What you’ll learn in this article…

- Federal Direct Unsubsidized and Grad PLUS loans offer fixed rates and borrower protections that private lenders cannot match.

- Roughly one in four MBA candidates receive some form of employer sponsorship or tuition reimbursement.

- Graduates who stack scholarships, savings, and assistantships can realistically complete an MBA with zero debt.

- Average MBA debt ranges from $60,000 to $120,000, but post-MBA salary premiums and loan forgiveness can offset the burden.

The average MBA graduate carries between $60,000 and $120,000 in student debt, a range wide enough to reshape your financial life for a decade or more. Yet a significant share of students, roughly one in four, graduate with little or no borrowing by stacking mba scholarships, employer sponsorship, and savings well before orientation day.

The tension is real: total cost of attendance at a top-20 program can exceed $200,000 over two years, while affordable mba programs may run a fraction of that. Where you land on that spectrum determines which funding levers matter most, from Direct Unsubsidized and Grad PLUS loans at current 2025-2026 federal rates to private lender options for domestic and international candidates. ROI varies just as sharply, with post-MBA salary premiums ranging from modest to transformative depending on industry, function, and pre-MBA experience. Whether the investment pencils out for you depends on choosing the right program at the right price, and that question of is an mba worth it deserves careful analysis before you sign any promissory note.

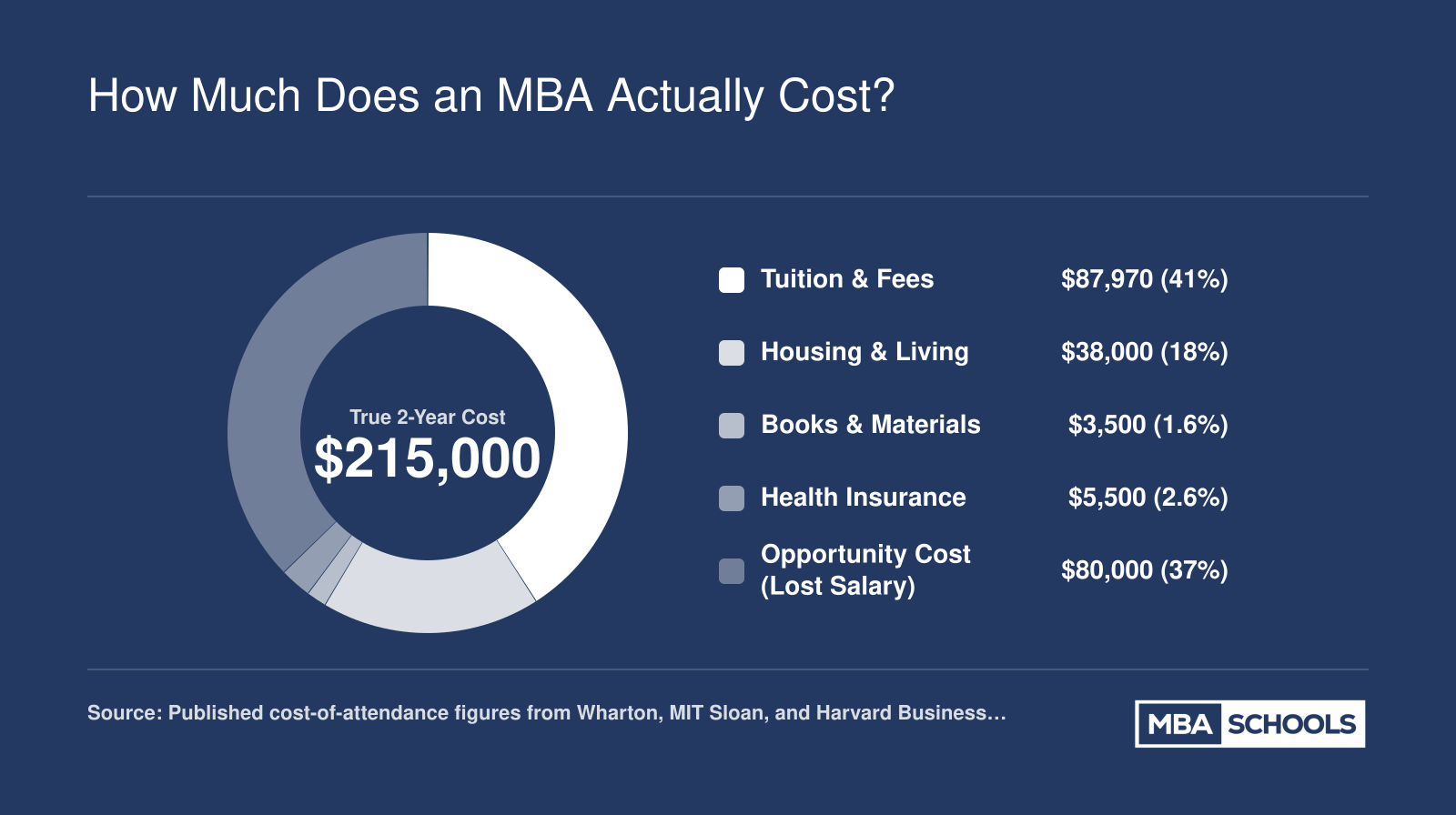

How Much Does an MBA Actually Cost?

The sticker price of an MBA extends well beyond tuition. When you add fees, living expenses, books, and the salary you forgo while studying, the true two-year price tag can be eye-opening. At elite M7 programs, total cost of attendance now exceeds $175,000, while top-25 schools typically run $150,000 to $200,000 for two years. Regional and state programs fall in the $60,000 to $120,000 range, and online MBAs can cost as little as $30,000 to $70,000 total. Keep in mind that sticker price rarely equals net price: merit-based scholarships significantly reduce what most students actually pay. And if you are wondering whether parental income disqualifies you from financial aid, know that MBA students are classified as independent on the FAFSA regardless of family earnings, so aid decisions are driven primarily by merit, not your parents' tax return.

Federal Student Loans for MBA Programs

Federal student loans are the foundation of most MBA financing plans, and for good reason. They offer fixed interest rates, flexible repayment options, and borrower protections that no private lender can match.1 Before you explore other funding sources, you should understand exactly what the federal government makes available to graduate students.

Direct Unsubsidized Loans

The Direct Unsubsidized Loan is the first federal loan most MBA students will use. For the 2025-2026 academic year, these loans carry a fixed interest rate of 6.39% and an origination fee of 1.057%.1 That origination fee is deducted before your funds are disbursed, so a $20,500 loan will put slightly less than that amount in your hands.

Graduate students can borrow up to $20,500 per year in Direct Unsubsidized Loans.2 If your two-year MBA program costs $50,000 or more per year, this loan alone will not cover the bill. The aggregate borrowing limit across all Direct Unsubsidized Loans (combining any undergraduate balance with your graduate borrowing) is capped, so you will want to check your remaining eligibility through your school's financial aid office.

One important note: "unsubsidized" means the government does not cover interest while you are enrolled. Interest begins accruing from the day your loan is disbursed, even if you defer payments until after graduation.

Grad PLUS Loans

When Direct Unsubsidized Loans fall short, Grad PLUS Loans fill the gap. These loans allow you to borrow up to the full cost of attendance minus any other financial aid you receive, making them the tool that covers the remainder of your tuition, fees, and living expenses.

For 2025-2026, Grad PLUS Loans carry a fixed interest rate of 8.94% and a significantly higher origination fee of 4.228%.1 On a $40,000 Grad PLUS Loan, that fee reduces your actual disbursement by roughly $1,691. Unlike Direct Unsubsidized Loans, Grad PLUS Loans also require a credit check; borrowers with adverse credit history may need to appeal or secure an endorser.

A critical development to be aware of: Grad PLUS Loans are being eliminated for new borrowers starting July 1, 2026, with only limited legacy provisions for existing borrowers.3 If you are planning to enroll in an MBA program in the near future, the timing of your enrollment could affect your access to this funding source.

Why Federal Loans Matter More Than the Rate Suggests

The interest rates on federal loans, especially Grad PLUS, may look higher than what some private lenders advertise. The real advantage lies elsewhere. Federal loans offer income-driven repayment plans that cap your monthly payment as a percentage of your discretionary income. They also provide pathways to loan forgiveness, including Public Service Loan Forgiveness for borrowers who work in qualifying nonprofit or government roles. Private lenders simply do not offer these protections.

Federal loans also come with deferment and forbearance options if you face financial hardship after graduation, giving you a safety net that private loans rarely match. If you are weighing the return on your degree investment, our analysis of whether an MBA is worth it in 2026 can help you put borrowing costs in perspective.

Eligibility: A Key Limitation

Only U.S. citizens and eligible noncitizens qualify for federal student loans. If you are an international student considering an MBA in the United States, federal loans will not be available to you, and you will need to explore alternative funding strategies.

To apply for federal loans, complete the FAFSA for MBA students as early as possible. Your MBA program's financial aid office will then determine your award package based on your cost of attendance and other aid you receive.

Private MBA Loans: Top Lenders Compared

When federal loans fall short of covering your full cost of attendance, private MBA loans can fill the gap. An important caveat applies, though: private loans do not offer income-driven repayment plans or federal loan forgiveness programs. Always maximize your federal borrowing first, then turn to private lenders only for the remaining balance. You may also want to explore mba scholarships before taking on additional debt.

Private loan rates, terms, and eligibility vary widely by lender. The comparison below covers several of the most prominent options for MBA borrowers, including lenders that serve international students.1

How Top Private MBA Lenders Compare

- SoFi: Fixed APR from 3.23% to 14.83%; variable APR from 4.64% to 15.86%. Repayment terms of 5, 7, 10, or 15 years. Cosigner is optional. Not available to international students. Offers in-school deferment options and is popular among MBA borrowers for its career services perks.

- Earnest: Fixed APR from 3.50% to 15.50%; variable APR from 4.99% to 15.50%. Repayment terms of 5, 7, 10, 12, or 15 years. Cosigner is optional. International student eligibility is limited. Earnest allows borrowers to customize monthly payments and skip one payment per year.

- Sallie Mae: Fixed APR from 2.89% to 14.99%; variable APR from 3.75% to 13.38%. Repayment terms of 5 to 15 years. Cosigner is optional. Not available to international students. Sallie Mae offers multiple in-school repayment choices, including full deferment, interest-only payments, or a flat $25 monthly payment while enrolled.

- College Ave: Fixed APR from 2.59% to 15.99%. Repayment terms of 5, 8, 10, or 15 years. Cosigner is required. Not available to international students.

- Ascent: Fixed APR from 2.69% to 16.61%. Repayment terms of 7, 10, 12, or 15 years. Cosigner is optional, and notably, Ascent does extend eligibility to international students even without a cosigner through its outcomes-based lending model.

- Prodigy Finance: Repayment terms of 7 to 20 years. No cosigner required. Designed specifically for international students attending top-ranked MBA programs. Prodigy Finance does not require a U.S. credit history or a U.S.-based cosigner, making it one of the few options built from the ground up for non-U.S. borrowers. Specific APR ranges vary by applicant profile.

- MPOWER Financing: Fixed APR from roughly 12% to 15%. Repayment terms of 10 or 15 years. No cosigner required. Open to international and DACA students at approved universities. MPOWER does not require a U.S. credit history, though its rate range tends to be higher than lenders that rely on traditional credit scoring.

All rates listed above are approximate and were current as of mid-2025.1 Your actual rate will depend on creditworthiness, loan amount, chosen term, and whether you apply with a cosigner.

In-School Deferment: What to Expect

Not all private lenders handle in-school payments the same way. Sallie Mae stands out for offering multiple paths during enrollment: you can defer all payments, make interest-only payments, or pay a small fixed amount. SoFi and Earnest also provide in-school deferment, though specific options may depend on the repayment term you select. Prodigy Finance and MPOWER Financing typically allow a grace period that extends six months after graduation before full repayment begins.

If cash flow during your MBA is tight, prioritize lenders with flexible in-school options. Even making small interest payments while enrolled can significantly reduce the total amount you owe after graduation.

Key Considerations Before You Borrow

- Compare total cost, not just APR: A lower rate with a longer term can cost more over the life of the loan. Run the numbers for each scenario.

- Cosigner release: Some lenders let you release a cosigner after a set number of on-time payments. Ask about this upfront if a family member is co-signing.

- International students have fewer choices: Prodigy Finance, MPOWER Financing, and Ascent are among the limited options that do not require U.S. citizenship or a U.S.-based cosigner. International students pursuing a STEM MBA program may find additional OPT-related benefits that make repayment more manageable.

- Rate type matters: Variable rates start lower but can rise over time. If you plan to repay quickly, a variable rate may save money. If your repayment horizon is 10 years or longer, locking in a fixed rate offers more predictability.

Before committing to any private loan, use rate-comparison tools and request quotes from multiple lenders. Even a fraction of a percentage point difference in APR can translate to thousands of dollars over a decade of repayment.

Questions to Ask Yourself

MBA Loans for International Students

International students face a fundamentally different financing landscape than their U.S. counterparts. Federal student loans, including Direct Unsubsidized Loans and Grad PLUS Loans, are available only to U.S. citizens and eligible noncitizens. That means international MBA candidates must piece together funding from private lenders, institutional aid, home-country financing, or some combination of all three.

The good news: a growing number of lenders and schools recognize the value international students bring, and the options have expanded considerably over the past decade. International candidates enrolled in STEM MBA programs may also benefit from extended OPT work authorization, which strengthens post-graduation earning potential and loan repayment capacity.

No-Cosigner Lenders for International MBA Students

Two lenders dominate the no-cosigner space for international students pursuing MBAs at highly ranked programs:

- Prodigy Finance: Lends to international students at over 100 top business schools worldwide. Loan amounts are based on projected future earning potential rather than current income or credit history. Interest rates are variable, and repayment typically begins six months after graduation.

- MPOWER Financing: Offers fixed-rate and variable-rate loans to international and DACA students at roughly 400 partner schools in the U.S. and Canada. No cosigner or collateral is required, and applicants are evaluated on academic merit and career trajectory.

Both lenders focus on students admitted to well-regarded programs, so eligibility is partly tied to the school you attend. If your target program is not on their approved lists, you will need to explore other routes.

The Cosigner Route

If you have a U.S. citizen or permanent resident willing to cosign, a wider set of private lenders opens up. Companies like SoFi, Earnest, and other major private student loan providers will consider international applicants with a creditworthy cosigner. This path often yields lower interest rates than no-cosigner options because the cosigner's credit profile reduces lender risk. Keep in mind that a cosigner assumes legal responsibility for repayment if you default, so this arrangement requires a high degree of trust on both sides.

Institutional Loan Programs

Several elite business schools run their own loan programs or maintain partnerships specifically for international admits. Harvard Business School, Wharton, Stanford GSB, and INSEAD all offer some form of school-based lending or financial aid that does not require U.S. citizenship. These programs vary widely in terms of loan limits, interest rates, and repayment terms.

Before you commit to any external lender, contact your school's financial aid office directly. Institutional options are sometimes more favorable than anything available on the private market, and they may not be prominently advertised. Students exploring affordable MBA programs should pay special attention to schools with generous institutional aid for international admits.

Watch for Exchange-Rate Risk

One factor that rarely appears in loan calculators but can significantly affect your total cost of borrowing: currency fluctuation. If you take out loans denominated in U.S. dollars but plan to work and earn in another currency after graduation, you are exposed to exchange-rate risk throughout your repayment period. A weakening home currency against the dollar means your monthly payments effectively increase, sometimes dramatically.

Strategies to manage this risk include:

- Prioritizing employment in the U.S. or another dollar-denominated economy for at least the early years of repayment.

- Borrowing partially in your home currency through domestic lenders if competitive rates are available.

- Building a repayment buffer into your financial plan to absorb currency swings.

International students should model repayment scenarios under different exchange-rate assumptions before signing any loan agreement. A loan that looks manageable at today's rates could become burdensome if your home currency depreciates 10 to 15 percent over a five-year repayment window.

MBA Scholarships, Fellowships, and Grants

Free money exists for MBA students, and securing it should be a top priority in your financing strategy. Scholarships, fellowships, and grants do not need to be repaid, making them the most valuable form of funding you can receive. Understanding the categories and knowing where to look can make the difference between graduating debt-free and carrying six figures in loans.

Types of MBA Scholarships

Most business school funding falls into four broad categories:

- Merit-based: The most common type at business schools, awarded for strong GMAT/GRE scores, undergraduate GPA, leadership experience, or professional accomplishments. Many schools automatically consider all admitted students.

- Need-based: Distributed according to financial circumstances. Schools typically require documentation of income, assets, and family obligations through a financial aid application.

- Diversity and identity-based: Designed to increase representation in MBA programs across gender, race, ethnicity, sexual orientation, and other dimensions of identity.

- Industry-specific: Targeted at students pursuing careers in sectors like healthcare, energy, social impact, or technology. These are often funded by corporate partners or alumni networks.

Can an MBA Be Fully Funded?

Yes, but full-tuition packages are rare and highly competitive. A handful of programs and external organizations offer full funding. The Consortium for Graduate Study in Management provides full-tuition fellowships at over 20 top business schools for students committed to diversity in business. Forte Fellows awards support women pursuing MBAs at dozens of partner schools. Management Leadership for Tomorrow (MLT) helps underrepresented minorities access scholarship-eligible programs. While not guaranteed full rides, these pipelines significantly increase your chances.

Major External MBA Scholarships Worth Pursuing

Several prestigious external awards can cover a substantial portion of your MBA costs. For a comprehensive list of opportunities, explore our guide to mba program scholarships.

- Forte Fellows: Awards for women at more than 50 partner business schools, often covering half-tuition or more.

- Consortium Fellowship: Full-tuition fellowships at member schools for students from underrepresented backgrounds.

- Reaching Out MBA (ROMBA) Fellowship: Supports LGBTQ+ students at top-ranked programs.

- National Black MBA Association Scholarships: Multiple awards for Black students in graduate business programs.

- Paul and Daisy Soros Fellowships for New Americans: Up to $90,000 for immigrants and children of immigrants pursuing graduate education, including MBAs.

Negotiate Your Scholarship Offer

One of the most overlooked strategies in financing an MBA is negotiation. Many schools will match or increase scholarship awards if you present a competing offer from a peer institution. This is not considered inappropriate; admissions offices expect it. When you receive multiple admits, share the competing financial package with each school's financial aid office and make a clear, respectful case for additional funding. Applicants who negotiate receive higher awards more often than you might expect.

Fellowships: More Than Just Tuition

Fellowships often go beyond covering tuition. Many include a living stipend, health insurance, or both. In return, fellows may be required to serve as teaching assistants, contribute to faculty research, or participate in program leadership. These commitments typically amount to 10 to 20 hours per week and provide valuable professional development alongside the financial benefit. If a fellowship is available in your area of interest, it can be one of the most holistic funding packages available to MBA students.

Start researching scholarships and fellowships early, ideally before you submit your applications. Deadlines vary, and some require separate essays or mba letters of recommendation beyond the standard admissions materials. Paying close attention to mba application deadlines ensures you never miss a scholarship window. A well-organized scholarship strategy can dramatically reduce your total cost of attendance.

According to GMAC's 2023 Prospective Students Survey, the majority of MBA candidates rely on a combination of personal savings, loans, and scholarships to fund their degrees, with employer sponsorship covering costs for roughly one in four students. For the most current funding breakdowns, visit gmac.com/research or check your target program's financial aid page directly.

Employer Sponsorship and Tuition Reimbursement

If you are already working for a mid-size or large employer, someone else may be willing to foot part, or all, of your MBA bill. Employer-funded education is one of the most underused financing levers available to working professionals, yet it can dramatically reduce your out-of-pocket cost and post-graduation debt.

Full Sponsorship vs. Tuition Reimbursement

These two arrangements differ in scope and commitment.

- Full sponsorship: The company covers tuition, fees, and sometimes your salary while you attend a full-time program. This model is most common in management consulting (McKinsey, BCG, Bain), the military (via the GI Bill and related programs), select tech firms (Google, Amazon), and certain private equity and hedge fund shops. You typically leave your role, earn your degree, and return to the firm afterward.

- Tuition reimbursement: The company reimburses a capped dollar amount per year after you complete coursework. Under IRS Section 127, employers can provide up to $5,250 per year tax-free. Many organizations go above that threshold, though amounts beyond the cap are treated as taxable income. Reimbursement is far more common than full sponsorship and is frequently tied to part-time or executive MBA formats that let you keep working.

Part-time and executive MBA vs. MBA formats are reimbursed more often than full-time programs because they allow the employer to retain your labor while investing in your development. If staying employed is feasible, these formats can unlock company dollars that a full-time program would not.

A 4-Step Negotiation Framework

Even when a formal policy exists, you will usually need to make a persuasive case.

1. Research your company's education benefits policy. Start with HR documentation, then talk to colleagues who have used the benefit. 2. Build a business case. Identify specific skills, leadership competencies, or strategic priorities the MBA will address. Quantify the return to the organization, not just to you. 3. Propose a service commitment. Employers worry about training you and losing you. Offering to stay for a defined period (typically two to three years post-graduation) signals good faith and makes approval more likely. 4. Get the agreement in writing. Spell out covered expenses, payment timing, GPA requirements, and what happens if either party ends the relationship early. A written agreement protects both sides.

Where Sponsorship Is Most Common

Some sectors have a long track record of funding MBA education:

- Military service members and veterans can access GI Bill benefits that cover full tuition at many programs, plus a housing allowance.

- Top-tier consulting firms routinely sponsor associates headed to full-time MBA programs, often with a salary stipend.

- Large tech companies sometimes offer tuition assistance as part of retention packages for high performers.

- Select finance firms, particularly in private equity and hedge funds, sponsor analysts who plan to return after business school.

Understand the Trade-Offs

Employer funding rarely comes without strings. Most sponsorship agreements require two to three years of post-MBA service with the same company. If you leave early, you may owe a prorated repayment of tuition. This commitment can limit your exit options, especially if the MBA opens doors to a different industry or role you did not anticipate.

Before signing, weigh the financial savings against the flexibility you may be giving up. For some professionals, the reduction in debt is well worth the commitment. For others, especially career-switchers, self-funding or scholarships may preserve the optionality that makes the MBA worthwhile in the first place. If you are still exploring which direction your degree could take you, reviewing common MBA career paths can help clarify whether a service commitment aligns with your goals.

If your employer offers any form of education assistance, explore it early. Even partial reimbursement layered on top of scholarships or savings can meaningfully shrink the financing gap.

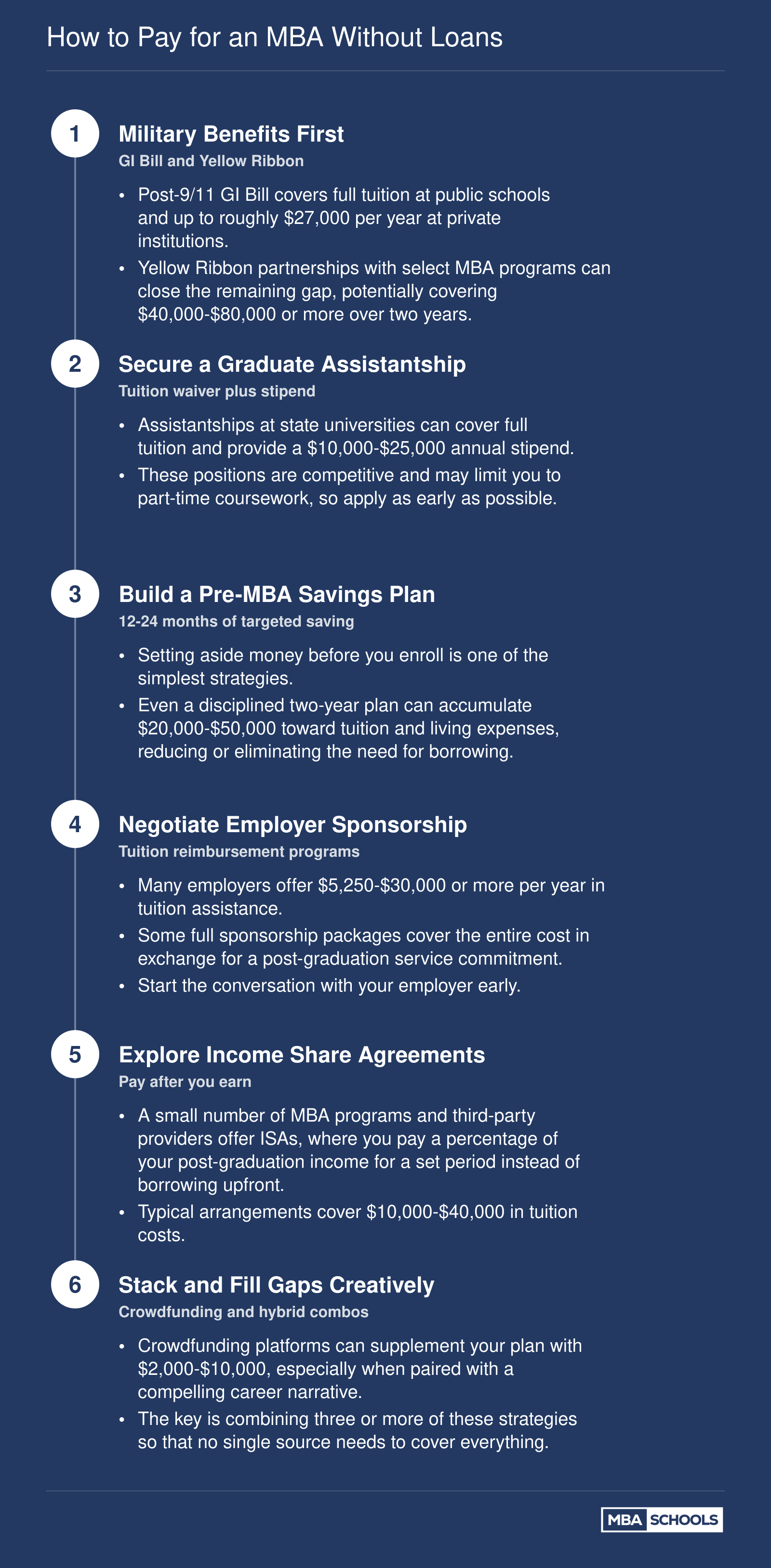

How to Pay for an MBA Without Loans

A debt-free MBA is achievable, but rarely through a single funding source. Most students who graduate without borrowing combine three or more strategies to cover the full cost of attendance. Here is a practical sequence for stacking no-loan funding, from the options you should lock in earliest to those you layer on last.

MBA Loan Repayment, Forgiveness, and ROI

Earning your MBA is one thing. Paying it off is another. Understanding how much debt you may carry, what relief programs exist, and whether the long-term salary premium justifies the investment are essential questions every prospective student should answer before signing a promissory note.

What Is the Average MBA Debt After Graduation?

MBA debt varies dramatically depending on the type of program you attend. Based on data from GMAC surveys and federal reporting through NCES, here are the general ranges by program tier:

- M7 and top-10 programs: $100,000 to $150,000 in total student loan debt is common, reflecting tuition that can exceed $80,000 per year before living expenses.

- Top-25 programs: Graduates typically carry $70,000 to $100,000, with variation depending on scholarship support and cost of living in the program's city.

- Regional and online programs: Debt tends to fall between $30,000 and $60,000, thanks to lower tuition and the ability to continue working while enrolled.

These figures represent loan balances at graduation, not total cost of attendance, which also includes opportunity cost for full-time students who forgo two years of salary.

Public Service Loan Forgiveness for MBA Graduates

Can you get loan forgiveness with an MBA? The answer is yes, but only under specific conditions. The federal Public Service Loan Forgiveness (PSLF) program discharges remaining federal loan balances after 120 qualifying monthly payments (roughly 10 years) made while working full time for a qualifying employer. Qualifying employers include federal, state, and local government agencies, 501(c)(3) nonprofits, and certain public health organizations.

The catch: most MBA graduates pursue private-sector careers in consulting, finance, or tech, which do not qualify. However, if you plan to work in healthcare administration, government management, nonprofit management, or public policy, PSLF can be a powerful tool. Only Direct Loans (or consolidated loans under the Direct Loan program) are eligible, and you must be enrolled in an income-driven repayment (IDR) plan.

For those who do not qualify for PSLF, IDR plans still offer a safety net. Under plans like SAVE, PAYE, or IBR, any remaining balance is forgiven after 20 to 25 years of payments. Be aware that forgiven amounts under IDR (unlike PSLF) may be treated as taxable income, though a temporary federal provision currently shields borrowers from that tax through 2025.

School-Based Loan Repayment Assistance Programs

Several top business schools offer their own Loan Repayment Assistance Programs, often called LRAPs, to graduates who take lower-paying positions in the public interest, nonprofit, or social-impact sectors. Schools like Harvard Business School, Stanford GSB, Wharton, and Yale SOM provide annual grants or loan subsidies for qualifying alumni, sometimes covering payments entirely for the first several years after graduation.

LRAP eligibility typically depends on your salary level, employer type, and sometimes the percentage of your income going toward loan payments. If you are considering a mission-driven career path, researching a school's LRAP offering before you apply can significantly influence your funding strategy.

Is the MBA Worth It? Framing ROI the Right Way

The question of whether is an mba worth it in your concentration comes down to a straightforward calculation. An MBA ROI analysis compares total cost of attendance plus opportunity cost (lost wages during a full-time program) against the salary premium you earn over a defined period, typically 10 years post-graduation.

Median starting salaries for graduates of top-25 programs generally fall between $120,000 and $175,000, according to GMAC Corporate Recruiters Survey data. If your pre-MBA salary is $65,000, the cumulative earnings gain over a decade can easily surpass $500,000, even after subtracting $150,000 or more in total program costs. Finance and consulting concentrations tend to produce the highest near-term returns, while entrepreneurship and nonprofit management paths may take longer to break even financially but offer other forms of value.

Before borrowing, use an MBA ROI calculator to model your own numbers. Factor in realistic salary expectations for your target industry, the specific cost of your target program, expected scholarship aid, and how quickly you plan to repay. We encourage every applicant to build a personalized funding plan, because the right MBA at the right price is almost always a strong investment, while the wrong financing strategy can undermine even a top-tier degree.

Frequently Asked Questions About Financing Your MBA

Financing an MBA raises a lot of practical questions, from whether full funding is realistic to how debt compares with long-term earnings. Below, we answer the most common questions prospective MBA students ask when mapping out their funding strategy.

The smartest MBA financing plans follow a clear order: exhaust mba scholarships, fellowships, and grants first, then maximize federal loans for their fixed rates and borrower protections, layer in private loans only as needed, and negotiate employer sponsorship to close any remaining gap. As we covered earlier, most students who graduate debt-free stack three or more of these strategies together.

Before you commit to any program or debt load, run your own ROI calculation. Compare projected post-MBA earnings against total cost of attendance, including forgone salary, to confirm the math works for your career goals. If you are still weighing whether the numbers add up, our breakdown of whether an MBA is worth it in 2026 can help you pressure-test your assumptions. Your concrete next step: visit your target school's financial aid page and submit the FAFSA for grad school as early as possible, even if you doubt you will qualify. Eligibility surprises happen, and filing opens doors to federal aid you cannot access otherwise.

Explore More

- AACSB-Accredited MBA

- Best GRE Prep Courses for MBA Applicants

- Best Military-Friendly MBA

- DISC Assessment for MBA Students & Graduates

- Executive MBA Courses

- Executive MBA vs. MBA

- FAFSA for MBA Students

- Financial Aid for Minority MBA Students

- GMAT Study Guide

- GRE Guide for MBA Applicants

- How Much Does an Online MBA Cost? Full Breakdown

- How to Choose the Right MBA

- How to Pay for an MBA

- LGBTQ+ MBA

- MBA Accreditation Types

- MBA Admissions Consulting Guide

- MBA Admissions Rounds vs. Rolling Admissions

- MBA Capstone Projects

- MBA Careers Guide

- MBA Entrance Exams

- MBA FAQ

- MBA Glossary

- MBA Preparation Courses

- MBA Requirements

- MBA Resume Guide

- MBA Salary

- MBA Scholarships

- MBA Scholarships for AAPI Students

- MBA Scholarships for Black Students

- MBA Scholarships for Hispanic & Latino Students

- MBA Scholarships for International Students

- MBA Scholarships for Women

- MBA vs. Master's Degree

- Military MBA Financial Aid

- Mini-MBA

- Native American MBA Scholarships

- Undergraduate Prerequisites for MBA

- What Is a STEM MBA Program? Benefits, Schools & OPT Guide

- What Is an MBA? Your Complete Guide to MBA Degrees