What you’ll learn in this article…

- Post-MBA PE associates routinely earn over $200,000 in base salary, with total compensation climbing much higher.

- An MBA is not required for private equity, but it remains the most reliable career-switching path into the industry.

- Harvard, Stanford, and Wharton dominate megafund placement, yet middle-market and growth equity firms recruit from a wider set of programs.

- Carried interest, not base pay, is the true wealth engine for PE professionals at the Vice President level and above.

Private equity firms now manage more than $8 trillion in global assets, and MBA graduates remain the primary feeder into associate roles at buyout, growth equity, and middle-market shops. That pipeline is well established, but it is also ruthlessly selective: top megafunds extend offers to fewer than 30 candidates per year, often before the first semester of business school is finished.

The central tension is straightforward. PE offers some of the highest post-MBA compensation in any industry, yet the path demands precise timing, targeted program selection, and pre-MBA credentials that most career switchers need years to build. Even candidates from elite programs face rejection rates north of 90 percent at the most sought-after firms. The margin for error in recruiting preparation is razor-thin, and the window to act is shorter than most applicants expect. This guide breaks down what PE professionals actually do, which MBA programs place the most graduates into the industry, how recruiting timelines work, what you can expect to earn, and how to best jobs for mba graduates position yourself for success whether you come from a finance background or not.

What Does a Private Equity Analyst or Manager Actually Do?

Before mapping out the MBA path, it helps to understand exactly what private equity professionals do every day and where you would slot into the hierarchy after graduating. The term "private equity analyst" dominates search queries, but the reality is more nuanced: post-MBA hires almost always enter PE firms as associates, not analysts. Analysts are typically pre-MBA professionals (often straight out of mba in investment banking programs), while associates sit one rung higher and carry broader deal responsibilities. This guide covers both search intents because many readers are researching the field for the first time, while others already know they want the associate track and need a roadmap to get there.

The PE Hierarchy at a Glance

Most private equity firms follow a relatively standard career ladder:

- Analyst: Pre-MBA; supports deal teams with modeling, research, and data gathering. Typical tenure is two to three years.

- Associate: Post-MBA entry point; leads workstreams on active deals, manages analysts, and interacts directly with portfolio company management.

- Vice President (VP): Oversees multiple deals simultaneously, mentors junior staff, and begins taking on client-facing and fundraising responsibilities.

- Principal/Director and Partner: Senior roles focused on deal origination, fund strategy, and investor relations.

The jump from analyst to associate is where an MBA creates the most value, both in skill development and in signaling readiness for greater responsibility.

A Typical Day in Private Equity

PE work centers on identifying, acquiring, improving, and eventually selling companies. Day-to-day tasks shift depending on deal flow, but associates generally rotate among several core activities:

- Deal sourcing: Screening potential acquisition targets, reviewing pitch decks from investment banks, and building relationships with intermediaries who surface opportunities.

- Financial modeling: Constructing and stress-testing leveraged buyout (LBO) models to determine how much a firm can pay for a target and still achieve its return hurdle.

- Due diligence: Coordinating teams of lawyers, accountants, and consultants to verify a target company's financials, operations, customer contracts, and legal standing.

- Portfolio company monitoring: Tracking KPIs, attending board meetings, and collaborating with management teams on strategic initiatives like add-on acquisitions or cost-reduction programs.

- Exit planning: Analyzing optimal timing and structure for selling a portfolio company, whether through an IPO, secondary sale to another fund, or strategic acquisition.

These responsibilities make PE distinctly hands-on. You are not simply advising a client; you are co-owning the outcome.

How PE Differs from Investment Banking and Hedge Funds

Investment bankers advise on transactions and move on once a deal closes. Hedge fund professionals trade securities and manage liquid portfolios with short feedback loops. Private equity sits between the two: deals take months to execute and years to realize returns. Hours can still be demanding, especially during live deals, but the chronic 80-to-100-hour weeks common in banking are less typical outside of crunch periods. The trade-off is intellectual depth. Associates spend weeks, sometimes months, embedded in a single company's operations rather than juggling dozens of pitch books.

The Skill Stack PE Firms Value

Firms evaluate candidates on a combination of technical ability and softer leadership qualities:

- Mastery of LBO modeling and valuation techniques

- Deep knowledge of at least one industry vertical (healthcare, technology, industrials, and consumer are among the most active sectors)

- Leadership presence and the confidence to challenge portfolio company CEOs on strategy

- The ability to synthesize complex information under time pressure and present clear recommendations to investment committees

This skill stack is precisely why so many PE firms recruit from top MBA programs. The combination of structured finance training, case-based strategic thinking, and peer networks makes MBA graduates well-suited for a role that demands both analytical rigor and boardroom credibility. Understanding how PE fits within the broader landscape of MBA career paths and salaries can help you benchmark compensation expectations as you evaluate programs. The sections ahead will explore how to choose the right program and position yourself for these roles.

Do You Need an MBA for Private Equity?

The short answer: no, an MBA is not a formal requirement to work in private equity. The longer, more practical answer is that it remains the single most reliable path into the industry, especially if you are switching careers or targeting the largest firms.

The Structural Reality at Top Firms

At megafunds like KKR, Blackstone, Apollo, Carlyle, and TPG, the vast majority of associates hold MBA degrees. This is not because these firms mandate the credential in their job postings. It is because their recruiting pipelines are built around MBA programs. On-cycle recruiting at elite business schools gives firms a concentrated, pre-vetted talent pool, and the two-year MBA structure gives candidates a natural window to interview, intern, and convert offers. When you look at associate classes at these firms year after year, the MBA is less a requirement and more a deeply entrenched structural norm.

Some pre-MBA analysts at PE firms do get promoted directly into associate roles without returning to school. This path exists, but it is the exception rather than the rule, and it typically rewards candidates who joined the firm early, proved themselves over multiple deal cycles, and had strong internal sponsors.

When Skipping the MBA Makes Sense

If you spend time on forums like Wall Street Oasis or Reddit, you will encounter a vocal camp that argues the MBA is unnecessary: "Just stay in banking and lateral directly." That advice is not wrong for everyone. Skipping the MBA can make sense if:

- You are already working at a PE firm with a clear internal promotion track.

- You have a strong investment banking background (two-plus years at a top group) and can leverage lateral recruiting networks.

- You are confident you want to stay in PE and do not need the broader career optionality an MBA provides.

In these scenarios, the opportunity cost of two years out of the workforce, plus tuition north of $200,000 at many top programs, may genuinely outweigh the benefits.

When the MBA Adds Irreplaceable Value

For a much larger group of aspiring PE professionals, the MBA fills gaps that no amount of self-study or networking can replicate:

- Career switchers: If your background is in consulting, operations, engineering, or another non-finance field, the MBA is often the only realistic on-ramp into PE recruiting. Firms rarely consider lateral hires from outside finance without it.

- Brand signaling: A degree from a target program signals analytical rigor and peer caliber in a way that opens doors before you ever submit a resume.

- Structured recruiting access: MBA programs offer direct pipelines to PE firms through on-campus events, dedicated career offices, alumni networks, and organized interview processes that are nearly impossible to access as an independent applicant.

- A two-year runway to pivot: The MBA gives you time to build financial modeling skills, complete a PE summer internship, and test whether the lifestyle and work truly fit before committing to a multi-year associate role.

The Bottom Line

Think of the MBA not as a checkbox but as an infrastructure advantage. It compresses years of networking, skill-building, and job searching into a structured two-year sprint. If you are already embedded in the PE ecosystem with a clear trajectory, the degree may be optional. For nearly everyone else, particularly career changers and candidates from non-target backgrounds, it remains the most efficient and widely recognized path into private equity at the highest levels. Professionals weighing private equity against other post-MBA roles should explore the full range of careers for MBA graduates before committing to a single track. Similarly, candidates coming from mba in consulting career backgrounds will find the MBA especially valuable as a bridge into finance-oriented roles.

Questions to Ask Yourself

Best MBA Programs for Private Equity Careers

Before diving into specific programs, a word on how to interpret PE placement data. Employment reports vary in how they categorize private equity. Some schools group buyout roles under a dedicated "private equity" label, while others fold them into broader categories like "investment management" or "other finance." This means the published PE placement rate for any given school may undercount actual PE hiring. Use the figures below as a directional guide rather than an exact ranking, and supplement your research by speaking directly with PE club members at each program.

The Top Tier: HBS and Wharton

Harvard Business School and Wharton consistently place the highest raw number of graduates into private equity, which is partly a function of their large class sizes but also reflects deep, longstanding relationships with major buyout firms. HBS reported that roughly 14% of the Class of 2025 entered private equity1, a figure that translates to well over 100 graduates given the school's scale. Wharton's PE and Venture Capital Club is one of the most active in the world, running deal competitions, hosting annual conferences, and maintaining a network that spans mega-funds to middle-market firms. Both programs offer rich elective menus in LBO modeling, deal structuring, and fund economics.

Strong Contenders: Booth and Columbia

Chicago Booth and Columbia Business School punch above their weight on a per-capita basis when it comes to PE placement. Booth's analytical rigor and deep coursework in leveraged finance and private equity make it a favorite recruiting ground for quantitatively oriented firms. Columbia benefits from its New York City location, which provides proximity to a massive concentration of PE offices and deal flow. Both schools maintain active PE clubs and facilitate on-campus recruiting events that connect students directly with hiring managers at top firms.

Programs Worth Serious Consideration

Stanford GSB, Kellogg, NYU Stern, and Tuck each offer distinct advantages for PE-bound students, though their placement numbers tend to be smaller in absolute terms.

- Stanford GSB: Smaller class size means fewer total PE placements, but the school's prestige and West Coast network open doors to growth equity and tech-focused buyout firms.

- Kellogg: Known for collaborative culture and strong general management training, Kellogg graduates increasingly find their way to PE through both on-cycle and off-cycle recruiting.

- NYU Stern: Like Columbia, Stern leverages its Manhattan location for unmatched access to middle-market and mega-fund PE shops, and its curriculum includes specialized courses in private equity finance.

- Tuck: Tuck's tight-knit alumni network is legendary in finance circles, and the school's intimate class size means the PE club can provide highly personalized recruiting support.

What to Look for Beyond Placement Rates

When evaluating programs, consider several factors that employment reports alone cannot capture. If you are also weighing adjacent mba career paths, the criteria below will help you compare PE-focused programs on the dimensions that matter most.

- PE club strength: How active is the club? Does it run deal competitions, bring in guest speakers from major firms, and organize treks to PE offices?

- Curriculum depth: Look for dedicated courses in LBO modeling, fund formation, and portfolio company operations, not just general finance electives.

- Firm placement highlights: Ask admissions and career services which specific firms recruit on campus. A school that regularly sends graduates to firms on your target list is more valuable than one with a higher overall placement rate at firms you have never heard of.

- Alumni density at target firms: Check LinkedIn to see how many alumni from each program currently work at the PE firms you aspire to join. Alumni density often correlates with recruiting access.

Keep in mind that published placement data from schools other than HBS was not available for the most recent graduating class at the time of writing. For the most current figures, check each school's official employment report and reach out to PE club leadership directly. The landscape shifts each year, and a school that placed 8% of its class into PE last year may place 12% this year depending on fund fundraising cycles and broader market conditions.

Related Articles

Admission Requirements and How to Stand Out for Pe-Track MBAs

Getting into a top MBA program is competitive on its own. Getting in with the explicit goal of recruiting into private equity raises the stakes further, because PE firms draw from a narrow slice of each class. Understanding what admissions committees and, ultimately, PE recruiters look for can help you build a candidacy that serves both gatekeepers.

GMAT and GRE Benchmarks for PE-Focused Applicants

At M7 programs, the median GMAT score typically lands in the 730 range, but PE-track admits often score above that median. Why? Because private equity recruiting is one of the most selective post-MBA outcomes, admissions officers know that students targeting PE need to be competitive in on-campus recruiting against classmates with elite pre-MBA profiles. A 730 or higher signals quantitative rigor and helps your application clear internal screens. If you are submitting a GRE score instead, aim for a comparable percentile in the quantitative section (165 or above). A strong test score alone will not get you in, but a weak one can quietly disqualify you from PE-track consideration before you even set foot on campus.

The Ideal Pre-MBA Profile

PE firms treat MBA recruiting as an extension of pre-MBA deal experience. The most competitive candidates arrive with two to four years in investment banking (especially leveraged finance or M&A groups), management consultant MBA roles at a top firm, or corporate development positions where they led or supported transactions. This background matters because associate-level PE work demands fluency in financial modeling, due diligence, and deal structuring from day one. Firms rarely have the bandwidth to train someone on fundamentals during a 10-week summer internship.

Beyond your job title, recruiters pay close attention to the caliber of transactions you have touched and the complexity of analysis you have owned. If your pre-MBA experience includes live deal work, be prepared to discuss it in granular detail during interviews.

Crafting Your Application Strategy

Writing about PE ambitions in your essays requires a careful balance. Admissions committees want to see candidates with clear goals, but framing your entire narrative around a single outcome can come across as rigid. A stronger approach is to articulate why PE aligns with your broader career arc, perhaps connecting your deal experience to a long-term interest in building or transforming businesses, rather than simply stating you want to work at a megafund. For guidance on framing those goals effectively, review strong mba personal statement examples from admitted candidates.

Recommenders also matter more than many applicants realize. A letter from a senior banker or deal professional who can speak to your analytical depth and judgment under pressure carries significantly more weight than a generic leadership endorsement from a manager outside of finance. If you have worked alongside PE professionals on a deal, a recommendation from that context is especially powerful.

The firms on your resume before business school also signal readiness. Bulge-bracket banks, elite boutiques, and top-tier consulting firms are well-understood brands that PE recruiters trust. If your pre-MBA employer is less recognizable, compensate by emphasizing the sophistication of your work and the outcomes you drove.

Breaking In Without Finance Experience

If you are coming from a non-finance background, such as operations, engineering, or the military, the path to PE through an MBA is steeper but not impossible. The most realistic bridge is to use your MBA summer internship in best mba for investment banking programs as a way to build the deal toolkit that PE firms expect. Several candidates each year successfully pivot from a banking internship into a full-time PE associate offer, though this route requires an intense ramp-up during your first year of business school.

Be honest with yourself about the timeline. Without prior deal experience, you are effectively compressing years of skill-building into a few months of coursework and one summer. Joining your program's PE or finance club, competing in LBO case competitions, and networking aggressively with alumni already in the industry can help close the gap. Some candidates also target middle-market or growth equity firms that may be more open to non-traditional backgrounds than the largest buyout shops.

The bottom line: your admission profile and your PE recruiting profile are deeply intertwined. Every element of your application, from your test score to your recommenders to the way you frame your goals, should reinforce that you are prepared for the rigor PE demands.

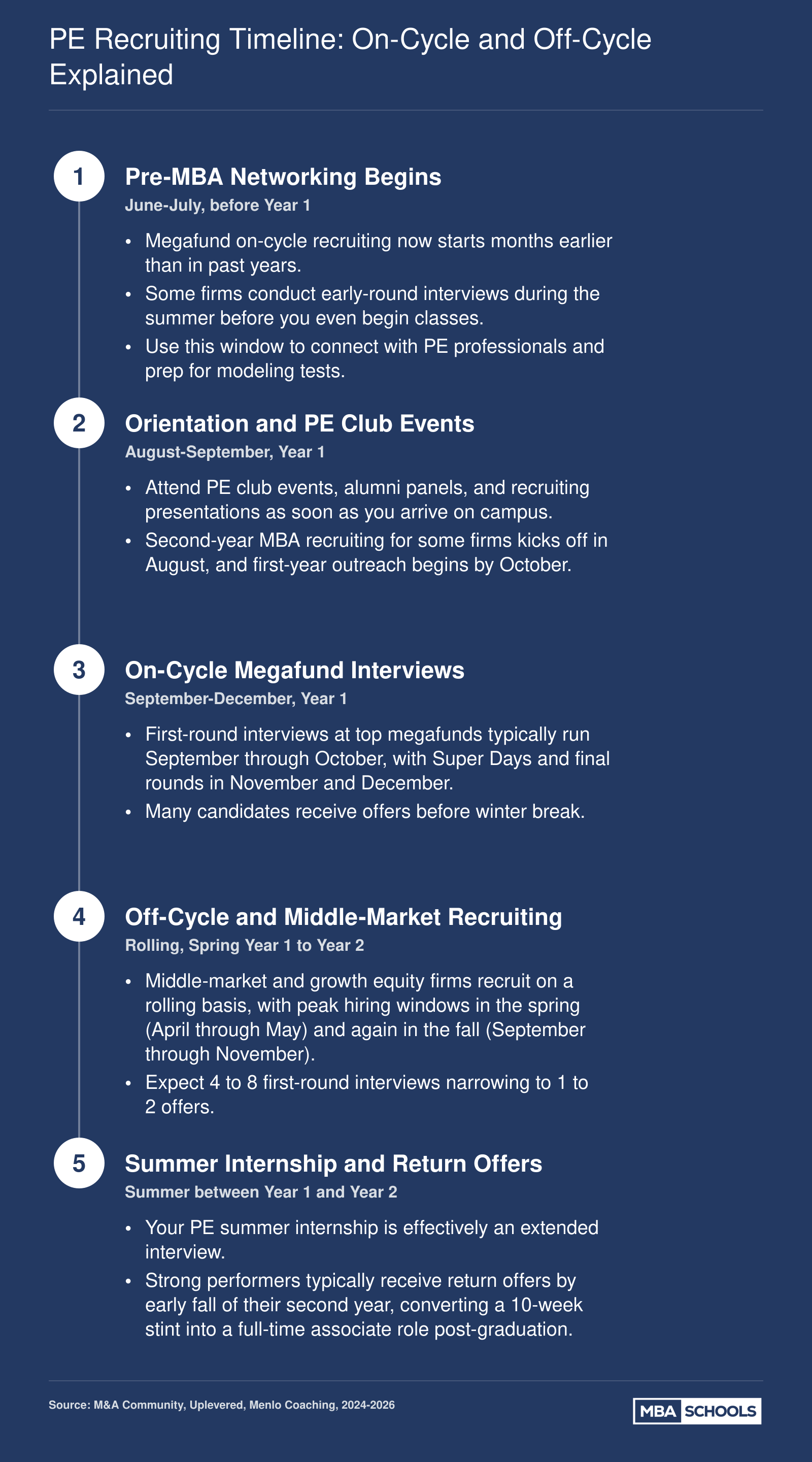

PE Recruiting Timeline: On-Cycle and Off-Cycle Explained

Private equity recruiting has accelerated dramatically in recent years. Megafund on-cycle processes now begin as early as the summer before MBA orientation, while middle-market and growth equity firms recruit on a rolling basis through your second year. Understanding this compressed timeline is essential to positioning yourself for PE internships and full-time offers.

Private Equity Salary After an MBA: Base, Bonus, and Carry

If you have ever searched "do private equity associates really make $200K a year," the short answer is yes, and often much more. Post-MBA PE associate compensation routinely exceeds $200,000 in base salary alone at top-tier firms, with total first-year compensation reaching well into the mid-six figures once bonuses are factored in. Here is a detailed breakdown by firm tier so you can set realistic expectations.

Megafund PE Associate Compensation

At the largest buyout shops (think firms managing $10 billion or more in assets), 2026 compensation benchmarks for post-MBA associates look roughly like this:

- Base salary: $150,000 to $175,0001

- Signing bonus: $75,000 to $100,0001

- Year-end bonus: $150,000 to $300,0001

- Total first-year compensation: $300,000 to $500,0001

These figures reflect the intense competition for talent among firms like KKR, Apollo, Blackstone, and Carlyle, all of which recruit heavily from elite MBA programs. The wide range in year-end bonuses reflects both individual performance and fund performance in a given vintage year.

Upper-Middle-Market and Middle-Market Firms

Compensation remains highly attractive outside the megafund universe, though the ranges step down as fund size decreases.

Upper-middle-market firms (typically managing $2 billion to $10 billion) offer:

- Base salary: $140,000 to $160,0002

- Signing bonus: $50,000 to $75,0002

- Year-end bonus: $120,000 to $250,0002

- Total first-year compensation: $250,000 to $400,0002

Middle-market firms (managing roughly $500 million to $2 billion) offer:

- Base salary: $125,000 to $150,0003

- Signing bonus: $30,000 to $50,0003

- Year-end bonus: $80,000 to $200,0003

- Total first-year compensation: $200,000 to $350,0003

Even at the lower end of the middle market, first-year total compensation typically clears $200,000, placing PE associate roles among the highest-paying post-MBA positions in any industry.

Carried Interest: The Real Wealth Builder

Base pay and bonuses are only part of the story. Carried interest, commonly called "carry," is the share of a fund's investment profits allocated to the deal team. It is what separates private equity compensation from even the most generous corporate salaries.

Carry is typically granted when you reach the senior associate or vice president level and vests over the life of the fund, usually five to ten years. Because PE funds often target net returns of 15 to 25 percent, a meaningful carry allocation can eventually dwarf your annual cash compensation. A principal or partner at a successful megafund can earn millions in carry from a single fund.

For post-MBA associates, carry is rarely part of your year-one package. But the trajectory toward carry is precisely why many professionals accept PE roles that demand 60-plus-hour weeks. Think of the first few years as building the track record and relationships that unlock carry allocations down the road.

Putting It All Together

When you evaluate a PE offer, look beyond the base salary figure. Factor in signing bonuses, performance bonuses, and the long-term carry trajectory. Compensation data from industry surveys confirm that total comp at every tier continues to climb year over year, driven by fierce competition for post-MBA talent.13 If you are weighing the return on investment of a top MBA program, private equity remains one of the clearest paths to outsized financial outcomes within the first decade of your post-graduation career. For broader context on how PE stacks up against other post-MBA paths, explore our guide to average mba salary 2025 across industries and roles.

How to Break Into Private Equity Without a Top-3 MBA

Let's address the elephant in the room: Harvard, Stanford, and Wharton dominate megafund placement, and that is unlikely to change anytime soon. But the private equity landscape is far broader than a handful of multibillion-dollar buyout shops. Middle-market firms, growth equity funds, and sector-specialist investors recruit from M7, T15, and even T25 programs regularly. The key is understanding where your competitive advantages lie and targeting opportunities accordingly.

Leverage Pre-MBA Deal Experience and Industry Expertise

If you attended a strong but not top-three program, your resume needs to do extra lifting. Pre-MBA deal experience in investment banking, corporate development, or consulting gives you credibility that transcends school ranking. Firms evaluating associate candidates care deeply about whether you can build a model, diligence a target, and contribute from day one.

Sector-specific funds are especially promising. A candidate with five years of healthcare operations experience and a T15 MBA can be more attractive to a healthcare-focused PE shop than an HSW graduate with a generalist background. If you have deep knowledge in industrials, technology, energy, or financial services, lean into that specialization during your recruiting conversations.

Use Off-Cycle Recruiting to Your Advantage

The on-cycle recruiting process is compressed, competitive, and heavily tilted toward top-three programs that have longstanding relationships with megafunds. Off-cycle recruiting, by contrast, happens throughout the year and is driven by immediate hiring needs. Middle-market and lower-middle-market firms often fill roles this way, and they cast a wider net when sourcing candidates. Networking directly with fund partners, attending industry conferences, and working with PE-focused recruiters can surface these opportunities before they ever hit a job board.

Navigate International Student Challenges

For international students, H-1B sponsorship adds a significant layer of complexity. Many smaller PE firms are unfamiliar with the sponsorship process or unwilling to absorb the costs and uncertainty involved. To improve your odds, target firms with global office networks, as they are more likely to have existing visa infrastructure. Some larger middle-market firms and growth equity platforms with international operations are known to sponsor, though policies vary year to year. Reaching out to alumni from your MBA program who successfully navigated this path can provide firm-specific intelligence that no career services office can match.

Consider Alternative Entry Points

Private equity is not a single doorway. For professionals exploring broader mba careers, several adjacent paths can lead to the same destination:

- PE-focused search funds: You raise capital to acquire and operate a single small business, gaining hands-on deal and operational experience that PE firms value highly.

- Independent sponsors: These fundless sponsors source deals and raise capital on a deal-by-deal basis, offering earlier exposure to the full transaction lifecycle.

- Family offices: Many single-family and multi-family offices make direct private investments. These teams are smaller, less brand-conscious about MBA pedigree, and often open to candidates with strong analytical skills and relevant sector knowledge.

- Portfolio company operating roles: Working in finance, strategy, or operations at a PE-backed company puts you inside the ecosystem. You build relationships with the fund's deal team and gain an insider's understanding of how value creation works post-acquisition.

None of these paths are shortcuts, but each one builds the type of experience and network that makes a lateral move into a traditional PE associate role realistic. The professionals who break in from outside the top three programs share a common trait: they are relentlessly strategic about positioning themselves where their specific skills matter more than the name on their diploma.

Step-By-Step Career Roadmap: From Pre-MBA to PE Associate

The MBA-to-private-equity pipeline is a well-defined sequence, but each stage demands specific preparation. Expect the full journey from college graduation to a PE associate seat to take roughly 6 to 8 years. Here is what each phase looks like and the critical actions you should take at every step.

Frequently Asked Questions About MBA-To-Pe Careers

Private equity recruiting can feel opaque, especially for MBA candidates navigating on-cycle timelines, program selection, and credential stacking. Below are answers to the most common questions we hear from working professionals weighing the MBA-to-PE path.

An MBA remains the most reliable pipeline into private equity, but the degree alone does not guarantee a seat at the table. As the earlier sections of this guide make clear, the program you choose, the pre-MBA experience you bring, and how skillfully you navigate on-cycle and off-cycle recruiting windows determine whether you land a megafund offer, a middle-market role, or neither.

Your concrete next step: audit your profile against the ideal candidate framework outlined in the admission section. Identify gaps in deal experience, modeling skills, or networking reach, and close them before you apply. If you are still weighing whether PE is the right fit, reviewing how to choose an MBA specialization can help you pressure-test that decision against other high-return paths. The PE industry continues to expand, and MBA programs are building deeper buyout-focused resources every year. The window is open for candidates who show up prepared.

Explore Careers

- Budget Analyst with an MBA

- Business Development Manager with an MBA

- CEO with an MBA

- CIO with an MBA

- CMO with an MBA

- Corporate Strategist with an MBA

- Data/Business Analyst With an MBA

- Digital Marketing Manager with an MBA

- Financial Analyst with an MBA

- Financial Manager with an MBA

- Advertising & Promotions Manager with an MBA