an MBA, treat a Round 1 submission as the default plan. That means finalizing your GMAT or GRE scores, essays, letters of recommendation, and any school-specific scholarship applications during the summer before enrollment year.

Build a Named-Scholarship Calendar

Several major external fellowships operate on their own timelines. Map them against your target admission rounds so nothing slips through.

- Forté Fellows: Apply through Forté member schools during the regular admissions cycle. Round 1 deadlines fall in September to October, with later rounds in January and March to April. Awards reach up to £40,000 at participating programs. All nationalities, genders, and gender identities are eligible.1

- Consortium for Graduate Study in Management: A single Consortium application replaces individual school applications at member programs. The early deadline is typically mid-October, with a final deadline in early January. Fellows receive full tuition and mandatory fees for two years. Eligibility requires U.S. citizenship or permanent residency and a demonstrated commitment to advancing racial diversity in business.2

- Robert Toigo Foundation Fellowship: Applications open after MBA admission, generally February through June. Awards range from $10,000 to $15,000 and target underrepresented minorities pursuing finance careers.2

- Reaching Out MBA (ROMBA) Fellowship: Schools nominate admitted ROMBA Fellows, with Round 1 nominations in September to October and Round 2 in January. Awards range from $10,000 to $20,000 for LGBTQ+ candidates or those with sustained LGBTQ+ community leadership.2

- Prospanica Graduate Scholarship: A direct application open April through June, offering $2,000 to $10,000 for Hispanic and Latinx students with a minimum 3.0 GPA. Prospanica has awarded over $30 million to date, and awards are stackable with school grants and other merit aid.2

For a broader look at identity-based funding, see our guide to minority MBA financial aid, which covers additional fellowships and need-based programs.

Gather Financial Documents Early

Some MBA programs require the CSS Profile alongside or instead of FAFSA to determine need-based aid. The CSS Profile asks for more granular financial detail, so begin collecting the following well before deadlines arrive:

- Prior-year federal tax returns and W-2s

- Current bank and investment account statements

- Records of any outstanding debt, including undergraduate student loans

- Business or partnership tax filings if you are self-employed or own a stake in a business

Having these documents organized in advance prevents last-minute scrambling that can cause you to miss priority filing windows.

Start the Employer Sponsorship Conversation Now

If your company offers tuition reimbursement or sponsorship, do not wait for an admission letter to begin the internal process. Many employers tie funding approvals to their fiscal-year budgets, with internal deadlines falling three to six months before the fiscal year starts. Identify the right contact in your HR or learning-and-development department, request the formal policy in writing, and clarify whether approval requires a manager endorsement, a commitment to return to the company post-MBA, or both. Beginning this conversation nine to twelve months out gives you time to navigate corporate bureaucracy without jeopardizing your enrollment timeline.

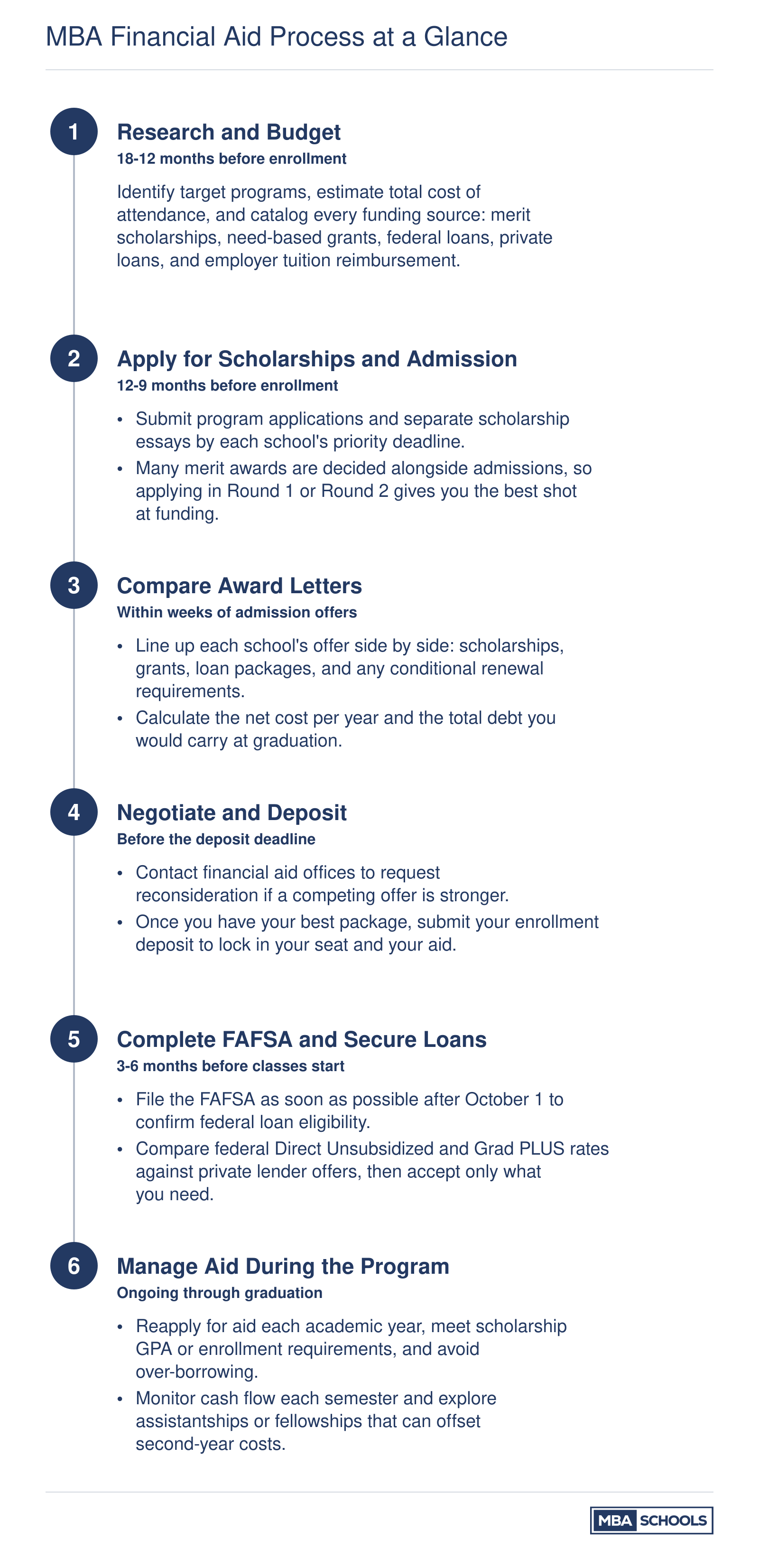

MBA Financial Aid Process at a Glance

Use this six-step sequence as your master roadmap. Each phase builds on the one before it, so staying ahead of deadlines is the single most important thing you can do to maximize funding.

After Admission: Compare Award Letters and Negotiate Scholarships

The window between receiving an admission offer and submitting your enrollment deposit is the single most consequential period for maximizing your MBA financial aid. During this narrow timeframe, you must decode award letters, compare packages across schools, and pursue scholarship negotiations before deadlines close your options.

Locating Official Deadlines and Award Information

Every school maintains its own timeline for releasing financial aid decisions, and these dates rarely align perfectly with admission notification dates. Some programs release merit scholarship awards alongside the admission decision, while others send financial aid notifications separately, sometimes just days before the deposit deadline.

To find exact dates for your target schools:

- Admitted students portal: After admission, you will receive access to a dedicated portal containing deposit deadlines, financial aid notification dates, and next steps specific to your round.

- Financial aid office contact: Email or call the financial aid office directly to confirm when merit decisions are released and whether you can expect notification before or after your deposit is due.

- Official FAQ pages: Most programs publish round-by-round timelines in the "Admitted Students" or "Financial Aid" sections of their websites.

Do not assume that all top programs follow the same schedule. Some release merit awards within two weeks of admission, while others may take a month or more. If you are admitted in a later round, the gap between notification and deposit deadline may be especially compressed, so understanding MBA application deadlines for each round is critical.

Comparing Award Letters Strategically

Award letters vary widely in format and clarity. Some schools break down tuition, fees, and scholarship amounts in detail, while others present a single net cost figure. When comparing multiple offers, normalize each letter by calculating your out-of-pocket cost per year, accounting for:

- Tuition and mandatory fees

- Scholarship or fellowship amounts (and whether they renew for year two)

- Estimated cost of living in each program's city

- Loan offers, which are not free money and should be considered separately from grants

Online forums such as Clear Admit and GMAT Club often feature threads where admitted candidates share timelines and compare award structures. While these discussions are anecdotal, they can help you understand whether your offer is typical or worth negotiating.

Negotiating Scholarships Before the Deadline

Many MBA programs are open to scholarship reconsideration, particularly if you present a competing offer from a peer institution. Certain demographics may also have access to targeted funding; for example, candidates eligible for MBA scholarships for women or mba scholarships for international students should factor those awards into their negotiation strategy. Approach the process professionally:

- Reach out to the financial aid office with a clear, concise explanation of your situation.

- Share specific details about competing offers, including the amount and program name.

- Emphasize your strong interest in the school and ask whether any additional funding is available.

Not every school will negotiate, and outcomes vary by round and available funds. However, the effort is low-risk and can yield meaningful increases in your award. The key is acting promptly, as most programs cannot consider requests after the deposit deadline has passed.

Questions to Ask Yourself

Before the Deposit Deadline: Coordinate Deposits, Aid, and Deferrals

One of the most stressful moments in the MBA financial aid timeline is the gap between the deposit deadline and the finalization of your full financial aid package. Understanding how to navigate this window can save you thousands of dollars and prevent costly surprises.

The Deposit-vs.-Aid Sequencing Gap

Most business schools require a non-refundable enrollment deposit, typically ranging from $1,000 to $5,000, well before your complete financial aid package is locked in. You may have received a merit scholarship offer at admission, but federal loan details, need-based grants, and outside award processing often lag behind the deposit deadline by weeks or even months. This means you are essentially committing financially before you know your total cost of attendance.

This is normal, not a red flag. Still, treat the deposit as a sunk cost if you ultimately choose another program. Before you pay, confirm in writing which elements of your aid package are already guaranteed and which are still pending. Ask the financial aid office for a preliminary cost-of-attendance estimate so you can compare offers across schools on roughly equal footing.

What Happens to Aid If You Defer

Deferring enrollment is increasingly common, but it introduces real risk to your funding. Most school-based merit scholarships are not automatically guaranteed to carry over to a new enrollment year. The admissions committee may reassess your award based on the incoming class's applicant pool, or the scholarship fund itself may have different allocations. Federal loan eligibility also resets to the new academic year, meaning interest rates and loan limits could shift. For a closer look at how federal loans for MBA students work, review your options well before committing to a deferral.

Before requesting a deferral, ask the school's financial aid office for its written deferral policy. Specifically, find out whether your merit award transfers, whether you will need to reapply for need-based aid, and whether any fellowship stipends or assistantship offers remain valid. Get any commitments in writing rather than relying on verbal assurances.

Negotiating the Deposit Deadline Itself

If you are waiting on a financial aid decision or admission result from a competing program, do not assume the deposit deadline is immovable. Many schools will grant a short extension, particularly if you communicate proactively and explain that you are comparing award letters. A polite, direct email to the admissions office is often all it takes. Frame your request around wanting to make a fully informed decision rather than stalling.

- Ask early: Contact admissions at least one to two weeks before the deadline, not the day of.

- Be transparent: Let the school know you are waiting on a specific competing offer or financial aid decision.

- Document everything: If an extension is granted, confirm the new date in writing so there is no ambiguity.

The deposit deadline is a commitment point, but it does not have to be a pressure point. With the right questions and clear communication, you can protect both your options and your financial position heading into enrollment.

Before Enrollment: Complete FAFSA, Secure Loans, and Finalize Funding

October 1 is the date to circle: the FAFSA opens for the upcoming academic year, and MBA candidates who file within the first few weeks consistently get the cleanest path to need-based grants, federal loans, and school-administered aid that draws from the same financial data.

File the FAFSA and CSS Profile Early

The federal FAFSA has no hard cutoff for MBA students, but priority deadlines at top programs typically fall between February and April for fall enrollment. A handful of schools also require the CSS Profile for institutional need-based awards, and those windows often close earlier than the FAFSA priority date. The practical rule: file both as soon as your prior-prior-year tax data is available. Need-based aid budgets are finite, and early filers reach them while the pool is full. You will need your school's federal code, the prior-prior tax return, and records of assets and untaxed income.

Understand the July 1, 2026 Federal Loan Changes

For any MBA student whose first federal disbursement occurs on or after July 1, 2026, the rules have changed materially.1 Our federal student loans for MBA guide covers the full details, but here are the headlines:

- Grad PLUS is ending: New Grad PLUS originations stop on July 1, 2026. Students whose first Grad PLUS disbursement occurred before that date can generally continue borrowing under legacy rules for a transition period, typically up to three years (Georgetown)3, with some schools applying end dates as late as June 30, 2029 (UC Law SF).4 Confirm your school's specific transition policy in writing.

- New annual caps: Graduate Direct Unsubsidized loans are capped at $20,500 per year, with a $100,000 aggregate. Professional programs (defined narrowly by the Department of Education) carry a $50,000 annual cap and $200,000 aggregate.3

- Combined and lifetime ceilings: Federal graduate and professional borrowing is capped at $200,000 combined, and total federal student loan borrowing across all degrees is capped at $257,500.3

- Proration: Less-than-full-time enrollment triggers a proportional reduction in annual borrowing eligibility.5

Because most MBA programs are not classified as professional under this rule, the $20,500 annual cap will leave a funding gap at virtually every full-time program. Plan for private loans, scholarships, savings, or employer support to fill it.

Shop Private Loans in the Spring

Begin comparing private student loans for MBA programs in March or April for fall enrollment. Look at fixed versus variable rates, cosigner release terms (typically 24 to 48 months of on-time payments), in-school deferment, and grace period length. Get pre-qualified rates from three or four lenders before committing. Disbursement is usually scheduled one to two weeks before classes begin, sent directly to the school, with any refund for living expenses released shortly after.

International Students: Plan Around Federal Ineligibility

International students are generally not eligible for federal loans. The standard playbook is school-administered scholarships and fellowships, U.S. private loans secured with an eligible U.S. cosigner, no-cosigner lenders that underwrite based on the school and post-MBA earning potential (offered at a limited set of programs), or home-country financing and sponsor agreements. For a deeper look at private MBA loans for international students, see our comparison guide. Start this work earlier than domestic peers: cosigner arrangements and cross-border underwriting routinely take 60 to 90 days.

FAFSA and CSS Profile Priority Deadlines at Top MBA Programs

When exactly does each MBA program want your FAFSA or CSS Profile on file?

That is the right question to be asking right now, and the honest answer is: it depends on the school, and the stakes for missing the window are real. Federal rules set October 1, 2025 as the earliest you could have submitted a 2026-2027 FAFSA, and the government's hard deadline runs all the way to June 30, 2027.1 In practice, those outer boundaries are almost irrelevant for MBA applicants, because individual programs set their own priority deadlines far earlier, and missing those internal cutoffs can mean losing access to grant money, institutional loans, or work-study funds.

For the 2026-2027 academic year, the pattern across top-20 MBA programs clusters in the January-through-March window.2 If you are enrolling in fall 2026 and have not already filed, that priority season has passed or is passing now. File as soon as possible and contact your program's financial aid office directly to ask whether late filers are still considered for institutional funds.

Where to Find the Actual Deadlines

The only authoritative source for a program's FAFSA priority deadline is that program's own financial aid webpage. Aggregate deadline lists published by third parties, including well-intentioned comparison sites, go stale quickly. Before you rely on any deadline you find outside a school's official site, verify it by checking the financial aid section of that program's website directly.

For general federal FAFSA information and state deadline lookups, studentaid.gov's 2026-2027 FAFSA form is the right starting point. It will not tell you Harvard Business School's internal priority date, but it will confirm federal processing rules and help you track your submitted application.

CSS Profile Requirements Vary by School

Some MBA programs require the CSS Profile in addition to the FAFSA to assess eligibility for their own institutional grant funds. The College Board's CSS Profile page explains the form itself and lists participating schools, but you should treat that list as a starting point rather than a definitive guide. Programs join and leave the CSS system, and a school may require the Profile for need-based grants but not for merit scholarships, or vice versa.

If a program's website does not clearly state whether the CSS Profile is required, call or email the financial aid office before assuming you do not need it. A brief phone call can prevent a costly oversight.

What to Do If Deadlines Are Not Posted

Occasionally a program's financial aid page is under revision, or deadline information is buried inside a PDF rather than posted prominently. In those cases, reach out directly to the admissions or financial aid office. Ask two specific questions: what is the priority deadline for FAFSA submission, and does the program require the CSS Profile for any of its institutional aid. Get the answer in writing, either via email or by noting the name of the staff member you spoke with and the date of the conversation.

Deadlines move. If you are applying to multiple programs, build a simple tracking document listing each school's priority date and whether the CSS Profile applies. Checking each school's site once per month between October and March is a reasonable habit during your application cycle.

During the Program: Manage Cash Flow, Renewals, and Second-Year Aid

Managing financial aid during your MBA means actively monitoring your funding, meeting renewal conditions, and adjusting your borrowing each semester to match actual needs, not just setting it and forgetting it after enrollment. The key is staying ahead of deadlines and recalibrating your budget as costs evolve.

Maintain Scholarship Eligibility

Most MBA merit scholarships come with renewal requirements. Typically, you must maintain a minimum GPA (often 3.0 or higher) and remain enrolled full-time. Some programs also require you to stay in good disciplinary standing. If your GPA dips below the threshold, you risk losing the award for the second year. Check your original award letter for the exact conditions, and schedule a meeting with the financial aid office if you anticipate difficulty meeting them. In some cases, you may be able to appeal a loss of scholarship due to extenuating circumstances.

File Second-Year Aid Applications

Even if you received aid in your first year, you generally need to reapply for the second year. This often includes filing a new FAFSA and, at some schools, a separate scholarship renewal form. Deadlines for second-year aid are typically in the spring of your first year, February through April, so mark your calendar early. Missing these deadlines can leave you with a gap in funding. The financial aid office will use your updated financial information to reassess need-based aid, but merit scholarships usually renew automatically if you meet the conditions.

Recalculate Borrowing Each Semester

Avoid the trap of borrowing the maximum allowed just because it is available. At the start of each semester, calculate your actual expenses: tuition, fees, housing, books, and a realistic living allowance. Then subtract any scholarships, employer tuition reimbursement, or savings. Only borrow the difference. If you have already accepted a larger loan, you can return unused funds to your servicer within 120 days of disbursement to avoid paying interest on money you did not need. This practice keeps your long-term debt burden manageable.

Understand Part-Time and Online Aid Timelines

If you are in a part-time or online MBA program, your aid disbursement schedule and eligibility windows may differ from the full-time calendar. For example, disbursements might occur at the start of each term rather than once per semester, and loan eligibility may be based on credit hours rather than enrollment status. Employer tuition reimbursement often follows a separate reimbursement cycle, so coordinate submission of grades and receipts promptly. For a full breakdown of online MBA cost factors, review your program's published cost-of-attendance figures alongside your aid package. Contact your program's financial aid liaison to map out a customized timeline.

How Timelines Differ: Full-Time Vs. Part-Time Vs. Online and International Students

Full-time MBA applicants typically navigate a structured admissions cycle with fixed scholarship deadlines tied to application rounds. Part-time and online students, by contrast, often encounter rolling admissions with no round-based scholarship structure, fundamentally altering when and how they secure funding.

Full-Time MBA Timeline

Full-time candidates usually apply in rounds between September and April for a fall start. Because merit scholarships are frequently awarded as part of the admission offer, financial aid applications like the FAFSA should ideally be submitted by the program's priority deadline, often as early as February or March. This synchronized rhythm means you can lock in your funding package right after acceptance, making it easier to compare offers.

Part-Time and Online MBA Timelines

Part-time and online programs admit students on a rolling basis, sometimes with multiple start dates per year. Without strict application rounds, scholarship awards can be less predictable or may not exist at all in the traditional sense. Instead, applicants often secure employer sponsorship for MBA tuition, which is paid per semester after grades post, creating a reimbursement cycle that requires upfront cash flow planning. You may also apply for federal loans at any point, but doing so closer to enrollment ensures funds disburse on time.

- Strategy: Rolling admission means you can apply for aid as soon as you are accepted, but you forfeit the ability to compare multiple offers side by side.

- Employer funding: Many part-time students remain employed and tap company tuition benefits; these typically require supervisor approval and a reimbursement form each term.

International Student Considerations

International applicants face a distinct set of deadlines tied to visa processing. After admission, you must submit proof-of-funds documentation to receive the I-20 form needed for your student visa.1 This documentation must demonstrate you can cover at least the first year's expenses, commonly between $40,000 and $70,000, though total program costs can range from $80,000 to $150,000.2 The proof can come from personal bank statements, loan approval letters, scholarship award letters, or sponsor letters, and all documents must be dated within three months of submission.3 Because international students have limited access to federal loans, many rely on private loans or family resources, making it critical to begin assembling these records as soon as you receive your admission decision.

- Timing: Submit financial documents promptly after acceptance; delays can postpone your I-20 and visa interview.1

- Combined funding: Schools accept a mix of sources, so you can combine a partial scholarship with a loan and savings to meet the threshold.3

- Currency and sponsors: If a sponsor or foreign bank provides funding, letters must be in English and specify exact amounts. Currency exchange rates can affect the total, so plan for a cushion.

Before Graduation and Beyond: Prepare for Repayment and Loan Assistance

Graduation does not end the financial aid process. It begins a new and equally consequential phase, and the decisions you make in the months immediately after finishing your MBA will shape your loan costs for years.

Use the Grace Period Deliberately

Federal student loans come with a six-month grace period after you graduate or drop below half-time enrollment. That window is not a vacation from financial planning. Use it to do three things: enroll in autopay (which typically reduces your interest rate by 0.25 percentage points on federal loans), select a repayment plan that fits your income trajectory, and confirm your loan servicer has your current contact information. Borrowers who coast through the grace period and miss their first payment often face unnecessary penalties and credit damage.

Loan Repayment Assistance Programs

If you plan to enter a nonprofit, government, or social-sector role after your MBA, check whether your program offers a Loan Repayment Assistance Program (LRAP). UC Berkeley Haas, for example, operates an LRAP for graduates whose salaries fall below a defined threshold and who work in qualifying public-interest roles. Several other top programs run similar arrangements. Eligibility rules, income caps, and benefit amounts vary considerably, so review the specifics during your second year, not after you have already accepted a job offer.

Income-Driven Repayment and Public Service Loan Forgiveness

MBA graduates carrying federal Direct Loans may qualify for income-driven repayment plans, which tie monthly payments to a percentage of discretionary income and forgive remaining balances after a set number of years. Public Service Loan Forgiveness, available to borrowers working full-time for qualifying government or nonprofit employers, can accelerate that timeline to ten years of payments. However, recent changes to federal loan caps and IDR plan structures have shifted the calculus for some borrowers. The long-term savings from PSLF remain substantial for those who qualify, but the math is no longer as straightforward as it once was. Run the numbers for your specific loan balance and expected salary before committing to a plan. For a deeper look at when MBA debt makes sense, weigh the forgiveness value against total interest paid under each scenario.

Refinancing: The Trade-Off to Understand

Private refinancing can reduce your interest rate, particularly if your post-MBA salary and credit profile are strong. The cost is permanent: once you refinance federal vs private MBA loans into a single private product, you lose access to income-driven repayment, PSLF, and federal forbearance protections. Refinancing makes sense for borrowers who are certain they will not pursue public service forgiveness and who have stable income that removes any need for a federal safety net. For everyone else, the flexibility of federal protections is worth more than the rate savings in most scenarios.

MBA Financial Aid Checklist: Your Complete Action List

Bookmark or print this master checklist so no deadline slips through the cracks. Each item maps to a phase of the financial-aid timeline covered in this guide.

- 12–18 Months Before Enrollment

- Calculate your full cost of attendanceInclude tuition, fees, living expenses, and opportunity cost of forgone income.

- Research scholarship databases and school-specific awardsNote eligibility criteria, essay prompts, and recommendation requirements for each.

- Request employer tuition reimbursement policies and formsConfirm annual caps, grade requirements, and any post-graduation service commitments.

- Draft a personal funding planEstimate the gap between savings, scholarships, employer support, and total cost.

- 9–12 Months Before Enrollment

- Prepare scholarship essays and secure recommendersGive recommenders at least six weeks and share your career narrative.

- Submit scholarship applications by each program's priority deadlineMany merit awards are decided with the earliest admissions rounds.

- Take or retake the GMAT or GRE if a higher score could unlock additional aidSome schools tie scholarship tiers directly to test-score bands.

- After Admission

- Compare award letters side by sideNormalize each offer by calculating net cost of attendance after grants, scholarships, and employer funding.

- Negotiate or appeal scholarship offers with admissions and financial-aid officesPresent competing offers, updated test scores, or new professional achievements as leverage.

- Before the Deposit Deadline

- Confirm deposit requirements and deferral policiesUnderstand whether your scholarship transfers if you defer enrollment.

- Coordinate deposit timing with employer approval cyclesSome companies require pre-approval before committing tuition funds.

- Before Enrollment

- File the FAFSA by your school's priority deadlineThe federal application opens on October 1 each year; submit as early as possible.

- Complete the CSS Profile if your program requires itCheck each school's specific deadline, many fall well before classes start.

- Accept federal Direct Unsubsidized Loans before considering private optionsFederal loans offer income-driven repayment and forgiveness protections that private loans typically do not.

- Compare private loan offers from at least three lendersEvaluate fixed versus variable rates, origination fees, and deferment options.

- During the Program

- File renewal scholarship applications each yearSome awards require a separate application or GPA verification for continued funding.

- Submit employer reimbursement claims each semesterTrack receipts, grades, and reimbursement deadlines to avoid forfeiting benefits.

- Borrow only what you need each termRevisit your budget before accepting the full loan amount offered.

- Before Graduation and Beyond

- Complete federal exit counselingRequired for all federal loan borrowers and available through your loan servicer's portal.

- Enroll in the repayment plan that fits your post-MBA income trajectoryEvaluate standard, graduated, and income-driven options before payments begin.

- Investigate employer loan-repayment assistance and Public Service Loan Forgiveness eligibilityApply early, some employer programs cap participation or operate on a first-come basis.

Frequently Asked Questions About MBA Financial Aid

Below are answers to the most common questions prospective MBA students ask about funding timelines, scholarships, federal aid, and employer support. Each answer is designed to help you take action at the right moment in your MBA financial aid timeline.