What you’ll learn in this article…

- Every MBA student at an accredited school is eligible for federal loans through the FAFSA, regardless of income.

- Always exhaust Direct Unsubsidized Loans before borrowing Grad PLUS Loans to minimize interest costs.

- File your FAFSA as early as possible since school priority deadlines, not the federal deadline, determine your aid.

- Layer scholarships, assistantships, and employer reimbursement with federal loans to shrink your total borrowing gap.

More than 70 percent of MBA students borrow federal loans to finance their degrees, yet a surprising number of applicants never file the FAFSA because they assume a six-figure salary disqualifies them. It does not. Every graduate student enrolled at least half-time at an accredited mba programs institution is eligible for federal Direct Unsubsidized and Grad PLUS loans through the FAFSA, regardless of income or assets.

The real cost of skipping the form is not just lost loan access. Many business schools require a completed FAFSA before releasing institutional scholarships, fellowships, or need-based grants. Filing early, understanding the difference between loan types, and knowing when the CSS Profile applies can collectively save tens of thousands of dollars over the life of your MBA debt. The step-by-step guidance below covers eligibility rules, filing instructions, federal loan comparisons, key deadlines, and strategies for layering mba program scholarships with employer benefits to minimize what you borrow.

Can MBA Students Get FAFSA? Eligibility Explained

Yes, MBA students can and should file the FAFSA. Every graduate student enrolled at an accredited mba programs institution is eligible for federal student loans through this single application. Even if you suspect your income or savings will disqualify you from need-based aid, filing is still a smart move because it unlocks loan programs and, at many schools, serves as a gateway to institutional scholarships.

Graduate Students Are Automatically Independent

One of the most common points of confusion for prospective MBA students is whether parental income affects eligibility. Here is the short answer: it does not, at least not for federal aid purposes. The FAFSA classifies all graduate and professional students as independent, regardless of age, living situation, or family wealth. Your parents' income and assets are never collected on the graduate FAFSA form, and they play no role in determining your federal loan eligibility.

That said, some MBA programs use supplemental forms (such as the CSS Profile) to evaluate candidates for institutional need-based scholarships. Those forms may ask about parental finances. But for the FAFSA itself, only your own income, your spouse's income if applicable, and your own assets matter.

The Pell Grant Misconception

A persistent myth is that the FAFSA is primarily about Pell Grants. While Pell Grants are a critical resource for undergraduates, graduate students are not eligible for them. Filing the FAFSA as an MBA student instead opens the door to two federal loan programs:

- Direct Unsubsidized Loans: Available to all eligible graduate students up to a set annual limit, regardless of financial need.

- Grad PLUS Loans: Available to cover remaining cost of attendance after other aid, subject to a credit check rather than a need-based formula.

These two programs together can cover a substantial portion of MBA costs, and neither requires you to demonstrate financial need.

Basic Eligibility Checklist

Before you sit down to complete the FAFSA, confirm that you meet the following requirements:

- U.S. citizen or eligible noncitizen (permanent residents, certain refugees, and other qualifying statuses)

- Valid Social Security number

- Enrolled or accepted for enrollment at least half-time in an eligible, accredited MBA program

- No defaults on existing federal student loans and no outstanding overpayments on federal grants

- Registered with Selective Service, if required

- Maintaining satisfactory academic progress (a standard your school defines)

If any of these items give you pause, your MBA program's financial aid office can help clarify your status before you file.

Why Filing Matters Even If You Are High-Earning

Many working professionals assume that a six-figure salary puts them out of the running for financial aid. That assumption can be costly. Filing the FAFSA is a prerequisite for federal Direct Unsubsidized and Grad PLUS loans, which are available to borrowers at every income level. Beyond federal loans, a growing number of business schools require a FAFSA on file before they will consider you for merit scholarships, fellowships, or graduate assistantships. Exploring mba scholarships early in the process helps you identify which programs tie their awards to FAFSA completion. Some state grant programs for graduate students also use FAFSA data to determine awards. In short, skipping the FAFSA does not save you time; it limits your options.

How to Fill Out the FAFSA for an MBA Program: Step-By-Step

Filing the FAFSA as an MBA applicant is more straightforward than most working professionals expect. The form has been significantly streamlined in recent years, dropping from 108 questions to roughly 36. A direct data retrieval connection with the IRS, established through the FUTURE Act, now pulls your tax information automatically, reducing manual entry and the errors that come with it. Here is how to move through the process efficiently.

Create Your FSA ID and Start the Application

Before you can access the FAFSA, you need a Federal Student Aid (FSA) ID. Create one at studentaid.gov using your Social Security number, date of birth, and a personal email address. If you are married, your spouse will also need their own FSA ID to sign the form electronically. Once your credentials are active, log in and select the correct academic year for your MBA enrollment. Make sure you designate yourself as a graduate or professional student when prompted; selecting the wrong enrollment level is one of the most common mistakes and can affect the types of aid you are offered.

List Your MBA Programs Strategically

You can include up to 20 schools on a single FAFSA submission. Each program you list will receive your financial data and use it to build an aid package. At private institutions, the order of your school list does not influence award decisions. However, if you are applying to any public university in a state that distributes its own need-based graduate aid, the order may determine priority for those state funds. A practical approach: place any state school in your home state at the top of the list, then add remaining programs in whatever order you prefer. If cost is a primary concern, you may also want to explore affordable mba programs as part of your school selection process.

Understand Your Independent Status

All graduate students are automatically classified as independent on the FAFSA, regardless of age or living situation. This is a point of frequent confusion. Your parents' income and assets will not appear anywhere on the form and have no bearing on your eligibility. If you are married, however, your spouse's income and tax data are required and will factor into your financial profile. If you are single with no dependents, only your own earnings matter. This independent classification often works in favor of career changers who have been supporting themselves but whose parents had higher incomes during their undergraduate years.

Avoid the Most Common Filing Mistakes

Several errors trip up MBA applicants every cycle. Watch for these:

- Skipping the electronic signature: Both you and your spouse (if applicable) must sign the FAFSA electronically with your FSA IDs. An unsigned form will not be processed.

- Entering incorrect tax figures: With IRS direct data retrieval now built in, let the system populate your tax information rather than entering it by hand. Manual overrides introduce discrepancies that can trigger verification delays.

- Assuming high income disqualifies you: Even if your salary is well above the national median, filing the FAFSA unlocks access to federal Direct Unsubsidized Loans and Grad PLUS Loans, neither of which is need-based. Walking away from the form because you assume you will not qualify leaves money on the table.

- Missing the graduate student designation: Selecting "undergraduate" instead of "graduate/professional" changes which federal programs you are eligible for and can delay your aid package.

File Early for the Best Outcome

The FAFSA typically opens on October 1 for the following academic year. Filing as close to that date as possible gives you a meaningful advantage. Many business schools distribute their own institutional scholarships and grants using FAFSA data, and a significant share of that funding is awarded on a first-come, first-served basis. Submitting early also provides a longer runway to compare aid offers across programs, negotiate packages, and build a complete financing plan before your enrollment deposit is due. Treat the October 1 opening as your target date, not a suggestion.

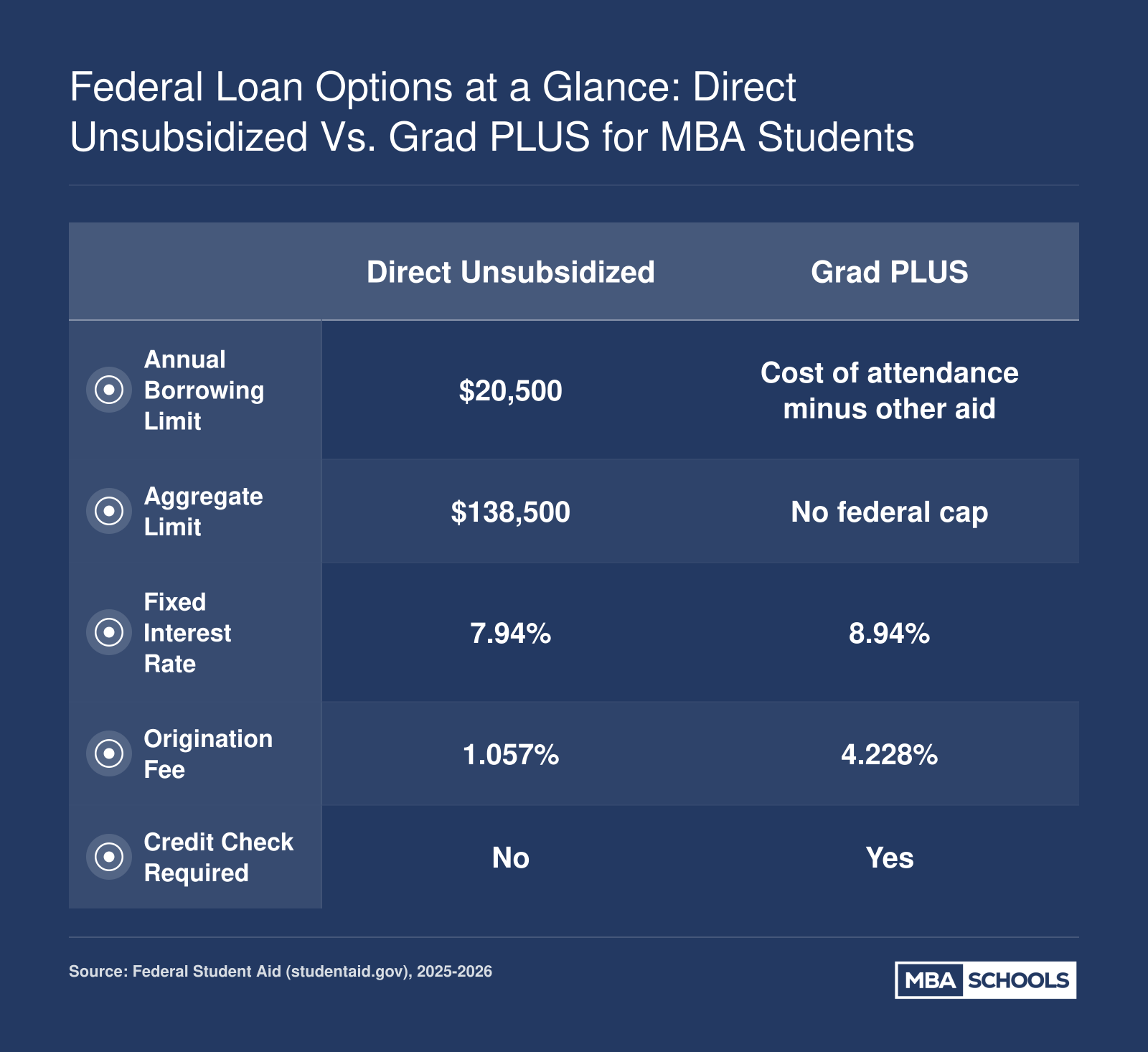

Federal Loan Options at a Glance: Direct Unsubsidized Vs. Grad PLUS for MBA Students

Before diving into the detailed breakdown below, use this side-by-side comparison to see how Direct Unsubsidized Loans and Grad PLUS Loans differ on the metrics that matter most. The strategic takeaway: always max out your Direct Unsubsidized borrowing first, since it carries a lower interest rate, a lower origination fee, and no credit check. Turn to Grad PLUS only after you have exhausted that first option. Figures shown are for the 2025-2026 award year and are subject to annual adjustment.

Federal Loan Types for MBA Students: Direct Unsubsidized Vs. Grad PLUS

Understanding the two federal loan programs available to MBA students is essential for building a smart borrowing strategy. Each carries different terms, limits, and costs, and the order in which you tap them can save you thousands of dollars over the life of your loans.

Direct Unsubsidized Loans: Your First Line of Borrowing

Direct Unsubsidized Loans should be every MBA student's starting point. Graduate students can borrow up to $20,500 per academic year, with an aggregate lifetime limit of $138,500 that includes any Direct Loans you took out as an undergraduate.

The word "unsubsidized" matters here. Unlike subsidized loans available to undergraduates, the federal government does not cover interest while you are enrolled. Interest begins accruing from the day funds are disbursed. For a two-year, full-time MBA, that means interest accumulates across roughly 24 months of coursework plus any grace period before repayment begins. If you borrow the maximum $20,500 each year, you will owe a meaningful amount of capitalized interest by the time you start making payments. Even so, Direct Unsubsidized Loans carry the lowest interest rate and origination fee of any federal graduate loan product, which is why exhausting this option first is so important.

Grad PLUS Loans: Filling the Remaining Gap

Grad PLUS Loans cover the difference between your total cost of attendance and any other financial aid you receive, including your Direct Unsubsidized Loan. There is no annual dollar cap beyond that cost-of-attendance ceiling, which means there is effectively no hard limit on total federal borrowing for an MBA.

A common misconception is that Grad PLUS Loans require a strong credit score. They do not. The federal government checks for "adverse credit history," a specific standard that looks for serious delinquencies, defaults, bankruptcies, or other negative events on your record within the past few years. Having a modest credit score alone will not disqualify you.

The tradeoff is cost. Grad PLUS Loans carry a higher fixed interest rate and a higher origination fee than Direct Unsubsidized Loans. For the current loan year, the rate differential between the two programs is meaningful enough that borrowing an extra dollar through Grad PLUS rather than Direct Unsubsidized adds noticeably to your total repayment. Over a 10-year standard repayment plan, that gap compounds.

The Right Borrowing Order for a High-Cost MBA

Consider a program with a total two-year cost of $120,000 or more. Before turning to loans, explore mba program scholarships and other grant-based aid that does not need to be repaid. A strategic borrower would then take $20,500 per year in Direct Unsubsidized Loans (totaling $41,000) at the lower rate, then cover the remaining balance through Grad PLUS Loans at the higher rate. This sequencing minimizes the share of your debt that carries the steeper interest charge. If you are weighing whether the overall investment makes sense for your career goals, it helps to understand is an mba worth it in 2026 before committing to significant loan balances.

Here is the priority order to follow:

- Direct Unsubsidized Loans: Borrow the full $20,500 per year first. Lower rate, lower origination fee.

- Grad PLUS Loans: Borrow only what you need beyond that amount. Higher rate, but still federal.

- Private loans (if necessary): Consider these only after exhausting federal options.

A Word on Private Loans

Some MBA students turn to private lenders to close a remaining funding gap or to chase a potentially lower variable rate. While private loans can sometimes offer competitive initial rates for borrowers with excellent credit, they come with significant trade-offs. Private loans do not qualify for federal income-driven repayment plans, Public Service Loan Forgiveness, or the borrower protections that accompany federal programs, such as deferment and forbearance options. For most MBA borrowers, private loans should be a last resort rather than a primary strategy.

Questions to Ask Yourself

FAFSA Deadlines and Timeline for MBA Applicants

The federal FAFSA deadline for the 2026, 2027 award year is June 30, 2027, but treating that date as your target is a serious mistake.1 The deadlines that actually determine how much aid you receive are set by individual business schools, and they arrive months earlier. Filing as soon as possible after the FAFSA opens on October 1, 2025, gives you the strongest position in every financial aid cycle you encounter.1

Why Institutional Priority Deadlines Matter More Than the Federal Deadline

Most top MBA programs distribute a significant share of their need-based and merit-based funding on a first-come, first-served basis within priority windows. Many schools set priority financial aid deadlines around early March (a common date across numerous institutions is March 2, 2026, for the 2026, 2027 cycle).1 Once that priority pool is allocated, late filers compete for whatever remains.

If you are applying in Round 1, which typically closes in September or October, you have the advantage of filing your FAFSA the same month the application opens. Round 2 applicants (January deadlines) can still hit most priority windows comfortably. Round 3 applicants, however, face real risk: by the time admissions decisions arrive in the spring, priority aid funds may already be committed. Delaying your FAFSA filing compounds that disadvantage.

State-Level Deadlines Worth Checking

State grant programs rarely extend to graduate students, but a few states do offer aid that MBA students can access. California, for example, sets its state aid deadline at March 2, 2026, for the 2026, 2027 cycle.2 Other states impose even earlier cutoffs in January or February. Even if the odds of receiving a state grant are low, a quick check with your state's higher education agency costs nothing and could surface money you would otherwise leave on the table.

A Recommended Timeline for MBA Applicants

Building a concrete schedule around these overlapping deadlines keeps you ahead of the curve:

- October (FAFSA opens): File your FAFSA as close to October 1 as possible using prior-year tax data, which is already available.1

- November to December: Submit the CSS Profile if your target schools require it. Programs like those at HBS, Stanford GSB, Wharton, and MIT Sloan use the CSS Profile for institutional aid decisions, so confirm each school's requirements early.

- January to March: Monitor your Student Aid Report for accuracy, correct any errors, and confirm that your FAFSA data has been received by every school on your list.

- April: Compare financial aid packages across programs side by side. Factor in mba program scholarships, assistantships, and loan terms rather than focusing on sticker price alone.

- May (or per school instructions): Accept your aid offer and submit your enrollment deposit by the school's stated deadline.

This timeline aligns your FAFSA submission with the earliest admissions rounds and ensures you never miss a priority funding window. We consistently advise candidates to treat October 1 as their personal deadline, not June 30. The earlier you file, the more options you preserve.

FAFSA Vs. CSS Profile: Which Forms Does Your MBA Program Require?

Most MBA applicants know they need to file the FAFSA, but many overlook a second form that can unlock significantly more institutional aid: the CSS Profile. Understanding which forms your target schools require, and how they differ, is essential to maximizing your financial aid package.

How the Two Forms Compare

The FAFSA and CSS Profile serve different purposes and collect different levels of financial detail. Here is a quick comparison across the dimensions that matter most for MBA applicants:

- Administrator: The FAFSA is a federal form managed by the U.S. Department of Education. The CSS Profile is administered by the College Board.

- Cost to file: The FAFSA is always free. The CSS Profile charges a fee per school (currently around $25 for the first school and $16 for each additional school), though fee waivers are available for lower-income applicants.

- Financial data collected: The FAFSA uses a simplified formula based on income, tax data, and limited asset information. The CSS Profile digs much deeper, asking about home equity, retirement account balances, non-custodial parent or spouse finances, medical expenses, and other assets the FAFSA ignores entirely.

- Aid it unlocks: The FAFSA determines eligibility for federal student loans (Direct Unsubsidized and Grad PLUS), federal work-study, and some state grants. The CSS Profile is used by individual schools to allocate their own institutional need-based grants and fellowships.

- Who requires it: Nearly every accredited MBA program in the U.S. requires the FAFSA. Only a subset of schools, typically those with large endowments and robust need-based aid budgets, also require the CSS Profile.

Because the CSS Profile captures a more complete picture of your finances, schools that use it can distribute institutional grants with greater precision. If your target program requires the CSS Profile, skipping it means leaving potential scholarship money on the table.

Which Top MBA Programs Require the CSS Profile?

For the 2026-2027 cycle, the majority of elite MBA programs require both the FAFSA and the CSS Profile. Several also ask for a supplemental institutional financial aid form on top of both.

Programs requiring the CSS Profile plus the FAFSA include Harvard Business School, Wharton, Chicago Booth, Northwestern Kellogg, MIT Sloan, NYU Stern, Duke Fuqua, Cornell Johnson, USC Marshall, CMU Tepper, Emory Goizueta, and Georgetown McDonough.

Stanford GSB, Columbia Business School, and Yale SOM go a step further: they require the FAFSA, the CSS Profile, and their own supplemental institutional form. These additional forms typically ask program-specific questions about your financial situation and expected resources.

Programs That Require FAFSA Only

Several highly ranked public university MBA programs require only the FAFSA for financial aid purposes. For 2026-2027, UC Berkeley Haas, Michigan Ross, UVA Darden, and UNC Kenan-Flagler fall into this category. At these schools, federal aid eligibility and merit-based scholarships are generally the primary financial aid pathways. If keeping costs low is a priority, you may also want to explore cheapest mba programs alongside these public options.

What This Means for Your Application Strategy

If you are applying to a mix of programs, check each school's financial aid page early to confirm its form requirements. Filing the FAFSA is non-negotiable for virtually every U.S. MBA program. If even one of your target schools requires the CSS Profile, budget extra time to gather the more detailed financial documentation it demands, including records related to home equity, investments, and spousal income.

Filing both forms promptly, well ahead of each school's priority deadline, positions you for the widest possible range of federal loans and institutional grants. The extra effort of completing the CSS Profile can directly translate into need-based fellowships that reduce your total borrowing.

Maximizing Financial Aid: Scholarships, Assistantships, and Employer Reimbursement

Federal loans through the FAFSA are only one piece of the MBA funding puzzle. The smartest applicants layer multiple sources of aid to minimize their total borrowing. Here is how to pursue every realistic avenue, from merit scholarships to employer benefits, and how each interacts with your financial aid package.

Merit-Based Scholarships: Common, Negotiable, and Worth Pursuing

Most top MBA programs award merit scholarships based on GMAT or GRE scores, undergraduate GPA, professional experience, and leadership potential. Earning a full-ride scholarship is exceptionally rare at elite programs, but partial merit awards ranging from 25 to 75 percent of tuition are far more common than many applicants realize. Many schools require a completed FAFSA as a prerequisite for any scholarship consideration, even for awards that are not need-based. Filing your FAFSA signals that you are serious about enrollment and opens doors you might otherwise miss. For a deeper look at finding and winning mba program scholarships, see our comprehensive guide.

One detail that surprises many candidates: merit scholarships are often negotiable. If you hold competing offers from peer-ranked programs, you can respectfully present that information to an admissions or financial aid office. Schools routinely adjust packages to attract strong candidates, so treating scholarship offers as a starting point rather than a final number can pay off significantly.

Need-Based Institutional Grants and the CSS Profile

Beyond merit awards, many MBA programs distribute need-based grants funded by their own endowments. These institutional grants typically rely on data from the CSS Profile rather than, or in addition to, the FAFSA. The CSS Profile captures a more detailed financial picture, including home equity and non-custodial parent assets, which schools use to calibrate awards. Filing both the FAFSA and the CSS Profile, where required, gives you the widest possible access to institutional aid. Check each target school's financial aid page to confirm which forms they require.

Graduate Assistantships and Teaching Positions

Some MBA programs, particularly part-time and less selective full-time programs, offer graduate assistantship (GA) or teaching assistantship (TA) positions. These roles typically provide a tuition waiver plus a modest stipend in exchange for research support, teaching duties, or administrative work. Because a tuition waiver reduces your cost of attendance dollar for dollar, it directly lowers the amount you need to borrow. If you are considering programs outside the most selective tier, ask admissions teams whether GA or TA positions are available to MBA students and how to apply.

Employer Tuition Reimbursement

If you plan to pursue an MBA while employed, check whether your company offers tuition reimbursement. Under IRS Section 127, employers can provide up to $5,250 per year in education assistance tax-free. Amounts above that threshold are treated as taxable income. Even partial reimbursement can meaningfully reduce your out-of-pocket costs over a two- or three-year program.

Coordinating employer benefits with your FAFSA filing is straightforward but important. Employer tuition assistance is considered a resource that reduces your cost of attendance, so your financial aid office will factor it in when assembling your award. Report any employer benefits to your school's financial aid office promptly to avoid unexpected adjustments later in the term.

Outside Scholarships: Know the Rules Before You Apply

Outside scholarships from professional organizations, community foundations, and diversity-focused groups can supplement your aid package. However, do not assume these awards simply stack on top of your existing institutional aid. Federal regulations require you to report outside scholarships to your financial aid office, and many schools will reduce your institutional grant or loan eligibility by the amount of the external award. Before investing time in outside scholarship applications, ask your program's financial aid office how they handle external awards. Some schools reduce loans first, preserving your grant money, while others reduce grants. Understanding this policy upfront helps you target applications where the net benefit is greatest.

- Merit scholarships: File your FAFSA even if you expect merit-only consideration, and negotiate offers when you hold competing admissions.

- Need-based grants: Submit the CSS Profile alongside the FAFSA at schools that require it to unlock the full range of institutional aid.

- Assistantships: Explore GA and TA roles, especially at part-time and mid-tier full-time programs, for tuition waivers that cut borrowing.

- Employer reimbursement: Claim up to $5,250 per year tax-free and report benefits to your financial aid office.

- Outside scholarships: Confirm your school's policy on how external awards interact with institutional aid before applying.

Financial Aid for Part-Time, Online, and International MBA Students

Not every MBA student follows a traditional full-time, on-campus path. Whether you are pursuing your degree part-time, through an online program, or as an international student, the rules for federal financial aid shift in important ways. Understanding these nuances before you enroll can prevent costly surprises down the road.

Part-Time MBA Students and the Half-Time Enrollment Threshold

Federal student aid, including Direct Unsubsidized Loans and Grad PLUS Loans, requires that you be enrolled at least half-time. For graduate programs, half-time enrollment is typically defined as 4.5 to 6 credit hours per semester, but the exact threshold varies by institution. If your course load dips below the minimum in a given term, you may lose eligibility for loan disbursement that semester, and your existing loans could enter their grace period prematurely.

Before registering for classes, confirm your school's half-time definition with the financial aid office. If you plan to take a lighter semester for work or personal reasons, ask how that decision will affect your aid package and repayment timeline.

Online MBA Programs and Title IV Eligibility

Students enrolled in accredited online MBA programs qualify for FAFSA on the same terms as their on-campus peers. The critical requirement is that the school itself must participate in the federal Title IV financial aid program. Most regionally accredited institutions do, but not all. Before you commit tuition dollars or sign an enrollment agreement, verify Title IV eligibility directly with the program or by searching the Department of Education's Federal School Code database. If you are weighing state-specific options, our breakdown of is fafsa available for online mba in Illinois offers a useful case study.

Executive MBA Considerations

Executive MBA programs often use non-traditional schedules: weekend residencies, intensive modules, or alternating terms. These structures can sometimes result in semesters where your enrollment does not meet the half-time threshold, temporarily interrupting your access to federal loans. Because EMBA tuition is frequently front-loaded or billed on a different cycle, even a brief gap in aid eligibility can create cash-flow challenges. If you are unsure whether the investment pencils out, our analysis of is an executive mba worth it 2025 2026 can help you run the numbers. Speak with the financial aid office early in the admissions process to map out exactly which terms qualify for loan disbursement and plan your personal financing accordingly.

International Students

Non-U.S. citizens who do not hold an eligible noncitizen status (such as a permanent resident card) cannot file the FAFSA. This excludes most international students from federal loans and need-based grants. Fortunately, several alternatives exist:

- Private student loans: Some U.S. lenders extend private loans to international students who have a creditworthy U.S. cosigner.

- Home-country financing: Government-sponsored loan programs and private lenders in your home country may offer education loans for study abroad.

- Institutional scholarships: Many MBA programs award merit-based scholarships that do not require FAFSA filing. Contact your admissions office to learn which awards are open to international applicants.

A Note on DACA Recipients

Students with Deferred Action for Childhood Arrivals (DACA) status are currently ineligible for federal student aid, including federal loans and Pell Grants. However, some states permit DACA recipients to access state-level financial aid, and individual institutions may offer their own mba scholarship opportunities. If you hold DACA status, research your state's policies and reach out to your target school's financial aid office to explore every available funding source.

Regardless of your enrollment format or citizenship status, the overarching advice remains the same: investigate your eligibility early, confirm requirements directly with your program, and layer multiple funding sources to close any remaining gap in your MBA financing plan.

Loan Repayment, Forgiveness, and Managing MBA Debt

Graduating with an MBA often means carrying a significant loan balance, but the repayment strategy you choose can save you tens of thousands of dollars over the life of your loans. Understanding your options before you graduate, not after, gives you the leverage to align your repayment plan with your mba career paths and salaries.

Standard Repayment Plans

Every federal borrower is automatically placed on the Standard Repayment Plan, which divides your balance into fixed monthly payments over 10 years. This approach minimizes total interest paid but produces the highest monthly obligation. Two alternatives ease the early burden:

- Graduated Plan: Payments start low and increase every two years over a 10-year term, which can help new MBA graduates whose salaries are expected to rise quickly.

- Extended Plan: Available to borrowers with more than $30,000 in outstanding Direct Loans, this stretches payments over up to 25 years with either fixed or graduated installments.

Both alternatives reduce short-term pressure but increase total interest cost over time.

Income-Driven Repayment: What MBA Graduates Need to Know Now

Income-driven repayment (IDR) plans cap monthly payments as a percentage of your discretionary income, with forgiveness of any remaining balance after a set period. The landscape shifted significantly in 2025 and 2026. The SAVE Plan, which had offered generous terms, was eliminated after enrollment was halted in February 2025.2 Legislation signed in July 2025 restructured the IDR framework effective July 1, 2026.1

For current borrowers, the key options are:

- Income-Based Repayment (new IBR): Payments set at 10% of discretionary income above 150% of the federal poverty level, with forgiveness after 20 years.3

- Original IBR: Payments at 15% of discretionary income, with forgiveness after 25 years. This version applies to borrowers who took out loans before certain cutoff dates.3

- Income-Contingent Repayment (ICR): An older plan that remains available but is generally less favorable for most MBA graduates.

Borrowers who first take out federal loans on or after July 1, 2026, will only have access to the Repayment Assistance Plan (RAP), a new program launching July 1, 2028.1 Until RAP becomes available, those new borrowers should plan around standard options.

All IDR plans require annual income recertification through the Federal Student Aid IDR application portal, and monthly payments are capped at the amount you would owe under the Standard 10-year plan.4 Any balance forgiven under IDR (outside of PSLF) may be treated as taxable income, so plan accordingly.

Public Service Loan Forgiveness for MBA Graduates

If you are pursuing a career in government, qualifying nonprofits, or social-impact organizations, Public Service Loan Forgiveness (PSLF) deserves serious attention. After making 120 qualifying monthly payments while employed at least 30 hours per week by an eligible employer, your remaining Direct Loan balance is forgiven, and that forgiveness is tax-free.4

PSLF works in tandem with IDR plans: enrolling in an income-driven plan keeps your monthly payments low during the 10-year qualifying period, maximizing the amount ultimately forgiven. For MBA graduates entering public-sector consulting, healthcare administration, or nonprofit management, this combination can eliminate a substantial portion of graduate school debt.

When Refinancing Makes Sense, and When It Does Not

MBA graduates who land high-paying private-sector roles may be tempted to refinance federal loans with a private lender to lock in a lower interest rate. This can be a smart move if your salary comfortably covers aggressive repayment and you have no interest in PSLF or IDR protections. Before refinancing, consider whether the long-term MBA career path you envision justifies giving up federal benefits.

Refinancing federal loans into private loans permanently forfeits access to income-driven repayment, PSLF, federal deferment, and forbearance options. If your career plans are even slightly uncertain, or if a future pivot to the public sector is on the table, keeping your federal loans intact preserves flexibility that no interest rate discount can replace.

A Simple Decision Framework

Think of your repayment strategy as a fork in the road:

- High-earning private-sector career with stable outlook: Prioritize aggressive repayment on the Standard Plan, or refinance if you can secure a meaningfully lower rate.

- Public-sector, nonprofit, or social-impact career: Enroll in an IDR plan immediately after graduation and pursue PSLF. Every qualifying payment counts.

- Uncertain career path or moderate initial salary: Stay on an IDR plan to keep payments manageable while preserving all federal protections. You can always switch to aggressive repayment later.

Grace Period and Timing

Direct Unsubsidized Loans provide a six-month grace period after you graduate or drop below half-time enrollment before repayment begins. Grad PLUS Loans technically enter repayment immediately, but you can request an in-school deferment and a post-enrollment grace period to align both loan types. Use that window to finalize your repayment strategy, set up autopay (which often earns a small interest rate reduction), and build an emergency fund before the first bill arrives.

Frequently Asked Questions About FAFSA for MBA Students

Below are the most common questions working professionals ask about filing the FAFSA for an MBA program. Each answer is designed to give you a clear, actionable takeaway so you can move forward with confidence.

Three actions matter most. First, file the FAFSA as soon as it opens each October; schools award institutional aid on a first-come, first-served basis, and waiting costs real money. Second, check whether your target programs also require the CSS Profile, since that form unlocks additional need-based grants at many top business schools. Third, always exhaust your Direct Unsubsidized Loan eligibility before turning to Grad PLUS borrowing, because the lower interest rate and fees save you thousands over the life of your loans.

Start today: visit studentaid.gov to create your FSA ID, then use your top-choice school's net price calculator to estimate your total funding gap. If you haven't yet explored how to get scholarships for mba programs, now is the time to layer those opportunities on top of federal aid. Thirty minutes now can reshape how you pay for your MBA and whether that investment delivers the return is an mba worth it 2026 analysis suggests it should.

Explore More

- AACSB-Accredited MBA

- Best GRE Prep Courses for MBA Applicants

- Best Military-Friendly MBA

- DISC Assessment for MBA Students & Graduates

- Executive MBA Courses

- Executive MBA vs. MBA

- Financial Aid for Minority MBA Students

- Financing Your MBA

- GMAT Study Guide

- GRE Guide for MBA Applicants

- How Much Does an Online MBA Cost? Full Breakdown

- How to Choose the Right MBA

- How to Pay for an MBA

- LGBTQ+ MBA

- MBA Accreditation Types

- MBA Admissions Consulting Guide

- MBA Admissions Rounds vs. Rolling Admissions

- MBA Capstone Projects

- MBA Careers Guide

- MBA Entrance Exams

- MBA FAQ

- MBA Glossary

- MBA Preparation Courses

- MBA Requirements

- MBA Resume Guide

- MBA Salary

- MBA Scholarships

- MBA Scholarships for AAPI Students

- MBA Scholarships for Black Students

- MBA Scholarships for Hispanic & Latino Students

- MBA Scholarships for International Students

- MBA Scholarships for Women

- MBA vs. Master's Degree

- Military MBA Financial Aid

- Mini-MBA

- Native American MBA Scholarships

- Undergraduate Prerequisites for MBA

- What Is a STEM MBA Program? Benefits, Schools & OPT Guide

- What Is an MBA? Your Complete Guide to MBA Degrees