What you’ll learn in this article…

- A full-time MBA can cost $150,000 to $350,000 when you include living expenses, opportunity cost, and loan interest.

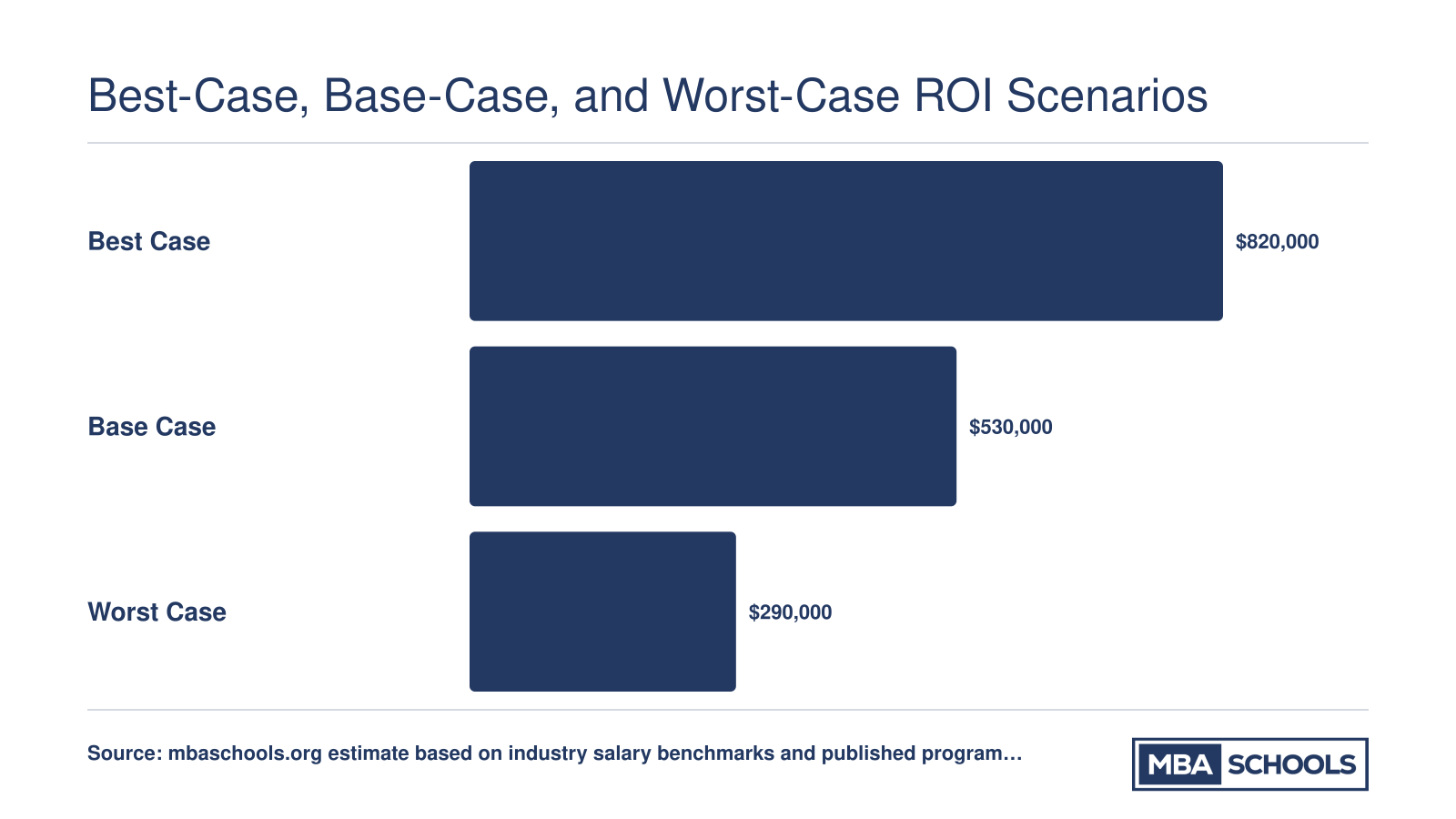

- Scenario analysis shows a 10-year ROI swing from roughly negative $20,000 in worst cases to over $800,000 in best cases.

- Post-MBA salaries vary by more than $60,000 for the same role depending on metro area, per BLS wage data.

- Non-financial returns like alumni networks, leadership development, and brand equity often drive career value long after graduation.

MBA ROI calculators produce reliable answers only when fed reliable inputs, and most applicants start with incomplete data. Tuition figures posted on program websites rarely include health insurance, international module fees, or the opportunity cost of two years without a paycheck. According to Lawrence Mur'ray, Executive Director of Admissions and Financial Aid at Tuck School of Business at Dartmouth, writing in June 2026, the right questions matter more than the calculator itself: you need to account for cost structure, career trajectory, financing mechanics, downside scenarios, and intangible returns that resist easy quantification.1

This article organizes those questions into seven categories. Cost questions surface the hidden line items most calculators omit. Opportunity cost questions force you to measure what you give up. Salary projection questions help you model realistic post-MBA compensation. Financing questions clarify the true burden of debt. Risk questions stress-test your assumptions. Non-financial questions capture network effects, brand equity, and developmental experiences. Comparison questions provide the framework for calculating MBA ROI across multiple schools on a level playing field.

Cost Questions: Tuition, Fees, and the Hidden Expenses Most Calculators MISs

What is the true all-in cost of an MBA program, and why does that number matter more than published tuition figures?

Most MBA applicants begin their ROI calculations with the wrong number. They anchor on the tuition figure prominently displayed on a program's website, run that through a calculator, and arrive at conclusions built on incomplete data. The reality is that most applicants undercount their total MBA costs by 15 to 25 percent, a gap that can translate into tens of thousands of dollars and fundamentally distort any return calculation.

The Full Cost Stack Beyond Tuition

Tuition is only the starting line. A comprehensive cost assessment must account for every mandatory expense you will encounter across two years:

- Mandatory fees: Activity fees, technology fees, and administrative charges can add $2,000 to $5,000 annually depending on the school.

- Health insurance: If you leave employer-sponsored coverage, expect $3,000 to $6,000 per year for school-sponsored plans.

- Course materials and software: Case studies, textbooks, and required software subscriptions often total $1,500 to $3,000 annually.

- Living expenses: Housing, food, transportation, and personal costs vary dramatically by location and lifestyle.

Before you input any number into an ROI model, ensure you are capturing this complete cost stack rather than just the tuition headline. Affordable MBA programs often compete on net cost rather than sticker price, making this distinction especially consequential.

Geography Changes Everything

Where your program is located fundamentally alters your cost equation. A student attending a program in Manhattan will face housing costs that can exceed $30,000 annually for a modest apartment, while a comparable living situation near a program in Durham, North Carolina might cost $14,000 to $18,000. These differences compound over two years.

For international students, geography introduces additional layers. Visa application fees, SEVIS charges, mandatory travel for consular interviews, and the cost of maintaining legal status add thousands to the baseline. Domestic students relocating across the country must budget for moving expenses, security deposits, and the friction costs of establishing a new household.

Sticker Price Versus Net Price

The most consequential number for your ROI calculation is not the sticker price but the net price after MBA scholarships, fellowships, and grants. A program with $160,000 in total published costs but $60,000 in merit aid presents a fundamentally different investment proposition than one with $140,000 in costs and no aid. Many ROI calculators prompt you for tuition without specifying whether to enter gross or net figures, leading to systematically inflated cost projections.

Before finalizing any calculation, confirm your expected aid package and use the net cost figure exclusively.

Year-Over-Year Cost Changes

Ask directly: Are there costs in Year 2 that differ from Year 1? Some programs increase tuition annually by 3 to 5 percent. Others front-load fellowship support in the first year, reducing aid in the second. A few programs have locked tuition policies that guarantee the same rate across both years.

The question to pose to any admissions or financial aid office is straightforward: What is the total all-in cost for students who complete the full program, not just the published first-year tuition? Schools with transparent financial aid practices make this calculation easier, while programs that obscure total costs warrant extra scrutiny before you commit any figures to your MBA ROI calculator.

The Full Cost of an MBA at a Glance

Most MBA ROI calculators ask you to enter a single tuition figure, but the true price tag extends well beyond what the bursar's office charges. The ranges below reflect realistic two-year totals across a spectrum of full-time programs, from regional state schools to top-ranked private institutions. Use them to pressure-test whichever calculator you choose.

Opportunity Cost Questions: What You Give up During Your MBA

Eighty-one percent represents the average salary increase for full-time MBA graduates compared to their pre-program earnings, according to historical GMAC data. That figure sounds impressive until you factor in what you sacrifice to earn it. Opportunity cost, the income and career momentum you forfeit while enrolled, often equals or exceeds tuition itself. Asking precise questions about these trade-offs separates realistic ROI projections from wishful thinking.

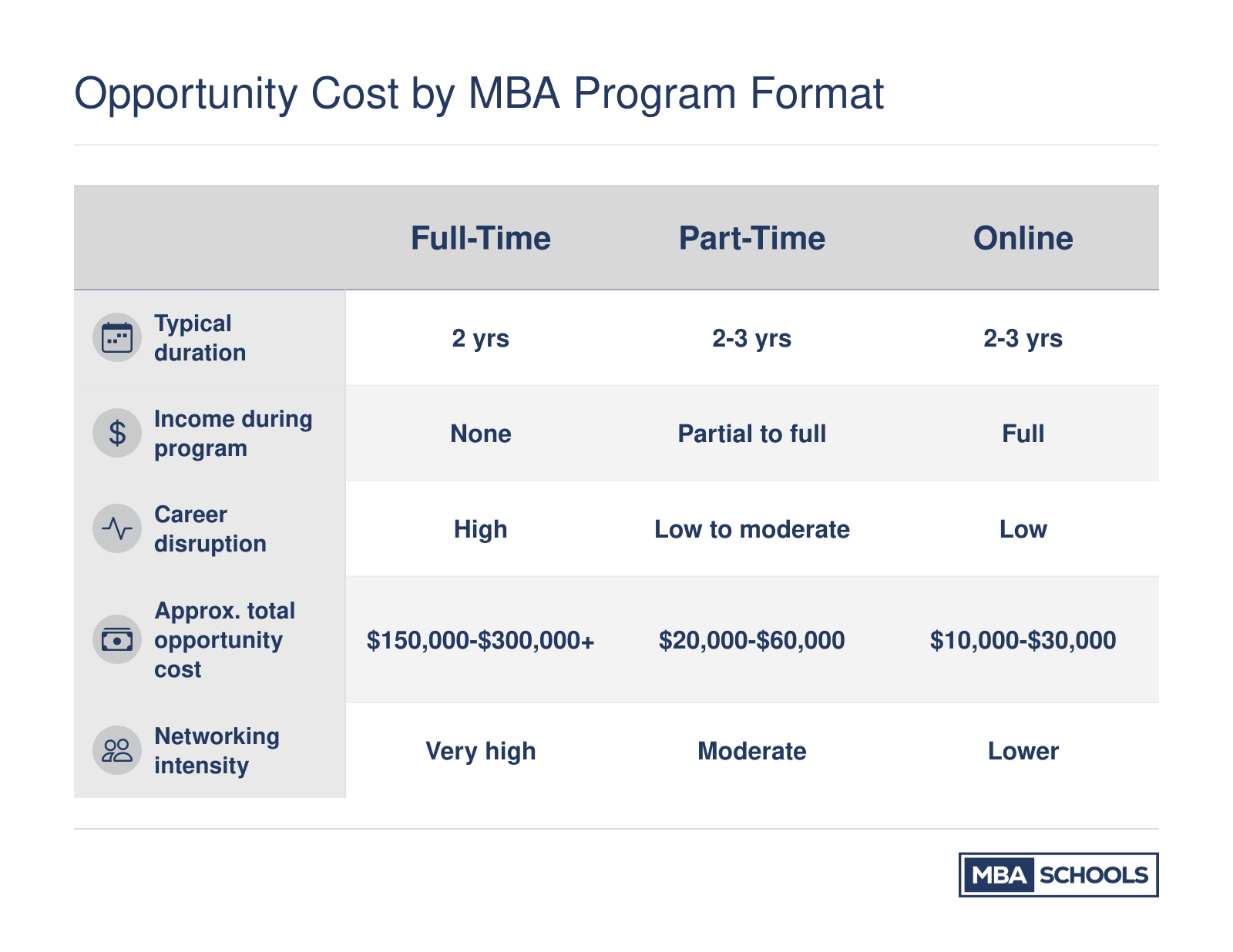

Quantifying Foregone Earnings by Program Format

The salary you give up during your MBA depends heavily on the format you choose. A full-time program typically removes you from the workforce for two years. If your pre-MBA salary sits at $85,000, that represents $170,000 in lost wages before accounting for bonuses, 401(k) matches, or equity vesting. Part-time and executive MBA students keep earning while they study, but they sacrifice evenings, weekends, and sometimes the mental bandwidth that could fuel promotions or side ventures.

Online MBA programs present a middle ground. While employer perception scores for online credentials hover around 60 percent favorable, what employers think about online MBA credentials is only part of the calculation: these programs let you maintain full income throughout. The trade-off becomes time rather than money: can you sustain 15 to 20 hours of weekly coursework alongside a demanding job for two or three years?

Questions to Ask About Your Specific Situation

Before running any calculation, gather answers to these foundational questions:

- What is my current total compensation? Include base salary, bonuses, stock options, retirement contributions, and health benefits. Many candidates undercount by focusing only on base pay.

- What raises or promotions would I likely receive if I stayed? Consult your company's typical advancement timeline and industry salary benchmarks from the Bureau of Labor Statistics.

- How long will my program take? Accelerated one-year MBAs cut foregone earnings in half but compress networking and recruiting timelines.

- Will my employer contribute tuition or maintain my salary? Some companies sponsor executive or part-time students, dramatically reducing opportunity cost.

Where to Find Reliable Comparison Data

The Graduate Management Admission Council publishes the Corporate Recruiters Survey annually, which includes salary premium data segmented by program format. Cross-reference these findings with employment reports published directly on top business school websites, where schools often disclose median salaries by prior industry and years of experience.

The Bureau of Labor Statistics provides occupation-level wage data by education attainment. While BLS figures do not isolate MBA holders specifically, you can compare median earnings for management analysts, financial managers, or marketing directors with bachelor's degrees versus master's degrees. This helps you estimate the incremental value your MBA might add within your target occupation.

Adjusting for Career Stage and Industry

Opportunity cost hits hardest for mid-career professionals with established salaries. A 28-year-old earning $70,000 sacrifices less in absolute terms than a 35-year-old earning $140,000, though the younger candidate may also have more career runway to recoup the investment. MBA career paths vary considerably: consulting and finance typically reward MBA credentials with immediate salary jumps, while tech and entrepreneurship offer more variable outcomes.

Ask yourself: does my target industry and role actually require an MBA, or would two years of aggressive networking and skill-building produce similar results? If the honest answer leans toward the latter, your opportunity cost extends beyond dollars to the alternative paths you could have pursued. Reviewing MBA ROI, salary, and career data side by side with your current trajectory can make that answer clearer.

Opportunity Cost by MBA Program Format

Opportunity cost is often the largest hidden expense in an MBA investment. The format you choose dramatically shapes how much income you forgo and how much career disruption you absorb. Use this comparison to frame the right questions before running any ROI calculation.

Salary and Career Projection Questions: Modeling Your Post-MBA Compensation

Projecting your post-MBA salary demands more than plugging a single number into a calculator. A defensible ROI model requires dissecting total compensation, accounting for career-switching versus advancement paths, and benchmarking against real-world salary distributions, not just optimistic averages.

Total Compensation: Beyond Base Salary

School-reported salary figures often spotlight base pay, but top MBA employers structure offers with multi-component packages. Your projection should model every element: signing bonus, annual performance bonus, stock or equity grants, and relocation allowances. For example, a consulting offer might include a $165,000 base, $30,000 signing bonus, and up to $40,000 in year-end bonus and stock. Excluding these from your model understates first-year earnings by 20%, 40%. Ask programs for detailed compensation reports that break out each component, not just the median base salary.

Career Switchers vs. Career Advancers: Different Trajectories

Your career-change status fundamentally alters the shape of your post-MBA earnings curve. Career advancers, those staying in their industry or function, often see an immediate salary jump, leveraging their existing experience for a premium. A financial analyst moving into investment banking may start at $175,000 total compensation, a 50% increase. However, their long-term ceiling may be bounded by industry norms they already know.

Career changers, transitioning from, say, education to marketing, frequently take a lateral or even lower base salary immediately post-MBA, as they reset to entry-level MBA roles. Their initial total comp might be $120,000, but the trajectory steepens after 3, 5 years as they climb new ladders. When modeling, differentiate the two paths: career advancers can input higher first-year earnings but moderate growth rates; career changers should model slower starts with higher long-term growth assumptions. A closer look at MBA career paths and salaries can help you calibrate realistic growth curves for each scenario.

Benchmarking Against National Salary Data

A reality check against government wage data guards against inflated expectations. According to the Bureau of Labor Statistics, Management Analysts earn a national median of $101,190 (25th percentile: $76,770; 75th percentile: $133,140). General and Operations Managers report a median of $102,950 (25th: $67,160; 75th: $164,130). Financial Managers, often a target for MBA graduates across careers, show a median of $161,700 (25th: $118,360; 75th: $214,210). These are broad averages, not top-tier MBA outcomes, but they anchor projections. If a school's reported median vastly exceeds the BLS 75th percentile for that role, scrutinize the placement statistics: are they concentrated in high-cost metros or a handful of exceptional students?

Median vs. Percentile: What's Your Real Likely Outcome?

MBA programs often tout average or top-percentile salaries, but your personal risk profile depends on the distribution. Ask explicitly: What do the 25th- and 75th-percentile graduates earn in my target industry? If you model the median outcome and still break even, the investment is sound. But if your break-even hinges on exceeding the 75th percentile, you're betting on outperformance. For career changers, examining the 25th-percentile figure is particularly important, as it reflects the early-career lag that can strain loan repayment.

The 3-to-5-Year Catch-Up Window for Career Changers

Because career changers often start at lower post-MBA salaries, their ROI timeline diverges from career advancers. Advancers typically see immediate net-positive returns once forgone salary and tuition are recouped within 2, 4 years. Changers, by contrast, may not surpass their pre-MBA earning power (including forgone wages) until year 3, 5. For example, an operations manager earning $90,000 who transitions to brand management might start at $105,000 but only net a positive ROI after accounting for two years of missed raises and promotions in their original field. Build your model with a 5-year horizon and run both a career-advancer and career-changer scenario to pressure-test the timeline.

Post-MBA Salary Benchmarks by Occupation and Metro Area

National salary averages can be misleading when you are modeling your post-MBA compensation. Where you plan to work matters enormously. The table below draws from 2024 Occupational Employment and Wage Statistics published by the U.S. Bureau of Labor Statistics, covering two roles common among MBA graduates: Management Analysts and General and Operations Managers. Use these metro-level benchmarks to calibrate your own ROI projections against realistic, location-specific pay ranges rather than a single national figure.

| Occupation | Metro Area | Total Employment | 25th Percentile | Median Salary | 75th Percentile | Mean Salary |

|---|---|---|---|---|---|---|

| Management Analysts | Boston, Cambridge, Newton (MA, NH) | 26,530 | $101,230 | $134,580 | $169,320 | $149,850 |

| Management Analysts | San Francisco, Oakland, Fremont (CA) | 24,790 | $91,950 | $128,120 | $167,410 | $141,310 |

| Management Analysts | Washington, Arlington, Alexandria (DC, VA, MD, WV) | 68,900 | $99,100 | $125,820 | $149,500 | $131,060 |

| Management Analysts | Chicago, Naperville, Elgin (IL, IN) | 36,300 | $82,860 | $120,140 | $162,330 | $127,990 |

| Management Analysts | New York, Newark, Jersey City (NY, NJ) | 63,220 | $84,660 | $110,950 | $162,220 | $129,500 |

| Management Analysts | Los Angeles, Long Beach, Anaheim (CA) | 39,750 | $79,750 | $107,470 | $164,440 | $126,340 |

| Management Analysts | Miami, Fort Lauderdale, West Palm Beach (FL) | 21,480 | $70,620 | $97,700 | $128,160 | $107,670 |

| Management Analysts | Minneapolis, St. Paul, Bloomington (MN, WI) | 18,030 | $77,010 | $97,390 | $127,750 | $113,610 |

| Management Analysts | Sacramento, Roseville, Folsom (CA) | 25,050 | $68,200 | $82,180 | $91,370 | $86,510 |

| General and Operations Managers | Washington, Arlington, Alexandria (DC, VA, MD, WV) | 108,510 | $96,550 | $151,420 | $194,190 | $160,690 |

| General and Operations Managers | New York, Newark, Jersey City (NY, NJ) | 187,400 | $96,790 | $149,260 | $221,830 | $187,140 |

| General and Operations Managers | Boston, Cambridge, Newton (MA, NH) | 76,980 | $83,970 | $129,850 | $208,400 | $163,750 |

| General and Operations Managers | Los Angeles, Long Beach, Anaheim (CA) | 102,370 | $85,150 | $127,610 | $207,050 | $168,990 |

| General and Operations Managers | Dallas, Fort Worth, Arlington (TX) | 132,030 | $64,170 | $108,690 | $172,060 | $141,400 |

| General and Operations Managers | Atlanta, Sandy Springs, Roswell (GA) | 68,560 | $70,400 | $105,760 | $168,120 | $136,260 |

| General and Operations Managers | Chicago, Naperville, Elgin (IL, IN) | 121,110 | $72,700 | $105,310 | $173,630 | $142,650 |

| General and Operations Managers | Houston, Pasadena, The Woodlands (TX) | 105,830 | $64,210 | $108,090 | $172,610 | $138,980 |

| General and Operations Managers | Miami, Fort Lauderdale, West Palm Beach (FL) | 74,070 | $69,130 | $104,060 | $163,820 | $135,050 |

| General and Operations Managers | Phoenix, Mesa, Chandler (AZ) | 73,000 | $62,780 | $94,130 | $141,450 | $122,850 |

Debt and Financing Questions: Loans, Repayment Timelines, and Tax Impact

Financing is where many MBA ROI calculations go wrong. Most applicants estimate tuition, subtract scholarships, and call it a day. But the true cost of borrowing depends on the loan type you use, how long you take to repay, and whether your employer or the tax code offsets part of the burden. Before you plug numbers into any calculator, work through the questions below.

What Will Your Actual Loan Balance Be at Graduation?

Start with total borrowing, not just annual tuition. federal student loans for MBA students in the Direct Unsubsidized program carry a 7.94 percent interest rate for the 2025-2026 disbursement year, and interest begins accruing immediately, even while you are in school.1 Over a two-year program, capitalized interest can add thousands of dollars to your principal before you make a single payment. If you need to borrow beyond the $20,500 annual Direct Unsubsidized limit,2 you may turn to Grad PLUS loans at 8.94 percent,1 though new borrowers should note that Grad PLUS loans are being eliminated for first-time borrowers starting July 1, 2026.2 Continuing students retain access for up to three additional academic years, but incoming classes will need to rely on Direct Unsubsidized loans and private lenders.2 Model your balance at graduation, not your balance at enrollment.

Which Repayment Plan Should You Model?

Your repayment strategy shapes both monthly cash flow and total interest paid over the life of the loan. Key options include:

- Standard 10-year repayment: Fixed monthly payments that minimize total interest but produce the highest monthly obligation.

- SAVE plan: Payments set at 10 percent of discretionary income, with unpaid interest that does not capitalize onto your principal, and forgiveness after 25 years.

- IBR (new borrower version): Also 10 percent of discretionary income, with forgiveness after 20 years, but requires a partial financial hardship to qualify.

- PAYE: Similar 10 percent payment cap with 20-year forgiveness, though this plan is now closed to most new borrowers.

If you plan to work for a government agency or 501(c)(3) nonprofit after graduation, Public Service Loan Forgiveness may apply after 120 qualifying monthly payments on any income-driven plan or the standard plan. That timeline, roughly ten years, can dramatically change the math for MBA graduates who pursue nonprofit management, public health administration, or government consulting.

When comparing plans, calculate both total interest paid and the monthly payment in your first post-MBA year. A lower monthly payment frees cash flow for investing or a down payment, but it may cost tens of thousands more over time.

Does Employer Sponsorship Change the Equation?

If your employer covers 50 to 100 percent of tuition, the cost side of your ROI calculation changes dramatically, but you need to read the fine print. employer sponsorship for MBA packages often include service commitments requiring two to four years of continued employment after degree completion. Ask about clawback clauses, which can require you to repay a prorated share of the benefit if you leave early. A generous sponsorship package that locks you into a below-market role for three years may actually reduce your ROI compared to self-funding and switching employers immediately after graduation.

What Tax Benefits Apply?

Three provisions are worth modeling:

- Student loan interest deduction: You can deduct up to $2,500 per year in loan interest paid, though the deduction phases out at higher income levels, which many post-MBA earners will approach quickly.

- Employer tuition reimbursement: The first $5,250 per year is excluded from taxable income. Amounts above that threshold are treated as taxable compensation, so a $30,000 annual reimbursement means roughly $24,750 will show up on your W-2.

- Scholarship tax treatment: Scholarships applied to tuition and required fees are generally tax-free, but amounts covering living expenses or stipends are taxable income.

Incorporating these details into your model will not make or break your decision, but ignoring them can skew your projected net cost by several thousand dollars per year, enough to tip the scales when comparing two programs with similar sticker prices.

Risk and Scenario Analysis Questions: Stress-Testing Your MBA ROI

Every MBA ROI calculation rests on assumptions. The smarter move is to test what happens when those assumptions are wrong. Scenario analysis does exactly that: it forces you to model your investment under conditions that are less comfortable than your best guess.

Build a Three-Scenario Framework

For each major variable in your calculation, construct three outcomes: a best case, a base case, and a worst case. Run those combinations across salary, time-to-employment, loan interest rate, and total program cost. What you will discover is that the numbers are far more sensitive to some variables than others.

Post-MBA salary is usually the most powerful lever. A 10 percent shortfall in your expected starting compensation compounds painfully over a 20-year career, dwarfing the financial impact of a $10,000 overrun in tuition. That does not mean you should ignore tuition, but it does mean salary assumptions deserve the most scrutiny in your model. Reviewing MBA career paths and salary benchmarks by function and industry can sharpen those assumptions before you build your model.

Account for Time-to-Employment Risk

Most ROI calculators assume you walk out of graduation into a signed offer. That scenario happens, but not universally. Ask yourself: what does my calculation look like if it takes six months rather than three to land a role?

The answer involves more than delayed income. It includes continued living expenses, potential loan interest accruing without offset, and the psychological cost of an extended search. Placement data from schools provides a useful probability anchor here. Among M7 programs in 2024, roughly 70 to 85 percent of graduates had offers at graduation, with 90 to 97 percent placing within three months.1 At T15 programs, those figures ran 60 to 80 percent at graduation and 88 to 95 percent within three months.2 T25 programs reported 50 to 75 percent at graduation and 85 to 92 percent within three months.3

Individual school results vary considerably within those ranges. MIT Sloan reported 100 percent placement within three months in 2024, while Wharton came in at 97 percent. Stanford GSB and Harvard placed closer to 89 and 86 percent respectively, partly reflecting a higher proportion of graduates pursuing entrepreneurial or non-traditional paths.4 Career switchers, as a group, tend to take longer than career advancers to secure offers, which matters when you are modeling your personal scenario rather than a program average.

Sensitivity Analysis in Plain Language

Sensitivity analysis simply means asking: if I change one variable by a fixed amount, how much does my ROI change? You do not need a spreadsheet formula to do this intuitively. Start with salary. Move your expected starting compensation down by 10 percent and recalculate your payback period. Then do the same for tuition (up 10 percent) and job search duration (extended by three months). The variable that produces the largest ROI swing is the one that deserves the most due diligence before you enroll. Understanding how much MBA debt is too much is an equally important input to that sensitivity check.

Factor In Macroeconomic and Sector Risk

Personal variables are only part of the picture. Graduating into a recession, an industry contraction, or a sector undergoing rapid automation introduces risks that no individual school can fully buffer against. A reasonable question to ask any program is: how did your graduates fare during the last major downturn, and which industries absorbed them?

Look at whether your target roles have durable demand. Functions tied to cost reduction, capital allocation, and operational efficiency have historically weathered downturns better than roles concentrated in discretionary spending or rapidly automating workflows. If your post-MBA plan depends heavily on a single industry, your scenario analysis should include a version of that industry shrinking.

Best-Case, Base-Case, and Worst-Case ROI Scenarios

Small shifts in your assumptions can produce enormous differences in long-term MBA returns. The scenarios below model a representative full-time MBA investment (total cost of roughly $200,000 including opportunity cost) over a 10-year horizon, varying post-MBA salary, time to first post-graduation paycheck, and whether annual raises compound modestly or aggressively. The spread between the best and worst case exceeds $500,000, underscoring why stress-testing your inputs is essential before committing.

Non-Financial ROI Questions: Network, Brand, and Personal Growth

The conversation around MBA value has shifted: today's applicants recognize that long-term career impact often outweighs the immediate salary bump. While spreadsheets can model base pay and signing bonuses, the real durability of an MBA comes from assets that resist quantification. A structured set of questions helps you evaluate these non-financial returns without resorting to hand-waving about 'priceless experiences.'

Evaluating Alumni Network Strength

- Network vitality: How active is the alumni base in your target industry and geography? Look beyond LinkedIn counts and ask for engagement data such as regional event attendance, mentorship program participation, or the share of alumni who volunteer as career contacts.

- Longevity of access: Lawrence Murray of Tuck emphasizes sustained career options as a core ROI pillar.1 A 10-year test is useful: will this network still open doors a decade after graduation, or is the school's ROI front-loaded into first-job placement? Many top programs report that over a third of alumni leverage their alumni network for mid-career transitions, but verifying this with the career office adds rigor.

Brand Equity and Career Switching

- Signaling power: Does the school's name carry weight in your target market? For career switchers applying to MBA programs, the brand often serves as a credential that substitutes for missing experience. If you already have an established track record, the incremental signaling benefit may be smaller.

- Employer perceptions: Ask for the employer survey feedback the career office collects. Which firms recruit on campus primarily because of the school's reputation? How does that brand translate in different geographies, especially if you plan to work internationally?

The Compounding Returns of Leadership Development

An immersive MBA delivers developmental experiences that compound over a 20- to 30-year career, not just the first job. As Murray notes, Tuck's model integrates academics, reflection, coaching, and experiential learning to build executive presence and cross-functional fluency.2 When evaluating programs, probe these elements: - Transformational vs. incremental growth: Are there leadership skills or professional transformations you need that only a full-time, immersive environment can deliver? If executive education or on-the-job development could close the same gaps, the non-financial return may be less compelling. - Built-in developmental experiences: Look for structured opportunities like global consulting projects, board fellowships, or intensive leadership labs. These are often the settings where lasting self-awareness and influencing skills take root.

Lifestyle and Mobility ROI

Non-financial returns also include changes in how and where you live and work. Consider: - Geographic flexibility: Does the program open doors to cities or regions you could not access otherwise? Some MBAs serve as deliberate relocation platforms. - International exposure: A global alumni network and overseas project experience can accelerate an international career shift. - Partner and family impact: Many two-career households need to evaluate how the MBA affects a spouse's job prospects, social support, and overall quality of life during the program and beyond.

Asking the Hard Questions

Frame your evaluation with prompts that surface hidden value and hidden costs: - In 10 years, will the network from this program still be actively opening doors for you, or is the ROI concentrated in your first post-MBA placement? - What proof does the school offer that its leadership development results are durable? Do they track alumni career trajectories beyond the initial employment report? - Could the lifestyle changes the MBA enables actually be achieved through a lateral move or professional certification at lower cost?

How to Compare MBA ROI Across Multiple Programs

Comparing ROI across MBA programs only works when every school is run through the exact same model. School-reported numbers are not interchangeable, and the most common applicant mistake is stacking Harvard's median total compensation against Kellogg's mean base salary and Tuck's reported figure that may or may not include sign-on bonuses. Normalize first, compare second.

Lock In One Time Horizon and One Discount Rate

Use a 10-year net present value (NPV) calculation for every program on your list. Ten years is long enough to capture promotion cycles and bonus growth, short enough that your assumptions are not pure fiction. Pick one discount rate and apply it to all schools.

The discount rate represents what your money could earn elsewhere. If you invested your tuition in a diversified portfolio instead of spending it, you might earn 3-5% above inflation over a decade. A 3% real rate is conservative, 5% is more aggressive. The higher the rate, the less your future post-MBA salary gains are worth in today's dollars. For most applicants who are not finance professionals, a 4% real discount rate is a reasonable default. Whatever you pick, use the same rate across every school.

Normalize Compensation Data Before You Compare

Employment reports vary in methodology. Some schools report medians, others report means. Some include sign-on bonuses and stock, others report base only. Some exclude graduates who did not respond or who self-funded into entrepreneurship. Before comparing, rebuild each school's number using the same components: base salary plus expected sign-on plus expected year-end bonus, using medians wherever available. A detailed look at MBA career paths and salaries by function can help you pressure-test whether a school's reported figures align with what graduates in your target role are actually earning.

Build a One-Page Comparison Spreadsheet

Create a simple grid with one column per finalist school (limit yourself to two or three) and standardized rows:

- Total program cost: Tuition, fees, and living expenses across the full program

- Opportunity cost: Foregone salary and benefits during enrollment

- Scholarship or fellowship amount: Subtracted from total cost

- Estimated debt at graduation: What you will actually owe

- Expected Year 1 total compensation: Normalized across schools

- Expected Year 5 total compensation: Apply a consistent growth rate

- Expected Year 10 total compensation: Same growth assumption everywhere

- 10-year NPV: The bottom-line comparison number

When all three finalists are modeled identically, the spreadsheet does the arguing for you. The school with the highest NPV is not automatically the right choice, but you now have a defensible financial baseline to weigh against fit, location, and the non-financial factors covered earlier. If you want a framework for deciding how much debt each NPV scenario can justify, MBA student loan repayment considerations are worth building into your model before you finalize a program choice.

Common Questions About Calculating MBA ROI

Calculating MBA ROI involves more than plugging tuition and salary figures into a formula. The questions below address the most common sticking points professionals encounter when trying to model whether a program is worth the investment, drawing on the frameworks covered throughout this guide.

Related Articles

The gap between a confident MBA investment and a regretted one is not the sophistication of your calculator. It is the quality of the questions you feed into it. As the frameworks above illustrate, small assumption shifts in salary growth, loan terms, or opportunity cost can swing your 10-year ROI by hundreds of thousands of dollars in either direction.

Build a comparison spreadsheet using the standardized inputs outlined in this guide: all-in cost, format-specific opportunity cost, location-adjusted salary benchmarks, and realistic repayment timelines. Then stress-test every program through the best-case, base-case, and worst-case scenarios before making a commitment. If you want to put these principles into practice immediately, how to choose the right MBA program is a natural next step once your financial model is in hand. Most importantly, remember the long view. As Lawrence Murray of Tuck's admissions team has noted, MBA ROI is a 20-year story, not a two-year payback equation.1 The network, the brand equity, and the personal growth compound long after the last loan payment clears.