What you’ll learn in this article…

- Admissions committees evaluate the founder, not the venture, so essays should demonstrate judgment and self-awareness instead of a pitch deck.

- Founders without traditional supervisors can use investors, co-founders, board members, or clients as recommenders at most top programs.

- Stanford, HBS, Wharton, MIT Sloan, and Babson rank among the strongest MBA ecosystems for entrepreneur applicants in 2026.

- Full admissions consulting is most valuable for career switchers targeting M7 schools, while experienced applicants often need only essay review.

Fewer than 15 percent of applicants at top MBA programs come from entrepreneurial backgrounds, yet admissions committees at schools like Harvard Business School, Wharton, and Booth actively recruit founders. The catch: those same committees are among the most skeptical readers a founder will ever face.

The central tension is not whether founders belong in business school. It is whether a specific founder, at this stage of a specific venture, has a credible reason to stop building and start studying. Pre-revenue entrepreneurs, active founders, applicants whose companies have failed, and professionals who want to launch something after graduation all face versions of that same pressure.

The admissions challenge for founders is structural. Most application frameworks assume a corporate career path: promotions, performance reviews, a clear supervisor. Founders have none of those signposts. Translating venture experience into the language admissions committees trust, sourcing recommenders outside a traditional reporting chain, and making a compelling case for why an MBA accelerates rather than interrupts a founder's arc requires a different playbook entirely. This guide covers how to choose an MBA admissions consultant suited to founder profiles, how to structure your narrative, and how to select programs whose entrepreneurship ecosystems match your post-MBA ambitions.

The Core Admissions Challenge: Why 'I'm Already Building Something' Isn't Enough

Why would a working founder, who already has product, customers, or funding, pause that momentum to spend two years and six figures on a degree? That is the question every admissions committee will ask before reading your second essay, and it is harder to answer well than most applicants expect.

The Question Behind the Question

On the surface, adcoms are asking about your goals. Underneath, they are testing whether the MBA actually adds something you cannot get by continuing to build. If your venture is succeeding, the case for leaving has to be specific: a capability gap, a network gap, a credibility gap, or a pivot that genuinely requires structured learning. If your venture has stalled or closed, the case has to avoid sounding like a retreat. Either way, vague answers ("I want to scale", "I need a stronger network") read as a founder who has not done the diligence on their own next chapter.

The Three Things Adcoms Must Believe

What MBA admissions committees look for goes beyond traction metrics. Readers of founder applications need three convictions before they advocate for an admit:

- Business judgment: Your decisions, whether to pursue a market, hire a cofounder, kill a product, raise capital, show pattern recognition and trade-off awareness, not just hustle.

- Self-awareness about gaps: You can name what you do not yet know (finance, operations at scale, a new industry, people leadership) and explain why classroom learning and peers will close that gap faster than another year of solo iteration.

- A credible post-MBA plan that benefits from the degree: Whether you are returning to your venture, joining a larger company, or starting something new, the path should be one where the MBA materially changes your trajectory, not one you could execute tomorrow without it.

Founder Mindset vs. Adcom Mindset

Founders are trained to sell the vision. Adcoms are trained to test the person behind the vision. That mismatch is where most entrepreneur applications fall apart. A pitch-deck MBA essay narrative full of traction metrics and market-size claims signals that the applicant is still in fundraising mode rather than reflecting on their own development. Admiration for entrepreneurship is real, but it does not translate to an admit on its own. Committees will still pressure-test whether the evidence is substantial, whether the lessons are honest, and whether the goals are realistic given your track record.

What Admissions Committees Look for in Founder Applicants

Admissions officers reading a founder's application are not evaluating the venture as an investor would. They are evaluating the person behind it. They want signals of judgment, growth, and the kind of leadership that will translate into classroom contribution and post-MBA impact. Pitch language, hockey-stick projections, and TAM slides do not move the needle. Concrete evidence of how you have operated under uncertainty does.

The Evidence That Actually Counts

Strong founder applications surface specific, verifiable proof points. MBA application evaluation factors extend well beyond traditional metrics, and across successful candidates, the recurring categories of evidence include:

- Revenue: Actual dollars earned, with context on margin and growth trajectory.

- Customer traction: Named accounts, retention rates, referenceable buyers, or pilot conversions.

- User growth: Cohort behavior, engagement metrics, organic vs. paid acquisition mix.

- Funding: Capital raised, investor quality, valuation context, or bootstrapped runway decisions.

- Product development: What you shipped, how you prioritized, what you killed.

- Team building: Who you hired, how you retained them, how you handled departures.

- Partnerships: Distribution deals, channel relationships, or strategic alliances you negotiated.

- Market validation: Evidence that customers want the thing, not just that you want to build it.

- Operational learning: Unit economics, hiring playbooks, supply chain decisions, pricing experiments.

- Failed experiments with clear lessons: What you tried, what broke, what you would do differently.

- Personal financial risk: Salary forgone, savings invested, opportunity cost shouldered.

- Strategic decision-making: Pivots, market choices, build-vs-partner calls, and the reasoning behind them.

You do not need every category. You need a credible cluster, presented with specificity rather than adjectives.

Where Founders Are Strongest

Founders typically over-index on dimensions corporate applicants struggle to demonstrate: real-world leadership without a title to hide behind, comfort operating with incomplete information, resourcefulness when budgets are thin, and the initiative to create roles rather than fill them. Adcoms recognize these as scarce traits in an MBA class and value the texture they bring to case discussions and team projects. For founders weighing how an MBA translates into career outcomes, jobs after mba in entrepreneurship range from launching new ventures to scaling existing ones within larger organizations.

Where Founders Are Most Vulnerable

The same profile carries predictable weaknesses. Quantitative proof can be thin if the venture is early, financial statements informal, or metrics inconsistently tracked. There is often no traditional promotion arc to point to, no peer cohort for the committee to benchmark against, and a fair concern that a founder who is already running something may not fully engage with a two-year program, or may not return to the workforce in a way that strengthens the school's outcomes. Your application needs to anticipate each of these doubts and answer them with evidence, not assertion.

Questions to Ask Yourself

Building the Founder Narrative: Essay and Resume Strategy

Most founder applicants know their venture inside out, but that fluency becomes a liability the moment they sit down to write MBA essays. The instinct to pitch is hard to suppress, and it is precisely that instinct that weakens most founder applications.

The Framework That Works

A reliable structure for mba essay narrative strategy moves through six stages: problem observed, venture action, leadership challenge, business lesson, MBA need, and future ambition. Each stage does specific work. The problem observed establishes that you identified something others missed. The venture action shows you moved on it. The leadership challenge surfaces a moment of real difficulty, not a highlight reel. The business lesson demonstrates what you extracted from that difficulty. The MBA need explains concretely what the degree gives you that experience alone cannot. And the future ambition closes with a credible, specific direction, not a vague declaration about disrupting an industry.

This framework keeps the essay grounded in judgment and growth rather than company promotion. Admissions committees are not evaluating your startup. They are evaluating whether you are worth a seat in the class.

Pre-Revenue Founders

Not having revenue does not disqualify a founder, but it raises the evidentiary bar on everything else. If your venture has not yet generated income, your essays must do more work to establish credibility. Focus on the depth of your market insight: how you identified the problem, what customer discovery you conducted, and how your understanding has evolved. Execution speed matters too. Show the committee how quickly you moved from idea to prototype, from prototype to feedback, from feedback to iteration. Learning velocity, meaning how fast you absorbed and acted on new information, is something admissions readers actively look for in early-stage founders.

Framing Failed Ventures

A failed or shuttered venture is not a disqualifier. It is usable material if handled with maturity. The key is specificity. Saying a venture failed because of poor market timing is too easy. Explaining what you learned about customer acquisition costs, why your initial hiring decisions created friction, or how your assumptions about product-market fit turned out to be wrong, that kind of granular reflection signals real business judgment. Committees want to see that failure taught you something durable, not just something painful.

Resume Strategy for Founders

Your mba resume strategy should read as a professional trajectory, not a company biography. Quantify wherever you can, even in small ventures: users served, revenue generated, team size, funding raised, partnerships secured. These numbers give context and credibility. Avoid listing every feature your product ever shipped. Instead, show decisions made, results produced, and responsibilities carried. The resume is a document of your growth as a professional, and for founders, the most compelling versions make that arc visible even across unconventional career paths.

The Founder Essay Framework: From Venture to Ambition

Strong founder essays follow a clear narrative arc, not a pitch deck. Each stage should demonstrate judgment, growth, and self-awareness rather than hype about your venture's potential.

Recommendation Strategy for Founders Without Traditional Supervisors

Most top MBA programs require two or three letters of recommendation, and the standard guidance assumes a traditional supervisor relationship. Founders without a manager, boss, or direct supervisor face an immediate structural disadvantage: the typical recommender playbook does not apply. The solution is not to force-fit an irrelevant reference, but to understand what admissions committees actually need from a recommendation and then identify the relationship that delivers it.

What Admissions Committees Want from Recommenders

Recommendation letters serve three functions. First, they verify leadership, judgment, and impact through observed behavior. Second, they provide context for claims made in essays and resumes. Third, they reveal how the applicant is perceived by someone with authority or credibility. For founders, this means the recommender must be someone who has observed decision-making, witnessed personal growth, or collaborated closely enough to comment on character and capability. Revenue numbers and product launches matter less than evidence of the founder's judgment under pressure.

Who Can Write for Founders

The best recommenders for entrepreneur applicants typically fall into one of four categories. Investors, advisors, board members, or mentors who have worked closely with the founder can speak to strategic thinking, receptiveness to feedback, and leadership maturity. Co-founders or senior team members can address collaboration, conflict resolution, and operational execution. Clients, partners, or industry veterans who have worked with the venture in a professional capacity can validate business acumen and external impact. In rare cases, a previous employer from a role held before founding the company may still be relevant if the experience is recent and the relationship remains strong.

How to Research School-Specific Policies

Recommendation policies vary by program, and assumptions about what is acceptable can derail an application. The first step is to check each school's MBA admissions website directly. Look in the application requirements section or the recommendations tab. Many programs maintain dedicated FAQ pages or admissions blog posts addressing nontraditional applicants, including entrepreneurs. Stanford GSB, Wharton, and similar schools often publish guidance on choosing recommenders when a supervisor is not available.

School admissions blogs and podcast archives are underused resources. Search for terms like entrepreneur, recommender, or startup founder to surface relevant posts. If public guidance is unclear, contact the admissions office directly via email or attend an online information session. Ask explicitly whether the program accepts recommendations from investors, clients, or co-founders, and request any written policy if it is not published. Admissions teams expect these questions and typically respond with clarity. Understanding what makes a strong MBA recommendation letter before reaching out will help you ask sharper, more targeted questions.

Professional associations like the Forté Foundation and The Consortium sometimes compile recommendation best practices for nontraditional applicants. These resources are not school-specific, but they offer frameworks that can inform recommender selection when official guidance is sparse.

Common Mistakes to Avoid

The most damaging mistake is choosing a recommender based on title rather than relationship depth. A famous investor who barely knows the applicant will write a generic letter that does more harm than good. A co-founder with daily interaction and direct observation of leadership will write a stronger letter than a distant advisor, even if the advisor has a more impressive résumé. The second mistake is failing to brief recommenders properly. Founders should provide context on the MBA program, the application narrative, and specific examples the recommender might reference. The third mistake is treating the recommendation as an afterthought. Strong letters require time, and last-minute requests produce weak results.

School Selection: MBA Programs With the Strongest Entrepreneurship Ecosystems

Choosing the right MBA program is a strategic decision that can accelerate or sidetrack a founder's career trajectory. The most effective entrepreneur applicants match a school's resources, culture, and alumni network to their specific post-MBA ambition, not just its reputation.

Top Programs and Their Entrepreneurship Ecosystems

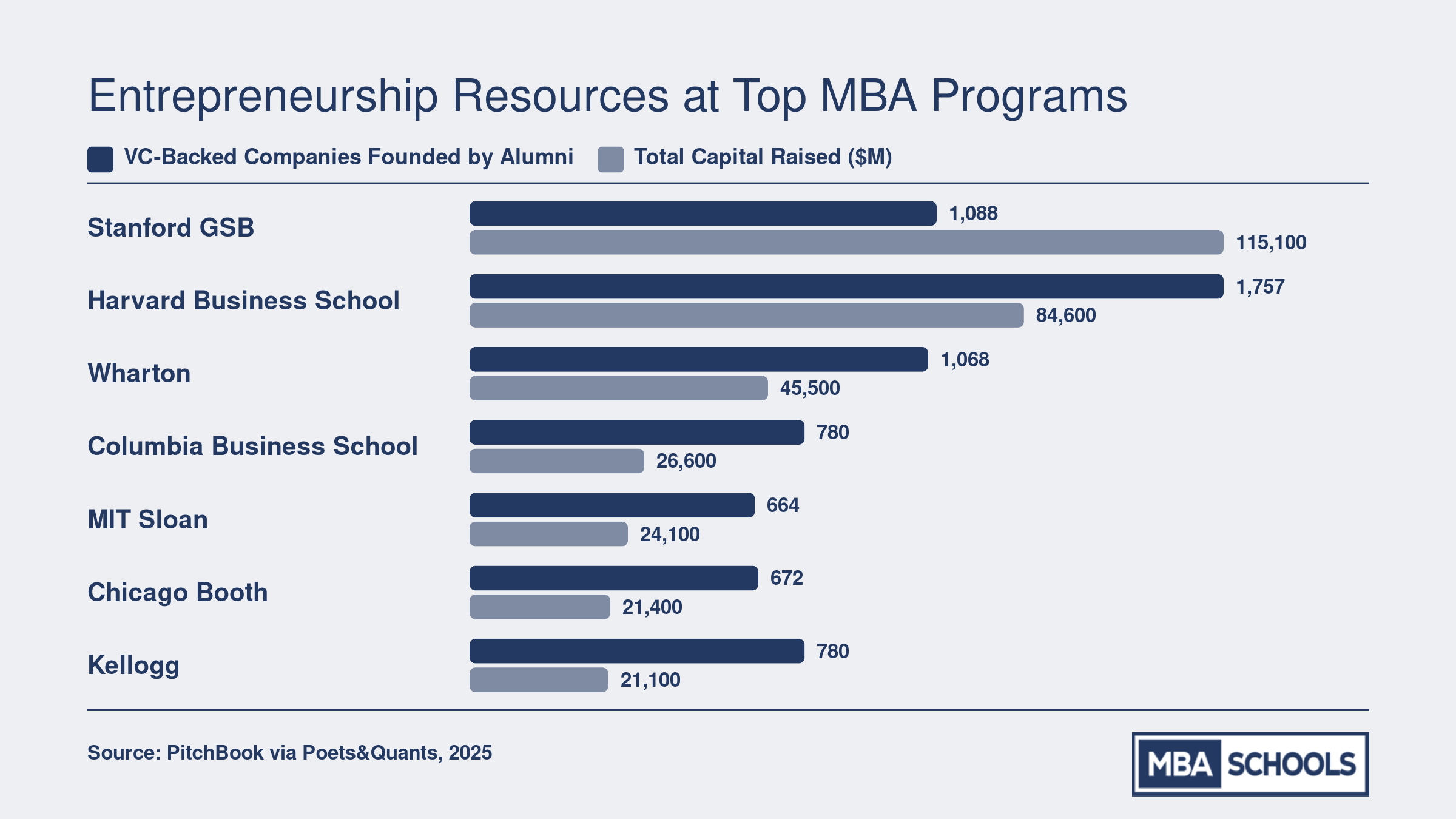

Several MBA programs stand out for deep, integrated support for founders. Harvard Business School runs the Rock Center for Entrepreneurship1, which in 2026 accepted 61 students into its Rock Venture Catalyst summer program. The Rock Center also provides Entrepreneurs-in-Residence, venture capital advisors, and legal specialists,3 and over 1,900 ventures have launched from HBS in the last decade.4 Stanford GSB's entrepreneurial DNA is legendary; its proximity to Silicon Valley and programs like Startup Garage and the Stanford Impact Founder Awards create potent founder pipelines. MIT Sloan offers delta v, an intensive summer accelerator operated by the Martin Trust Center, along with the $100K Competition. Wharton's Venture Initiation Program (VIP) functions as an educational incubator, while the Penn Wharton Entrepreneurship ecosystem provides seed funding and mentorship. At Chicago Booth, the New Venture Challenge, established in 1996, has awarded over $435,000 in investment to winning teams, with many participants securing real funding. Columbia Business School leverages its Lang Center for Entrepreneurship and the Columbia Startup Lab to support founders in New York City's dynamic market. For those drawn to the West Coast, UC Berkeley Haas integrates with Berkeley SkyDeck and the Lester Center for Entrepreneurship. Tuck's close-knit community offers personalized guidance through its Center for Entrepreneurship and Dartmouth Entrepreneurial Network.

PitchBook university rankings consistently place Stanford, MIT, and Harvard at the top of MBA-founded company counts and venture capital raised, but schools like Wharton MBA program and Booth produce significant exit value as well. When reviewing these figures, ask whether the numbers reflect startups launched during the MBA or the long-term alumni network effect.

Matching Programs to Your Founder Path

Your intended post-MBA route should heavily influence school selection. For a broader view of how entrepreneurship MBA programs structure their curricula around founder outcomes, compare programs across ecosystems before committing to a target list.

- Scaling an existing venture: Look for programs with flexible schedules, strong executive networks, and leadership courses. HBS and Stanford offer robust alumni connections and investor access, while Booth's evening and weekend options might suit founders who cannot pause operations.

- Launching a new company after graduation: Prioritize schools with extensive accelerator programs, seed funding, and physical co-working space. MIT's delta v, Wharton's VIP, and Columbia's Startup Lab provide hands-on environments to test ideas.

- Joining a high-growth startup: Geographic ecosystem matters. Stanford and Haas sit in the Bay Area; Sloan and HBS are in Boston; Columbia and NYU Stern anchor New York. Access to local startup talent flows and venture capital firms during the MBA can shape your immediate role.

- Pivoting into venture capital: A handful of schools feed directly into top VC firms. Stanford, HBS, and Wharton have formal and informal tracks that produce a disproportionately high share of junior investors. Seek programs with student-run VC funds and strong finance-entrepreneurship intersection.

Standardized Testing for Founder Applicants

Founders with unconventional academic profiles often worry about the GMAT or GRE. Most top MBA programs accept either exam, and the GRE is often gentler on non-quantitative backgrounds. However, test-optional policies remain rare among the top entrepreneurship schools; most still require a score, and a competitive result remains one of the few standard benchmarks for comparing applicants with non-traditional paths. If your undergraduate GPA is weak, a strong GMAT quant score or GRE equivalent can serve as offsetting evidence. For founders who have built successful ventures, the operating experience itself may demonstrate analytical capability, but do not assume admissions committees will disregard low scores without a compelling narrative. Prepare early, aim for a score near the program's median, and consider a test-prep consultant if you have been away from classroom testing for years.

The right MBA program amplifies your founder credibility. Align its tools with your destination, and your application will show a deliberate career architect, not just an entrepreneur with a degree plan.

Entrepreneurship Resources at Top MBA Programs

A program's founder alumni network is one of the strongest signals of its entrepreneurship ecosystem. The PitchBook rankings track how many MBA alumni have gone on to found venture-capital-backed companies and how much total capital those companies have raised. For prospective founder applicants, these numbers reveal where the deepest startup networks, mentorship pipelines, and investor relationships live.

Interview Prep, Scholarships, and ROI: What Founders Get Wrong

Founders routinely underestimate how much the MBA decision costs them, and overestimate how quickly it pays back. Before you submit a single application, you need a clear-eyed accounting of what you are giving up, what you are spending, and what you realistically gain on the other side.

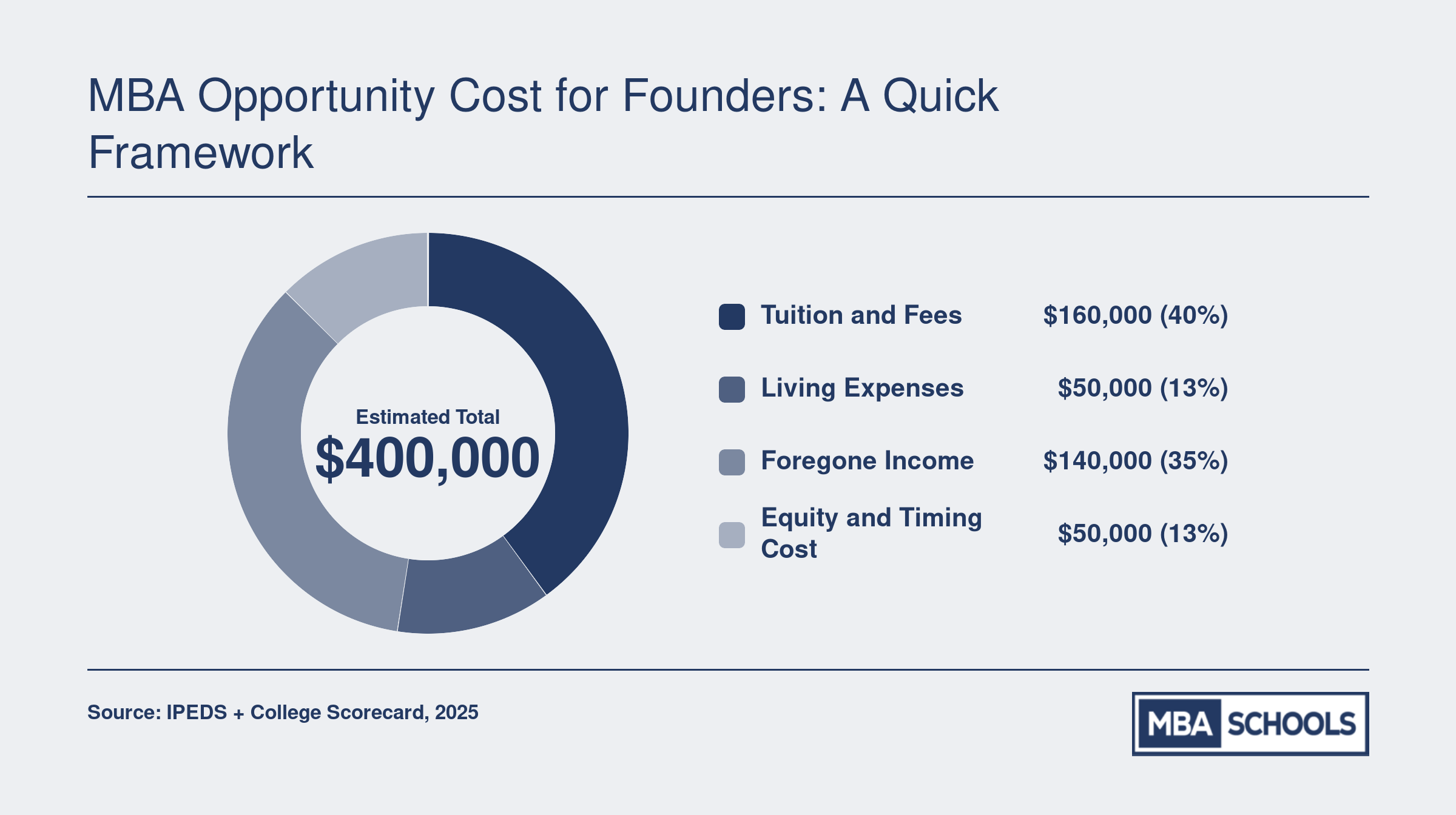

The Real Cost of Attendance

Top MBA programs publish detailed cost-of-attendance figures on their official websites each academic year. These figures typically include tuition, fees, housing, health insurance, and estimated personal expenses. The total is almost always higher than tuition alone, sometimes by a significant margin. Before anchoring to any number you read in a forum or a rankings article, go directly to each school's financial aid or admissions page and pull the current figures for the year you plan to enroll. Numbers shift annually, and rounding down to a comfortable estimate is one of the most common financial mistakes applicants make.

Opportunity Cost Is the Number Founders Forget

For a founder, opportunity cost is not just a foregone salary. It includes deferred equity vesting, lost fundraising momentum, team continuity risk, and the compounding value of product decisions made in real time. Salary benchmarking tools like Glassdoor or Payscale can give you a baseline for what operators with your background typically earn, and startup compensation surveys can help you think through equity timing. The question is not only what you will earn after the MBA, but what you and your company lose while you are away.

Post-MBA earnings data from schools is worth examining carefully. Many programs publish employment reports that break out outcomes by career track, and some, including schools with well-known entrepreneurship centers, publish separate reports on venture creation rates and founder income trajectories. These documents are more useful than generic salary averages because they reflect what people with entrepreneurial post-MBA intentions actually experienced. Calculating MBA ROI with scholarships and aid gives you a more complete picture of what the numbers mean over a realistic payback horizon.

Interview Strategy for Founders

Founders often perform well in MBA interviews on energy and storytelling, then stumble on precision. Interviewers at selective programs will probe the substance behind the narrative. They will ask what specific decisions you made, what you got wrong, and why the MBA is necessary at this exact moment in your career rather than later. Rehearsing vague answers about disruption or passion will not serve you. Prepare concise, evidence-based answers that connect your venture experience to concrete lessons and then to a specific post-MBA plan.

Scholarships and Funding

Many founders assume merit scholarships are reserved for candidates coming from investment banks or consulting firms. That is not accurate. Schools with active entrepreneurship programs often recognize founder applicants as strong scholarship candidates, particularly when the venture evidence is compelling and the application is well-positioned. Research each school's named fellowships and entrepreneurship-specific funding opportunities before you assume the sticker price is fixed. Ask admissions consultants about schools where founder profiles have historically attracted scholarship consideration, and treat financial aid as part of your school selection conversation, not an afterthought.

MBA Opportunity Cost for Founders: A Quick Framework

The sticker price of an MBA is only part of the equation. For founders, the real cost includes income you stop earning, living expenses during the program, and the harder-to-quantify impact of stepping away from a venture at a critical moment. This framework uses representative figures from top-tier two-year, full-time programs to help you size the total investment.

When MBA Admissions Consulting Is Worth It, and When It Isn't

Not every founder needs a full admissions consulting package, and claiming otherwise would be dishonest. The right level of support depends on your background, your target schools, and how well you already understand the process. Here is a straightforward breakdown to help you decide.

Pros

- First-generation applicants or founders without MBA networks benefit enormously from expert guidance on norms, expectations, and positioning they would not learn on their own.

- Founders with unconventional backgrounds (no corporate experience, nontraditional education, career gaps) need narrative coaching to translate their story into language admissions committees trust.

- Applicants targeting M7 or other highly selective programs face acceptance rates below 15 percent, where small differences in essay quality and positioning can determine outcomes.

- Candidates who have been denied in a previous cycle often repeat the same strategic mistakes without outside perspective on what went wrong.

- Pre-revenue or failed-venture founders need careful help framing their experience as evidence of leadership and judgment rather than a liability.

Cons

- Serial applicants who have been through the process before and understand school-specific expectations can often self-guide with minimal outside input.

- Founders with strong writing skills, genuine self-awareness, and a clear post-MBA plan may already have the tools to craft a compelling application independently.

- Applicants targeting less competitive programs where acceptance rates exceed 40 percent are unlikely to see a return on a full consulting investment.

- Experienced founders who have board advisors, mentors, or MBA alumni in their network can often get quality feedback without paying for it.

- Candidates on tight budgets should weigh whether consulting fees meaningfully reduce the financial runway they need for their venture or MBA tuition.

Common Questions About MBA Admissions for Entrepreneurs

These are the questions founders ask most often when weighing an MBA application. Each answer is deliberately concise; for deeper treatment, refer to the corresponding section of this guide.

Related Articles

Submitting an application versus building one are two different exercises. The first is paperwork. The second is strategy, and founders who skip straight to the forms usually pay for it in weaker essays and weaker outcomes.

Three things matter most. Prove the founder, not the company: admissions committees are evaluating your judgment, not your valuation. Solve the recommender problem early, because founders without traditional supervisors need months to brief the right advocates. And match the school's ecosystem to your actual post-MBA goal, not its ranking.

Start with the Founder MBA Narrative Builder framework before you open a single application portal. Map your venture proof points, leadership stories, and why-MBA argument first. For founders who want structured guidance on how each piece connects, MBA admissions consulting by applicant type offers a broader view of how different profiles approach the process. Not every founder needs a consultant, but every founder needs a strategy, and the strategy comes before the form.

Explore More

- MBA Admissions Consulting for Career Switchers

- MBA Admissions Consulting for Consultants

- MBA Admissions Consulting for Engineers

- MBA Admissions Consulting for Finance Professionals

- MBA Admissions Consulting for First-Generation Applicants

- MBA Admissions Consulting for Healthcare Professionals

- MBA Admissions Consulting for Military Veterans

- MBA Admissions Consulting for Reapplicants

- MBA Admissions With a Low GPA